The "New Energy Vehicles" Pivot

An asymmetric way to play this trend while avoiding the miners

One should always be on the lookout for when a major narrative pivots.

An example was the shift from 100% renewables to green/zero carbon (to include nuclear and carbon capture).

New energy vehicles will be a way to maintain the 100% EV narrative as zero emission vehicles (ZEV) or battery electric vehicle (BEV) adoption stalls out over time.

This shouldn’t surprise anyone paying attention to the resource requirements of policy such as the IEA’s Net Zero Roadmap (I can’t remember which page below was from…)

Energy density matters, and no amount of subsidies, regulation, or modelling assumptions (learning rates and avoided impacts approach) can change this.

Take this chart from the Net Zero Roadmap (page 161) material intensity drops by 68% if you exclude steel, aluminium, concrete, and silicon, and I shit you not all the waste rock to get the critical minerals (similar, I guess to showing CPI is flat after removing energy, food and anything that dares to rise in price).

Energy density/economics will win out in the end.

For example, look no further than Germany/VW with their renewables and EV push.

Volkswagen AG plans to close at least three factories, eliminate thousands of jobs and slash wages for tens of thousands of German workers as Europe’s biggest automaker tries to halt its tailspin.

The current IEA projections are that BEVs will dominate between 50% and 90% market share by 2035, with PHEVs (plug in hybrid vehicles) playing a 5-10% role.

While heavy trucks are supposedly going to go from a rounding error in 2023 to 20-50% market share in 10 years…

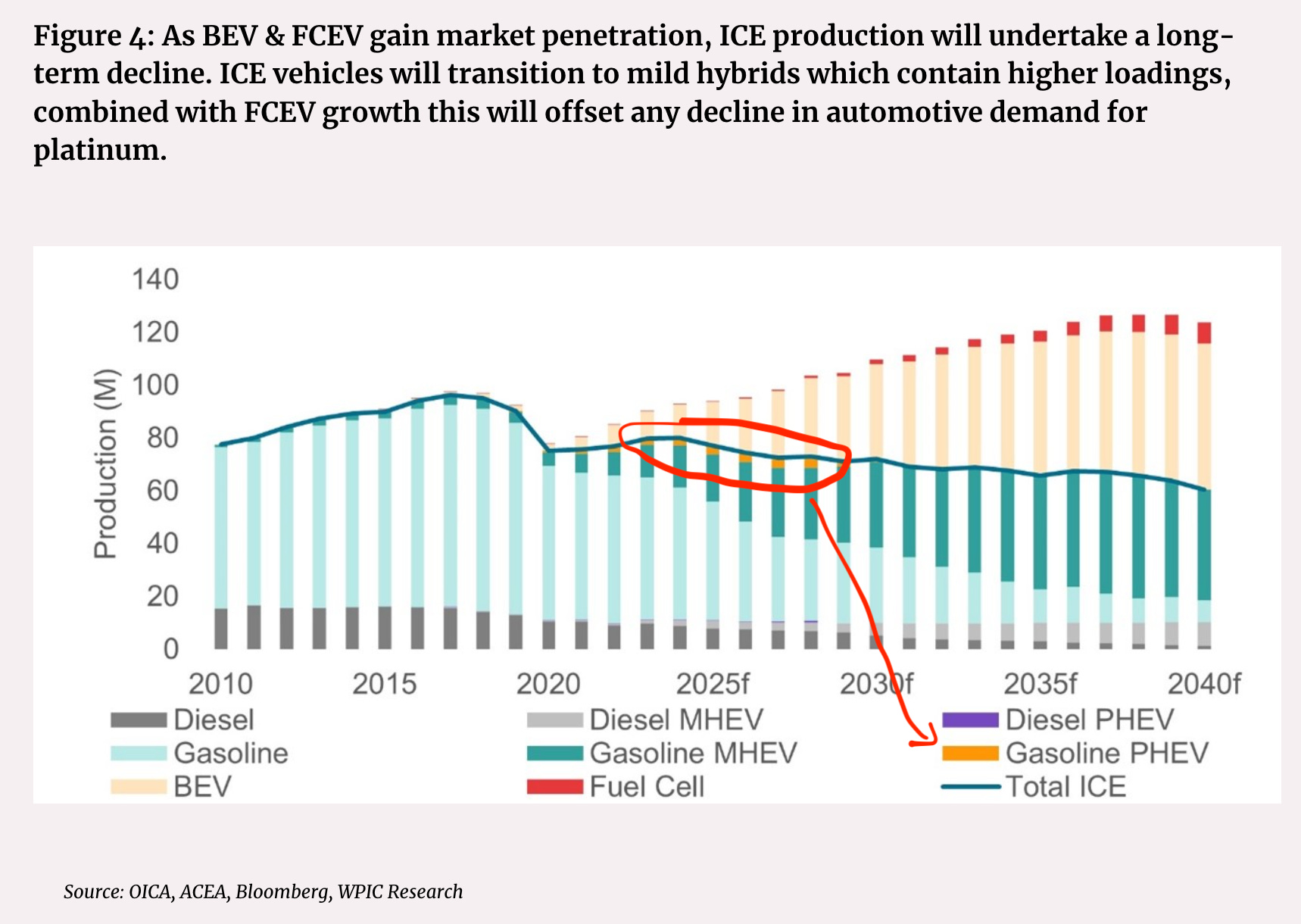

A less extreme forecast is that of OICA, ACEA, Bloomberg and WPIC Research.

They see PHEV as a short-lived phase, with the future split between BEVs and MHEVs (mild hybrids) by 2035.

Mining majors have allocated billions on the certainty of BEV dominating north of 50% market share.

I’m looking for the polar opposite, in an asset where the consensus narrative is it is fucked in terminal/irreversible decline.

This quote was music to my ears having just finished my deep dive on met and thermal coal.

Garvey said the PGM situation had some parallels to coal, which is being phased out as governments slash carbon emissions, but will still be needed for years until more renewable energy is rolled out.

I've already outlined much of my thinking on PGMs here: Pulling the Trigger on Gold and PGMs.

I'll run through demand and supply, and no, this isn't going to culminate in me pitching another PGM miner. If anything, this hedges the PGM miners while likely achieving a larger payoff.

Demand

For those who are new, a quick rehash is that the consensus view is that the PGM market is in for a steady decline due to the reduction in demand for full electric cars.

Platinum demand is best positioned with only 41% for catalytic converters, while palladium and rhodium, with 84% and 90%, respectively, are in trouble if you believe IEA or pretty much any vehicle forecast (BEVs don't require catalytic converters).

The article below was written on 31 January 2024. I note that the PHEV to BEV ratio is 36% this year, and forecast to decline to 32% by 2026.

When you look at the trend of the actual data, it paints a very different picture.

This article hits at the core issue of "pure electric vehicle firms not being profitable," and this is before we get to the second wave of inflation I see coming.

I've been a lithium bear for a long time because I don't see BEV vehicle adoption rates holding up due to material intensity/poor economics and range anxiety/charging constraints (McKinsey: 46% of EV owners said they would go back to ICE cars as their next purchase).

Take this statement from Ford;

“The next generation of Ford EVs will be launched "only when they can be profitable, " Marin Gjaja, head of the Model E EV business, told analysts Tuesday.”

PHEVS > BEV

PHEVs give the best of both worlds with one-third of the critical mineral requirements.

The weighted average battery size for PHEVs for the first half of this year was 23.3 kilowatt hours (kWh), versus 64.5 kWh for pure battery EVs (BEVs), according to consultancy CRU.

To top it off with multiple battery chemistries to choose from with the all the CAPEX having gone to lithium-ion which now sits at the top of the battery cost curve (yes lithium is ion is superior but with a PHEV platform range is no longer a issue.

I see the PHEV/BEV ratio of sales exceeding 75% in 2026.

Which isn’t a stretch when you consider China’s (YTD to October) sales PHEV to BEV ratio is already sitting at 51% YTD.

This is a big deal for the PGM market as PHEVs need roughly 10% more PGMs due to the more frequent cold start of the engine (switching back and forth between battery and internal combustion engine).

Each additional million cars that need catalysts will add about 150,000 ounces of PGM demand, Swarts said.

The main driver of PHEV numbers is BYD. With Sept YTD of the 2.76m "New energy vehicles" they produced, 57% of PHEV, or an additional ~235,000 ounces of PGM demand YTD! (BYD produces ~90% of China's PHEV)

Why the focus on China and BYD?

While western companies like to point to Chinese subsidies as the reason China’s automakers have leap frogged Western automakers there is more to it (China’s EV Makers Got $231 Billion Aid Over 15 Years, Study Says).

To explain it via meme, the Chinese ran a hunger games in each of the sectors they wished to dominate.

It's the way industrial policy should work: You encourage innovation and competition, with only the best surviving and being globally competitive without subsidies.

Big Market Delusion: Electric Vehicles by Rob Arnott highlighted this delusion back in 2021:

The “big market delusion” is when all firms in an evolving industry rise together, although as competitors ultimately some will win and some will lose.

Hence, my focus is on BYD as it's won the Chinese auto hunger games, and China will ensure it has access to cheap energy and critical minerals/processing it needs to scale rapidly (a luxury none of the below competitors have (bar Changan).

Forecasts of anaemic global auto growth of 0-1% YoY are common, which I think ignores the rest of the world, where all the growth will be (the new vehicle buyer will be in India, Brazil, Indonesia, etc.).

I see Chinese auto sales surprising to the upside with their crazy value proposition.

BYD launched the new DM-i 5.0 PHEV platform and advertised its 2100 km range on the Seal 06 DM-i and Qin L DM-i. Both cars were introduced with a starting price of 99,800 yuan (13,750 USD). Real-world tests concluded with 2.54L of fuel every 100 kilometres.

I mean no Western offering comes close, UBS even dismantled a Seal to assess build quality.

The below trend looks set to continue.

The US and EU were quick to throw up the tariffs instead of rejoicing about the potential emission reductions.

It's not that I'm a bearish Western demand for PGMs, either. It's just more a function of ever-stricter emission regulations and the desire for larger vehicles in the US.

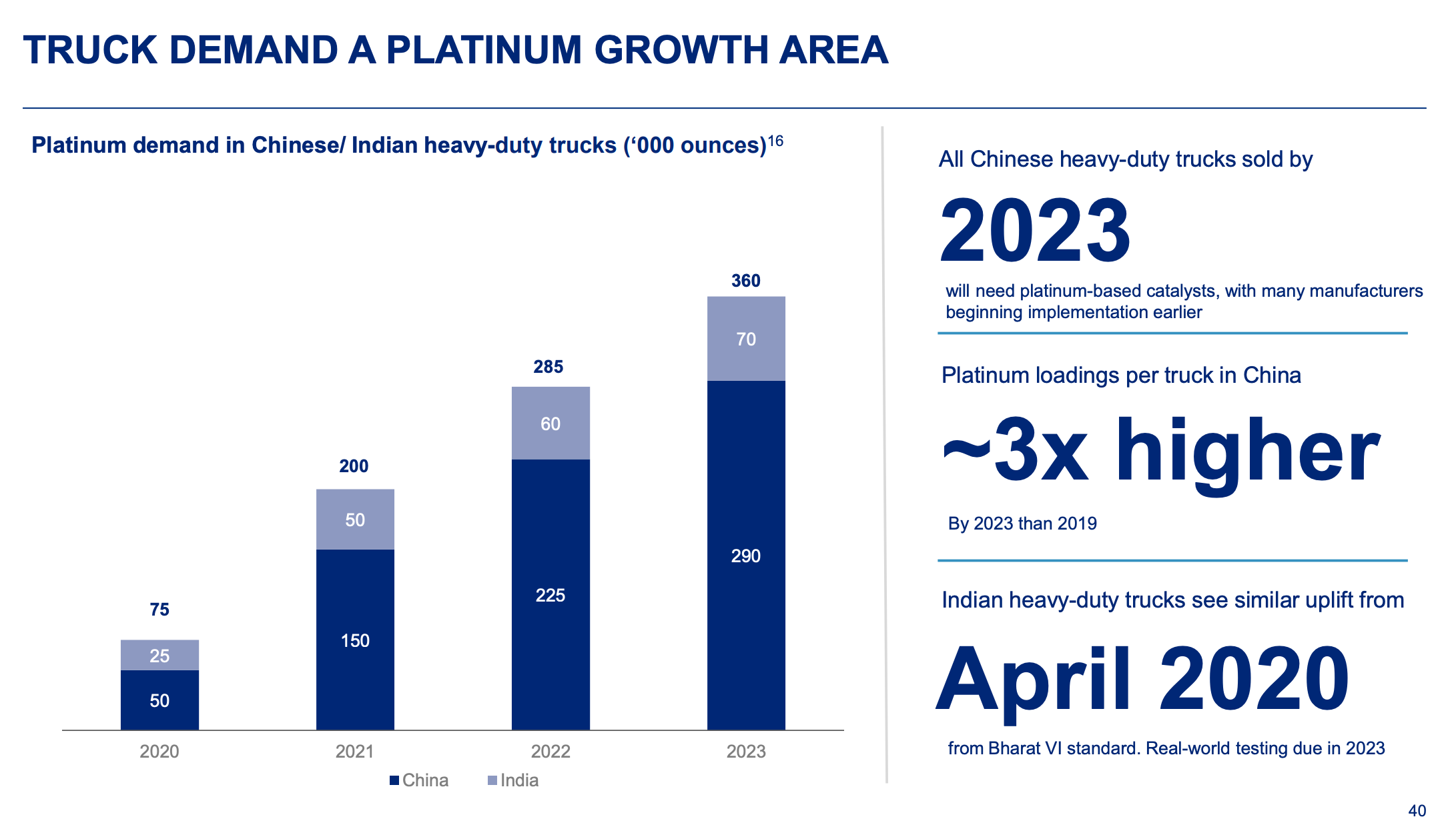

Heavy-truck demand is also a growth market, while diesel trucks don't need a three-way catalytic converter, so they use no palladium or rhodium, driving platinum loading.

In the heavy duty sector, PGM use rose faster than vehicle volumes. This was not due to any specific legislative drivers, but rather due to a sharp increase in production of large trucks powered by compressed natural gas (CNG). This was particularly evident in China, where low gas prices helped stimulate this market segment. These CNG vehicles use gasoline-type catalyst technology but - despite recent thrifting efforts - they typically require much higher PGM loadings than other powertrains.

Also, interestingly, LNG trucks require three-way catalytic converter to meet China's latest China National VI emission standards (switch to stoichiometric engines from lean burn). Granted I'm not convinced the current LNG trend is anything to be extrapolated more a arbitrage of cheap LNG prices (if I'm wrong, it's just more PGM demand…)

.

What about other demand drivers, i.e. chemical, electronics, glass, etc?

I see most of these adding to incremental demand, but I am mostly interested in getting the auto angle correct, as you'll see from how I'm playing this trend.

I'm sceptical about projections of green hydrogen and fuel cell vehicles as I haven't seen anything that makes economic sense. Take this article which summed it up for me: Why Almost Nobody Is Buying Green Hydrogen

I’ll save you 5mins as this is the crux of the article:

But it’s not a simple switch. Most of the businesses that could run on hydrogen would need expensive new equipment to use it, a leap they’re reluctant to make. Hydrogen produced using clean energy costs four times as much as hydrogen made from natural gas, according to BNEF.

The takeaway on demand is I see PGM demand being similar to coal in it’s going to prove more robust then anyway has forecast.

Supply (the deficits are coming)

The majority of PGM consultants and producers are forecasting deficits. Here is Amplats, Johnson Mathey and Davis estimates which take into account the higher PGM loadings for hybrids and the right hand chart includes platinum loadings for heavy trucks.

This should come as no surprise to anyone paying attention to the PGM cost curve with third of miners making losses at current prices (platinum and palladium just over $1000 ounce).

The small amount of CAPEX planned for PGMs is being delayed, and producers are scaling back production, reminiscent of what we saw in the uranium market.

This isn’t the only issue facing mine production either.

South Africa Load Shedding

Not only do you have the price issues, but load shedding is also affecting miners' ability to operate. It's no small issue either, with Dr David Davis pegging the estimated loss at ~19% SA production potentially rising as high as 34%. With South Africa dominating global production, the estimated loss on a global basis is between 11.5% and 18.5%!

There doesn't appear to be any light at the end of this tunnel for South Africa either, with its coal fleet rapidly reaching the end of its life and Germany advising it on its energy policy.

Recycling to the Rescue?

I don't think so, as vehicle scrappage rates have deteriorated over the last five years, with only a slight bump in recycling activity during the elevated PGM prices of 2021 and 2022.

This take from Johnson Matthey was insightful:

It is now clear that shortfalls in auto sales between 2020 and 2022 have had severe and lasting impacts on the second-hand vehicle market. Compared to pre-Covid levels, the volume of non-realised car sales during this three year period amounted to around 25 million units in the mature auto markets of Europe, North America and Japan. As a result, the flow of one-to-three-year-old vehicles onto the second-hand market has been severely curtailed.

This scarcity of nearly new cars, combined with higher borrowing costs and general cost-of-living pressures, has forced buyers to consider older vehicles than in the past. A budget that would have bought a three-year-old vehicle prior to Covid might now be sufficient to purchase a six- to eight year-old car. This has had a knock-on impact across the entire second-hand market, leading to large increases in the value of used cars of all ages, delaying the scrapping of older cars, and increasing the average age of vehicles entering scrapyards.

It's likely a combination of higher borrowing costs, cost-of-living pressures, and the simple fact that cars are lasting longer.

Above Ground Inventories

This is another bear argument against PGMs, and in particular, platinum: that there are large above-ground stocks. While true, the question is how mobile those inventories are and how quickly they could be worked through.

As for over a decade now China has been stockpiling all the platinum it can get its hands on with zero exports of platinum. Again this reminds me of uranium in the bear thesis that China could dump its large uranium stockpile.

It's illogical. Why would they dump a strategic stockpile when rapidly building out their nuclear fleet? The same goes for platinum. Why would they start selling down a commodity they can't produce domestically and is important to industrial growth aspirations?

The two charts below tell the story.

This is an insightful read on the issue: The Platinum Stock Supply Crisis by Dr. David Davis (Dr. Davis is the expert in this space. I reached out to set up an interview only to sadly learn of his passing earlier this year).

Enough rehashing the PGM thesis. What is the new angle?

It’s not Johnson Matthey Plc although I do find that angle interesting.

It's not another South African miner, that's for sure; if anything, this is an angle to hedge the PGM miners.

A hedge that has historically outperformed the most leveraged miners.