Ferg’s Finds

This is a short weekly email that covers a few things I’ve found interesting during the week.

Article(s)

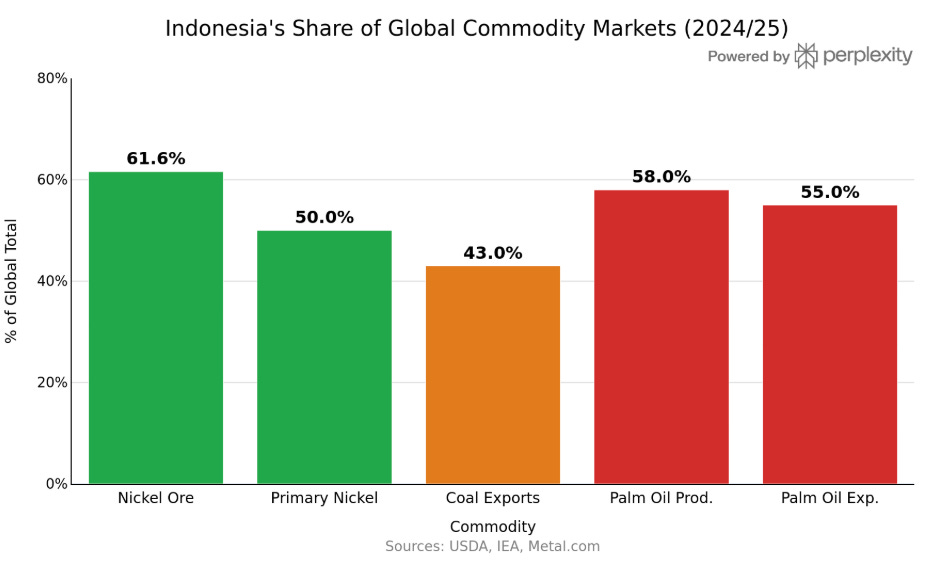

Prabowo’s biggest crackdown on Indonesia tycoons shocked his own officials(21/5/26)

The president then dropped the hammer, confirming that all exports of palm oil, coal, ferro-alloys and potentially other strategic commodities must now be conducted through state-owned enterprises.

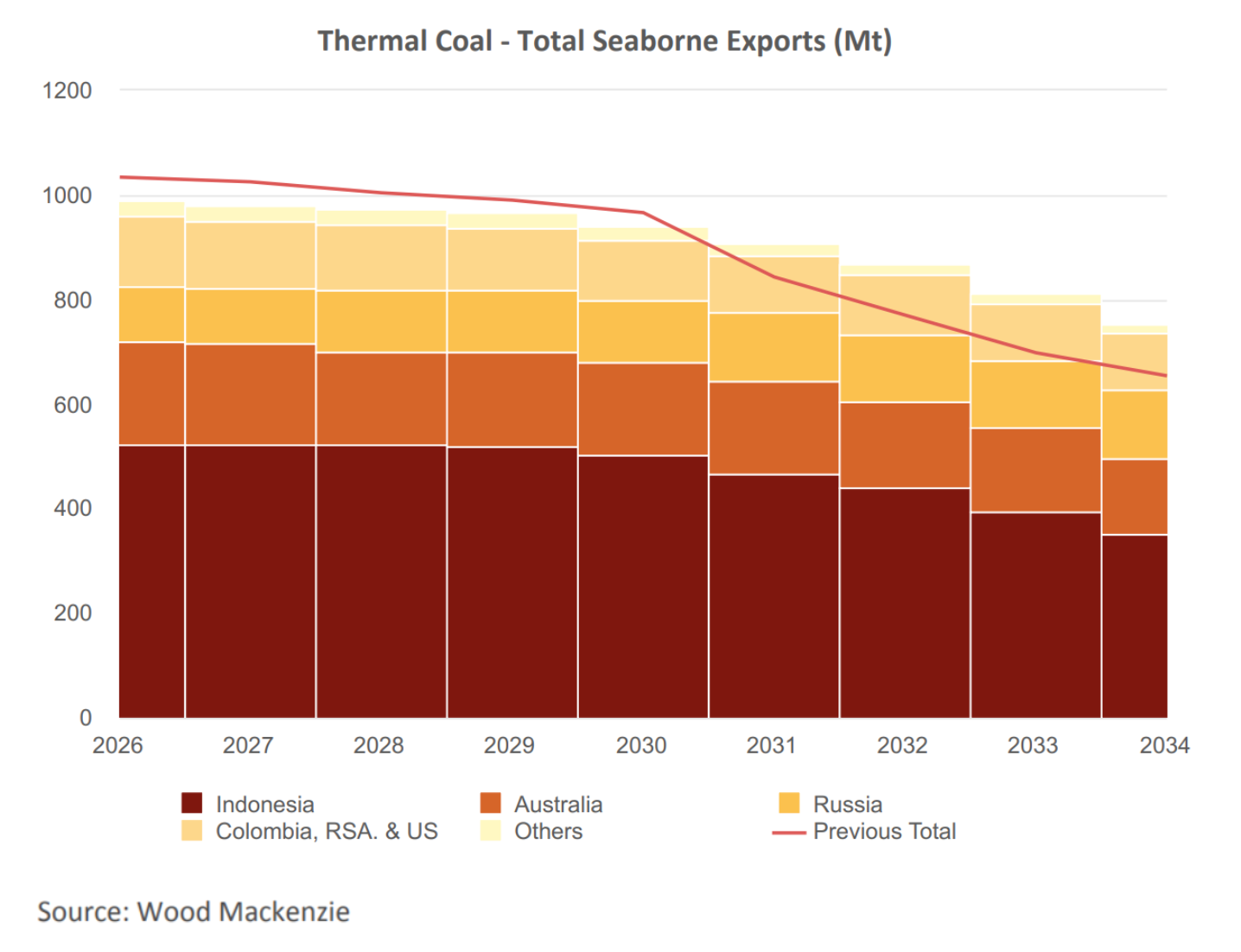

History is clear when governments pursue monopsonies, investment collapses along with supply and Indonesia’s coal supply outlook was already grim.

Podcast/Video

The Money of Mine boys continue to pump out the quality! Both of these episodes are well worth your time.

Quote

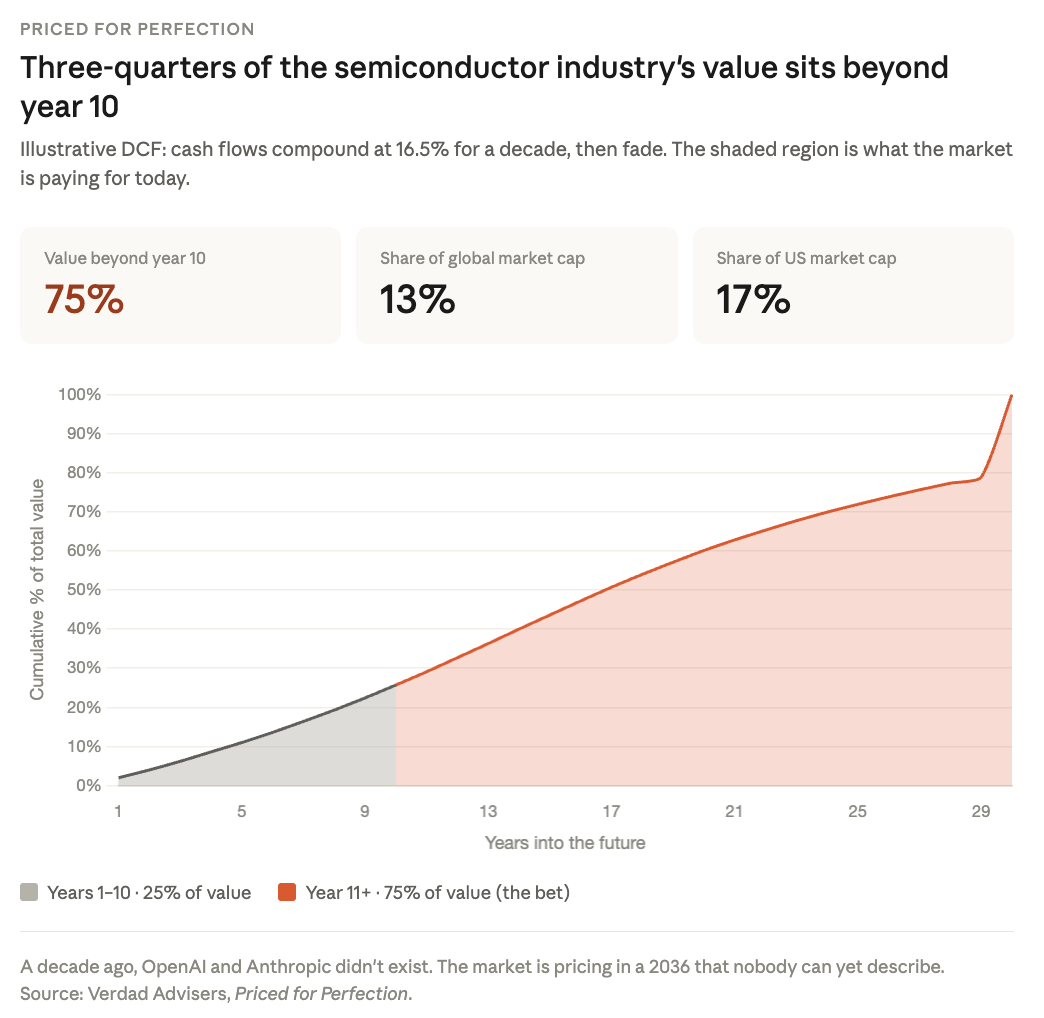

Great way to articulate the over-extrapolation of cyclical industries’ earnings…

Roughly 75% of the current value of the global semiconductor industry (13% of global market cap and ~17% of US market cap) is derived from cash flow projections that are more than 10 years in the future (after first compounding at 16.5% for 10 years). A decade ago, OpenAI and Anthropic didn’t even exist. Who is to say what the world will look like in another 10 years?

-Daniel Rasmussen & Chris Satterthwaite (Priced for Perfection)

Tweet

Fantastic little history lesson on monopsonies in Indonesia by Michael.

Charts

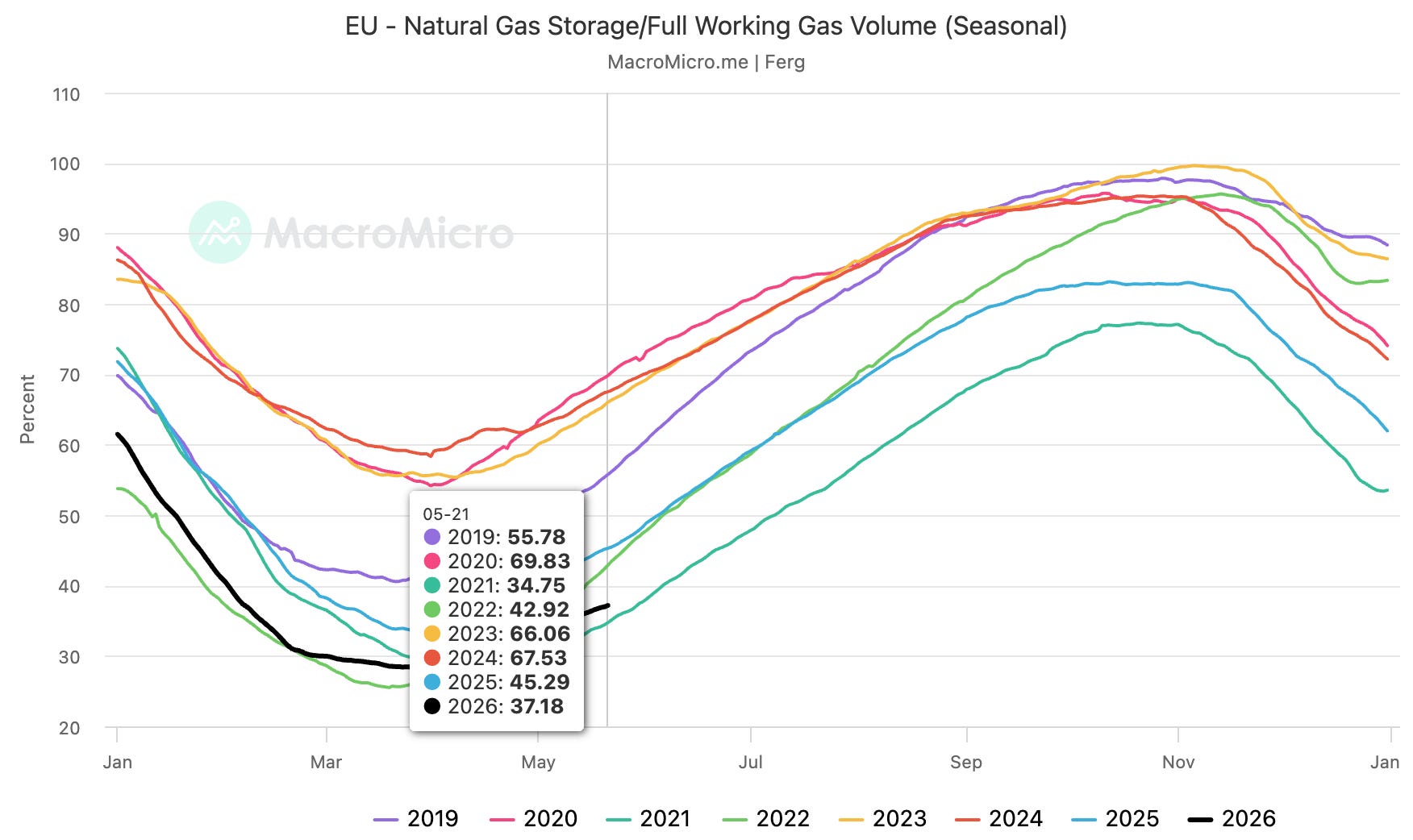

As we exit shoulder season, we now have an explosive mix of Qatar LNG offline, EU storage at record lows, and the potential for super El Niño to boost Asian cooling demand (as I went over in Ferg’s Radar and in detail in this piece).

Something I’m Pondering

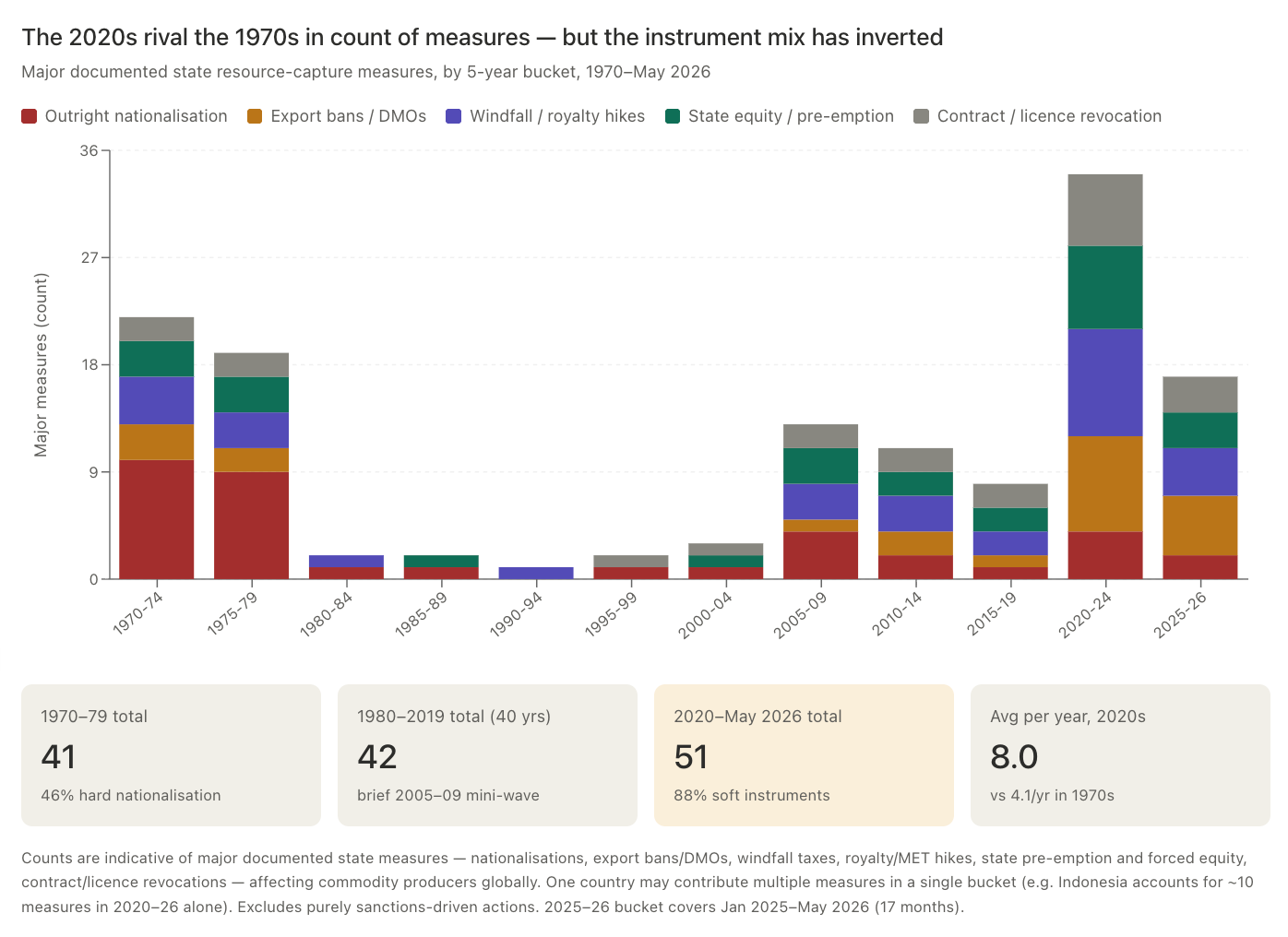

I’m pondering how the constraints on physical supply keep stacking up rapidly. Whether it’s soft nationalisations (as I touched on with Kazatomprom here), state monopsonies as Indonesia has just announced, or the likes of Australia, Europe and the UK doing their best to kill productive capacity via onerous taxes.

A quick search of the frequency of these measures paints a clear picture.

This Twitter thread by Craig Tindale did a great job working through all the issues with the Australian tax reform.

The Architecture of Financialisation: How the 2026 Tax Reform Starves Australian Industrial Capacity

The ultimate consequence of this architecture extends far beyond individual tax bills. By penalising direct, high-dispersion equity and pushing wealth toward unitised wrappers and residential property, the tax code actively starves physical industrial capacity.

At the exact moment the global economy enters a material-constrained environment requiring extraordinary, risk-heavy investment in resource sovereignty and critical mineral supply chains, the domestic system is engineered to retreat from risk. This architecture explicitly divorces capital from physical production, trapping it instead in passive financialisation and housing supply.

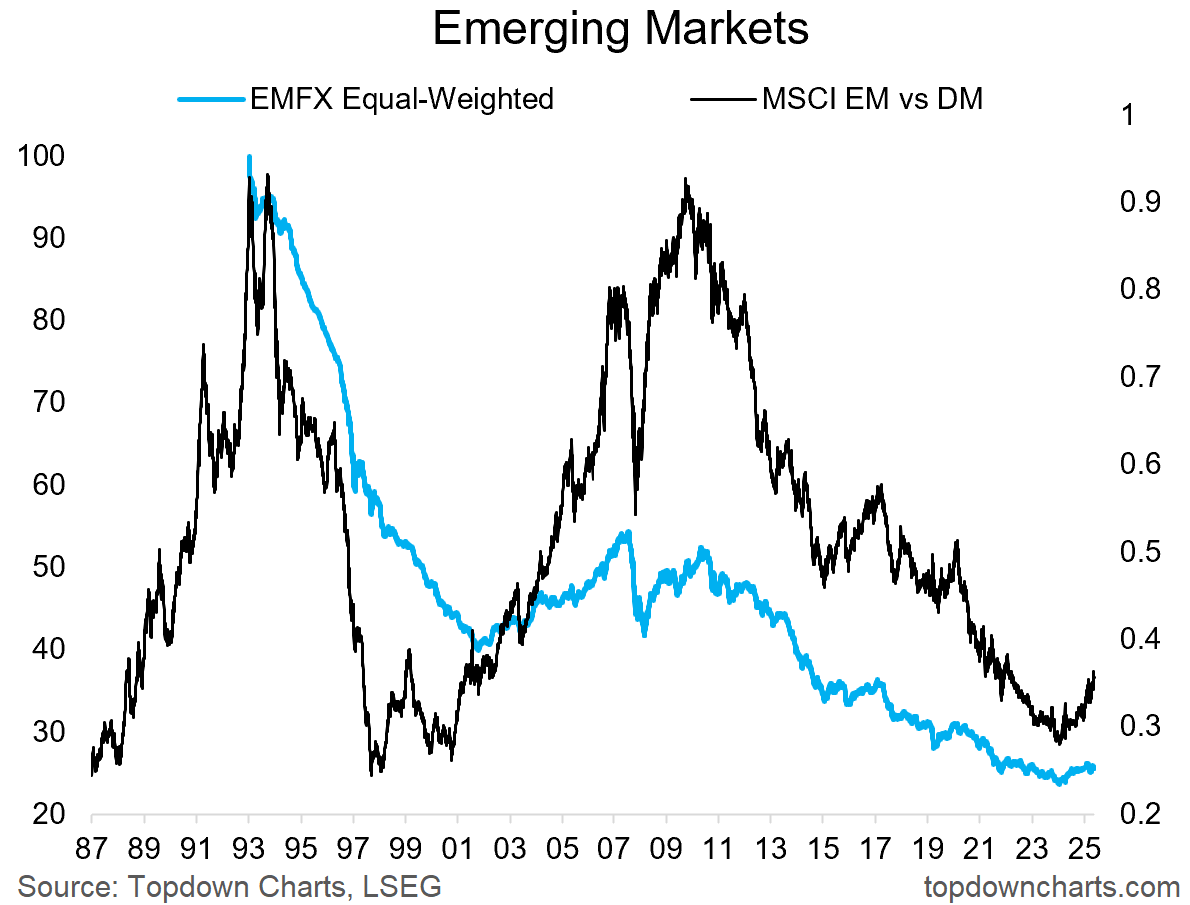

Ultimately, all these constraints are setting the stage for another decade of commodity and emerging-market outperformance. The hard part is how to capture this in the most effective way (certainly not via MSCI EM index as I touched on in the last Ferg’s Finds!)

Hope you are all having a great week!

Cheers,

Ferg

P.S. I wrote this piece to outline a few of the rules I stick to religiously to protect myself from a dose of FOMO…

Wonderful content for American investors looking for alternatives to U.S. companies, U.S. Exchanges and Wall Street financial advisors. The young “smarts” are apparent, the research is deep and the conversations are always challenging, often scintillating.

A future of emerging Michael Every’s, Luke Gromen’s and Doomberg’s are gestating here for those investors who enjoy being challenged and encouraged to think. Makes me far more optimistic about the world!

great continued point about what's going on with emerging markets & semis; not sure if you called it out (apologies if I missed it), but for EM funds/ETFs that track the FTSE Emerging Markets index instead (such as Vanguard), that index excludes Korea (classifying it as a developed market instead) so you at least dodge the huge slug of SK Hynix & Samsung in the MSCI index