Ferg's Finds

This is a short weekly email that covers a few things I’ve found interesting during the week.

Article(s)

Goehring & Rozencwajg: 3rd Quarter 2024 Natural Resource Market Commentary Copper and Uranium: The Coming Divergence

Lots of good stuff in this piece, I found their less optimistic view on copper interesting.

Our research suggests that the universally bullish copper demand forecasts are poised to unravel, potentially leading to bearish copper price implications.

While I’m bullish most commodities, I figured it it paid to be wary with commodities where renewables/EVs played a big roles in the demand outlook (Fantasy Demand vs Real Demand).

I wanted demand that was “knowable” i.e. uranium with operational reactors plus those under construction or “inconvenient demand” i.e. thermal coal demand which continues to surprise to the upside (Global thermal coal exports and power use to hit new highs in 2024: Maguire).

Similar to demand forecasts for lithium and nickel, how much of that forecast 17millions tonnes of renewable copper demand will actually be realised?

S&P Global projects that copper demand will double between 2023 and 2035, climbing from 25 million tonnes to nearly 50 million tonnes. Almost half of this increase—about 17 million tonnes—is expected to come from renewable sources.

Podcast/Video

Valuable to get Luke's take on what the implications of Trump policies could mean for markets: Luke Gromen: What economic advice we would offer Trump

Also, get some insight into the views of one of the people guiding Trump:

Scott Bessent | The Fallacy of Bidenomics: A Return to Central Planning | A New Supply-Side

Quote

“Establishing and maintaining an unconventional investment profile requires acceptance of uncomfortably idiosyncratic portfolios, which frequently appear downright imprudent in the eyes of conventional wisdom. Unless institutions maintain contrarian positions through difficult times, the resulting damage of buying high and selling low imposes severe financial and reputational costs on the institution.”

― David F. Swensen

Tweet

Some interesting conclusions, particularly the shorting of SMR companies.

This was also a great dive into the lithium market.

I’m less optimistic about long term demand I don’t see EVs, heavy vehicles and energy storage ever scaling as the economics don’t make sense now and likely won’t make sense in a higher structural inflation.

Long term demand thesis is still strong. ESS, EVs, drones, buses, mining trucks, the whole laundry list. This suppressed lithium pricing & continued dominance of LFP are all doing numbers for downstream demand.

Expect wind + solar + ESS to be preferred electricity generation product mix for the global south that is developing, without wide industrial bases that need high base load, and in countries that are short O&G. (which is about 3 billion people btw).

Charts

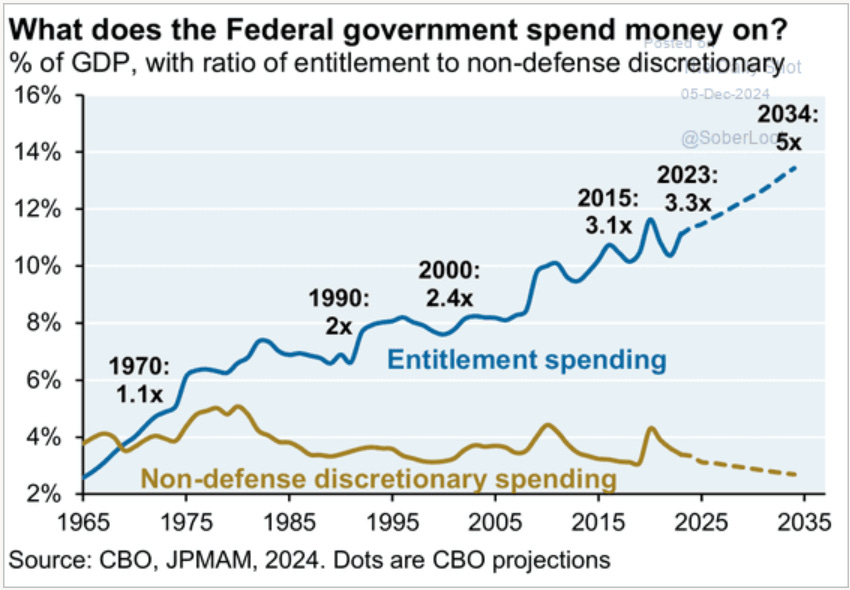

Two charts on why there is more inflation on the way.

What is going to get cut that makes a meaningful difference?

Something I'm Pondering

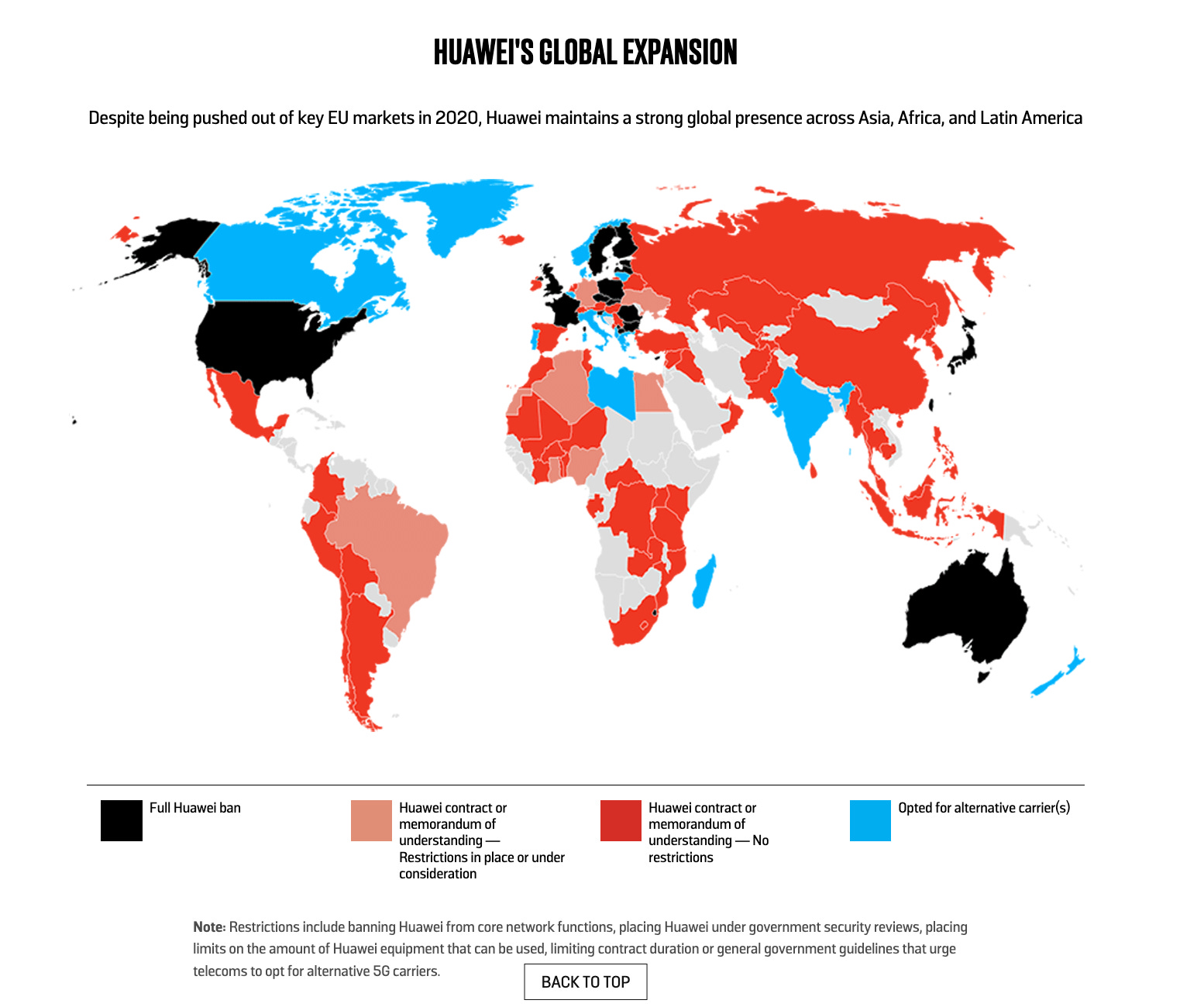

How to capture this trend? South Asia and Africa account for 44% of the global population, and it's pretty incredible that South Asia's share of the population using the internet has gone from 20% in 2018 to 42% as of 2022 (probably over 50% now).

It's clear China is dominating 5G in South Asia and Africa.

Similar to global trade.

How to profit from this trend?

Well, I’m hoping to capture it with Chinese tech as per my latest piece: Hated Tech?

I hope you’re all having a great week.

Cheers,

Ferg

P.S. If you’re interested in my story and why I started this Substack, you can read the story here.

I hesitate to push back at G&R... but I suspect they are missing the full-scale grid build-out that is likely in the US. It seems broadly bipartisan in support and is going to take a lot of copper and other metals. I am expecting a lot of the "environmental blockages" towards construction to be tossed out by the new administration. This is going to be a lot more than just major powerlines-- it will reach right down to the neighborhood level.

Transformers and wires will be a major, possibly profitable, constraint.

Most U bulls do not seem to be factoring in U consumption from SMR's, as its a big unknown. This adds weight to that thesis.