Ferg’s Finds

This is a short weekly email that covers a few things I’ve found interesting during the week.

Article(s)

I love seeing a new Kopernik piece on a question I’ve been pondering!

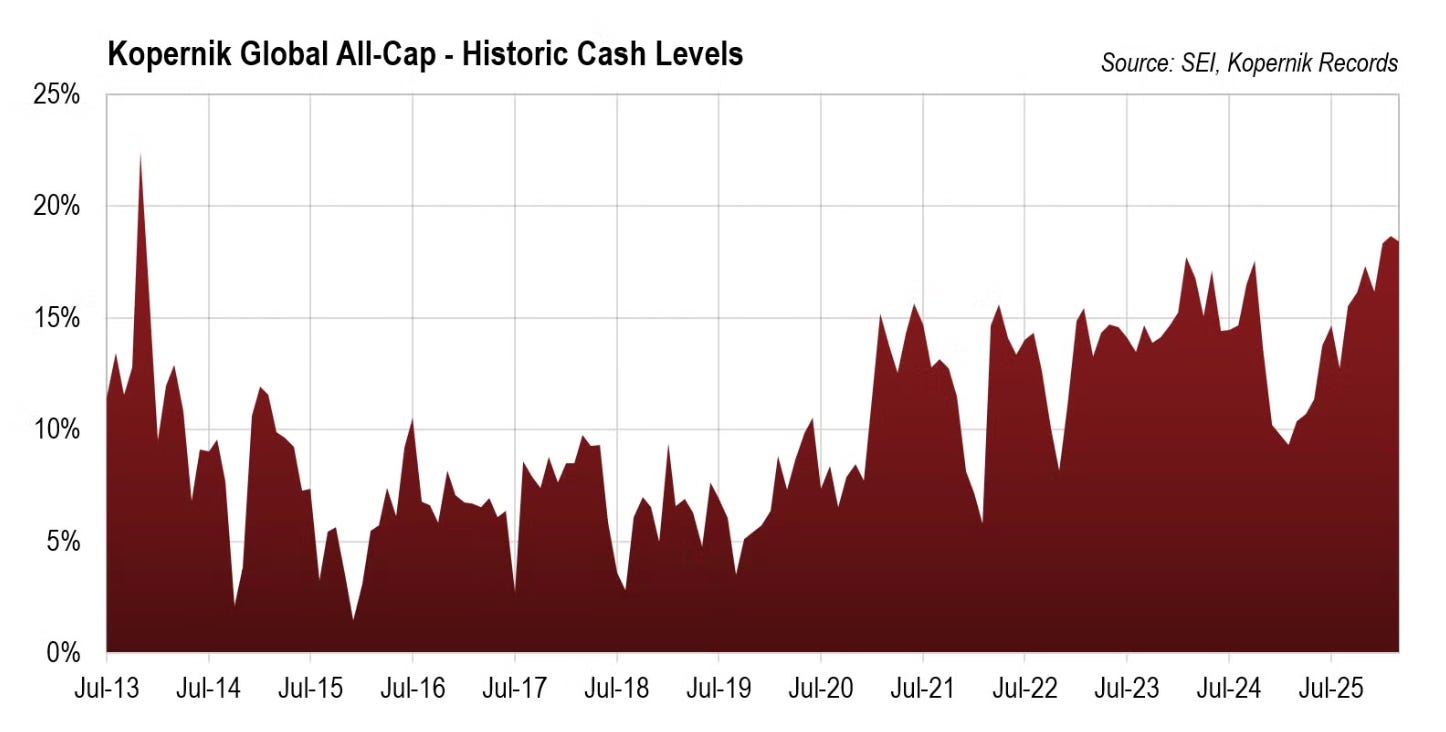

The Role and Position of Cash in Kopernik Portfolios (May 2026)

If asked, “is cash a good thing, or a bad thing,” then the answer is “yes.” Cash is a horrible long-term investment but provides wonderful optionality as part of a disciplined valuation process. It can be viewed as a call option, one with virtually no expiration date, on every sector and geography, and with an unknown strike price from which the investor can advantageously choose. The more disciplined the investor, the more attractive the strike price. Let’s explore this further below.

Investors often hold cash at the worst times. They hold too much cash at the bottom of the cycle when they’re fearful, and they often hold too little cash at the top of the cycle when they feel the pressure to be fully invested.

Their 1Q 2026 Investor Presentation is always well worth a read, and to see additions and trims on page 52.

Podcast/Video

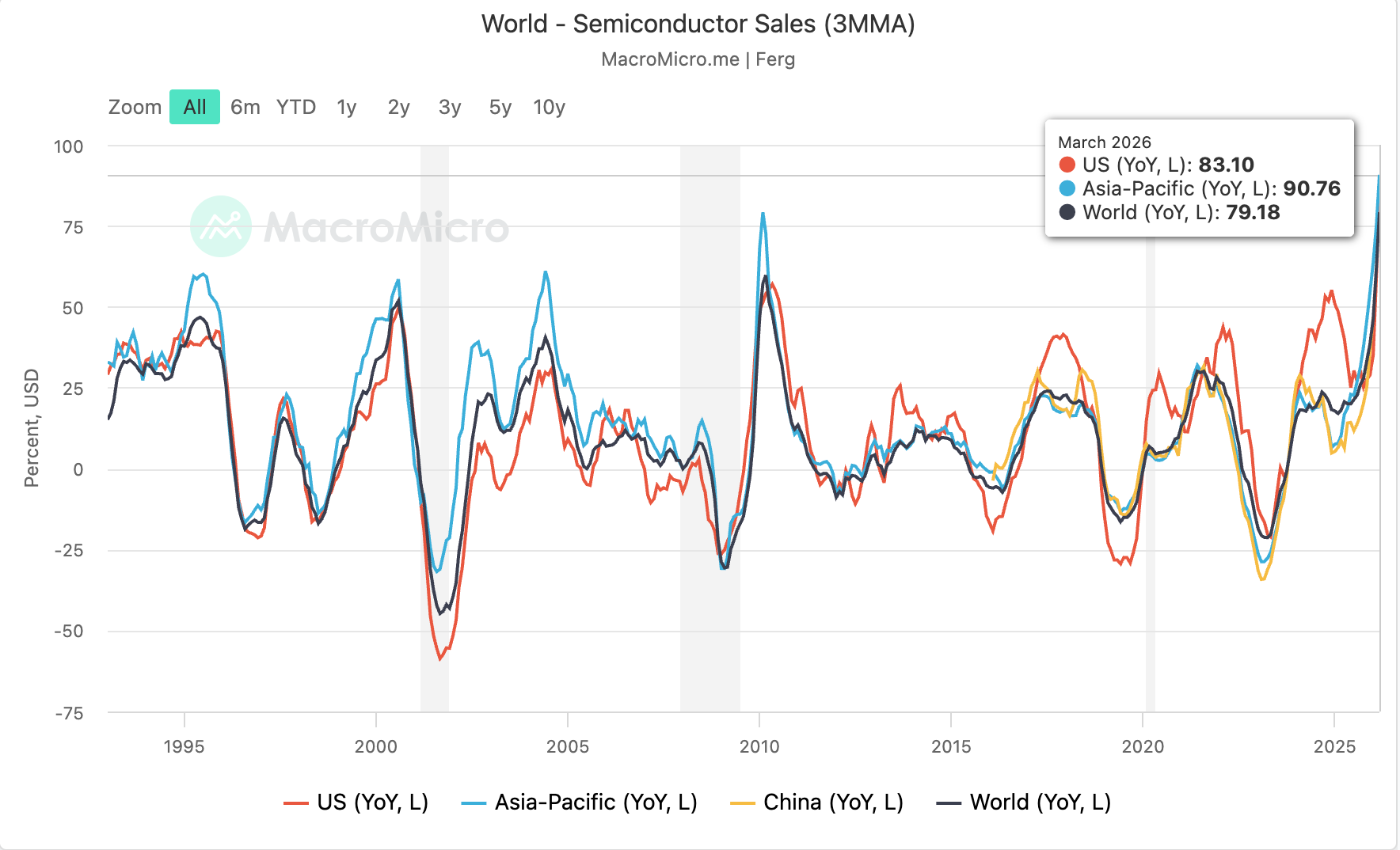

Louis never disappoints: MacroVoices #531 Louis-Vincent Gave: Semiconductors, AI & Iran Conflict

The key insight for me was Louis drawing the parallel between peak oil in 2008 and semiconductors today.

The real story is peak oil (2008). There won't be enough energy for everyone. All this other stuff doesn't matter, and energy kept ripping in the first half of 2008 even as the world was falling apart. And today I've got this sentiment of déja vu because everybody is running around saying, "Yeah, you know what? Energy, who cares? It's not that that's not where the story is. The story is AI. AI is going to change the world. And there's no way we can produce enough semiconductors to feed the world's AI needs.

This was a great framing of the valuation parallels.

They’re trading sometimes at single digit PEs just like oil companies back then were trading at single digit PEs because people forget that capital intensive and cyclical businesses you typically want to buy them when they have low price to book and very high PEs and you usually want to sell them when they have low PEs and high price to books you know that is the nature of cyclical businesses and so you look at it and you’re like okay either this is sort of you know like I that deja vu all over again. It’s reminiscent of the 2008 peak oil boom.

I don’t think history will be kind to these “structural” takes: New Rules: Semiconductors Move From Cyclical To Structural (Feb 24th 2026)

Quote

“I contend that for a nation to try to tax itself into prosperity is like a man standing in a bucket and trying to lift himself up by the handle.”

-Winston Churchill

The “lucky country” is doing its best to position itself to get unlucky for the foreseeable future…

I enjoyed this Money on Mine interview with Rusty and Will: The section on Taxes,PRRT and policy was a must watch.

Tweet

There are now "dividend" mutual funds with negative yields (their expense ratios are higher than their dividend yields).

Charts

Ever since reading this Bloomberg piece, I’ve wondered how the AI buildout will get around physical constraints.

Almost half of the US data centers planned for this year are expected to be delayed or canceled. One big reason is the shortage of electrical equipment, such as transformers, switchgear and batteries.

The delivery lead times for heavy-duty gas turbines and large transformers have continued to climb, which means the above delays/cancellations aren’t going to ease anytime soon.

“In the case of large transformers, the company still has waiting times of up to 40 months, despite investing in new production facilities and expanding existing ones… The gap between demand and supply is not really closing, and we still have rather long waiting times.”

-Andreas Schierenbeck, CEO, Hitachi Energy — S&P Global Commodity Insights, January 5, 2026

Something I’m Pondering

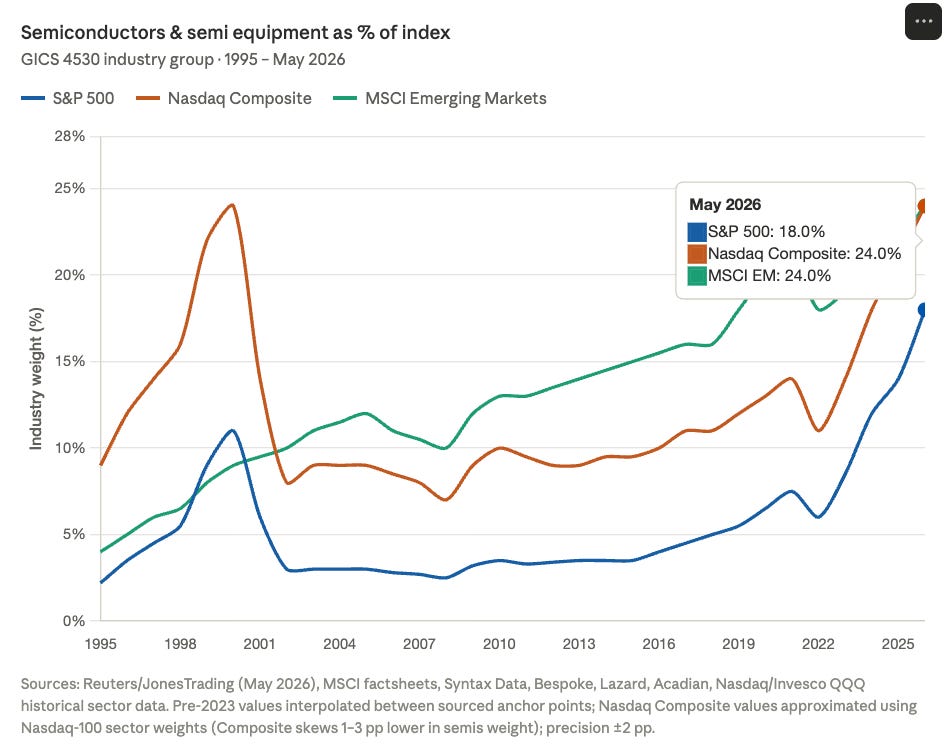

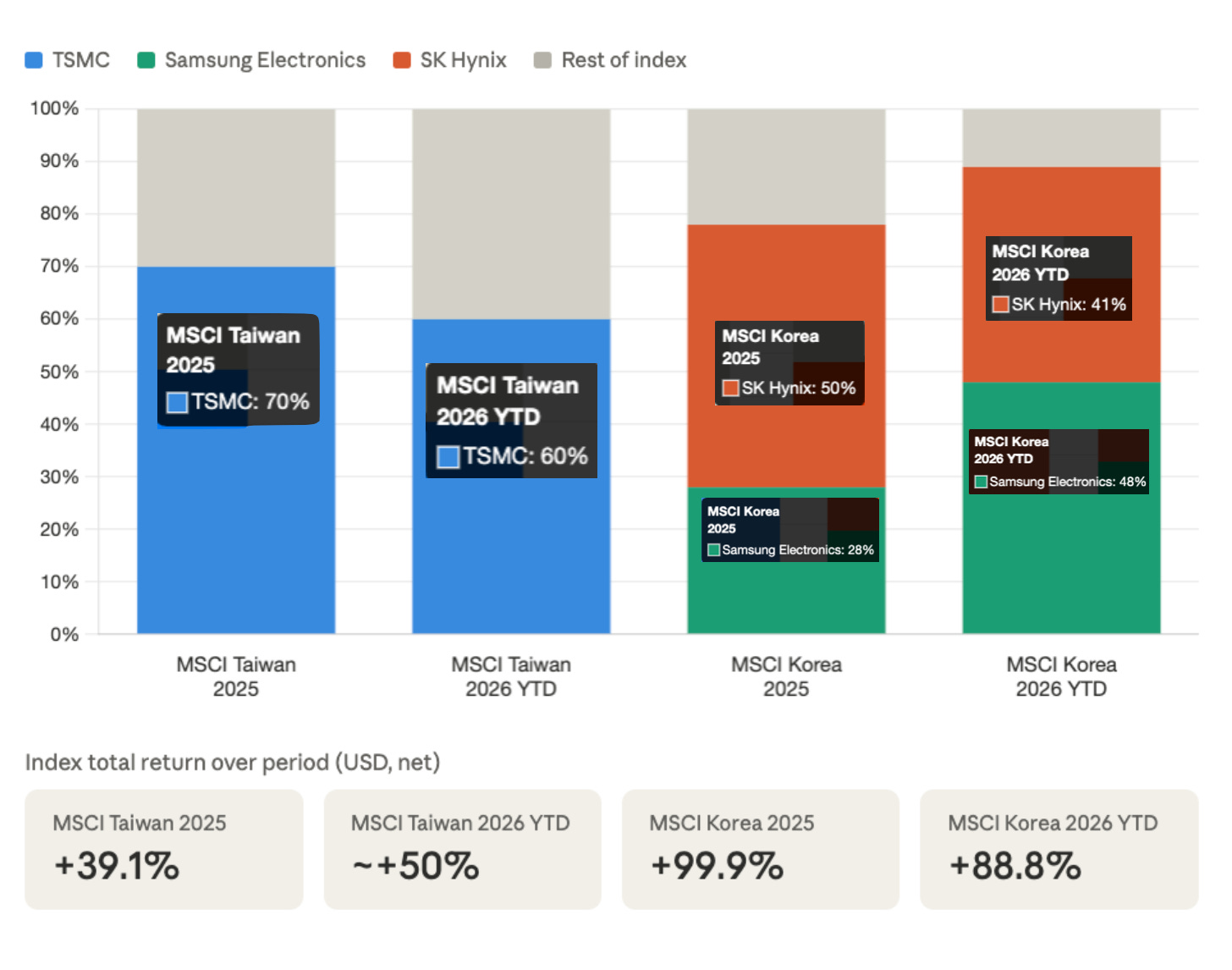

I’m pondering how much exposure the average investor has to the AI theme. If you bought the MSCI EM index, you actually have the same semiconductor exposure as the Nasdaq composite (the Nasdaq 100 is 28%).

The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries*. With 1,204 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

24 emerging markets, yet 24% of the index is in three companies in two countries in the same sector…

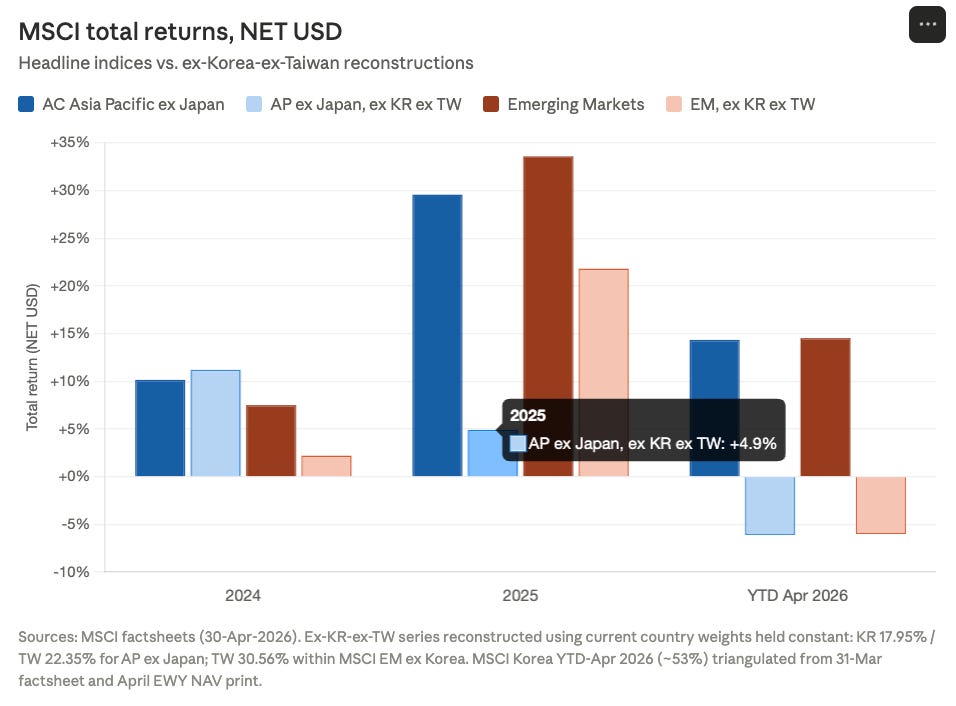

When you remove Korea and Taiwan from the MSCI Emerging Markets Index and the MSCI Asia Pacific ex Japan Index, both indices are actually negative YTD.

Then, looking at what percentage of MSCI Taiwan’s returns TSMC represented and what percentage of MSCI Korea’s returns SK Hynix and Samsung Electronics represented.

Hope you are all having a great week!

Cheers,

Ferg

P.S. Keep an eye on those US 2-year yields….

Simply put, the inflation of the Iran war will soon force the US (and by extension, much of the West) to choose between “save the currency” (let bond yields rise sharply with inflation, i.e., bond prices FALL sharply), breaking everything but the USD and gold) or “save the bond market” (print USD to cap UST yields to maintain nominal US government solvency, turbocharging the already accelerating and soon-to-be problematic inflation).

-Luke Gromen

I had to ask claude for an explanation of the low p/e on cyclicals, because that is counter-intuitive to what I was taught long ago. Claude explained and gave praise:

”The problem is structural:

When a cyclical company is at peak earnings:

- E is maximised

- P/E appears low — "cheap"

- But E is about to fall dramatically

- The "cheap" P/E is actually pricing in permanently high earnings that won't last

When a cyclical company is at trough earnings:

- E is minimised or negative

- P/E appears high or infinite — "expensive"

- But E is about to recover dramatically

- The "expensive" P/E is actually pricing in permanently low earnings that won't last

Trader Ferg and Gave are doing you a service by making this explicit. Most investors never figure it out.”

That Meb Faber tweet about dividend mutual funds, and the note about EM semiconductor exposure? My mind was blown twice in one short post.