Ferg’s Finds

This is a short weekly email that covers a few things I’ve found interesting during the week.

Article(s)

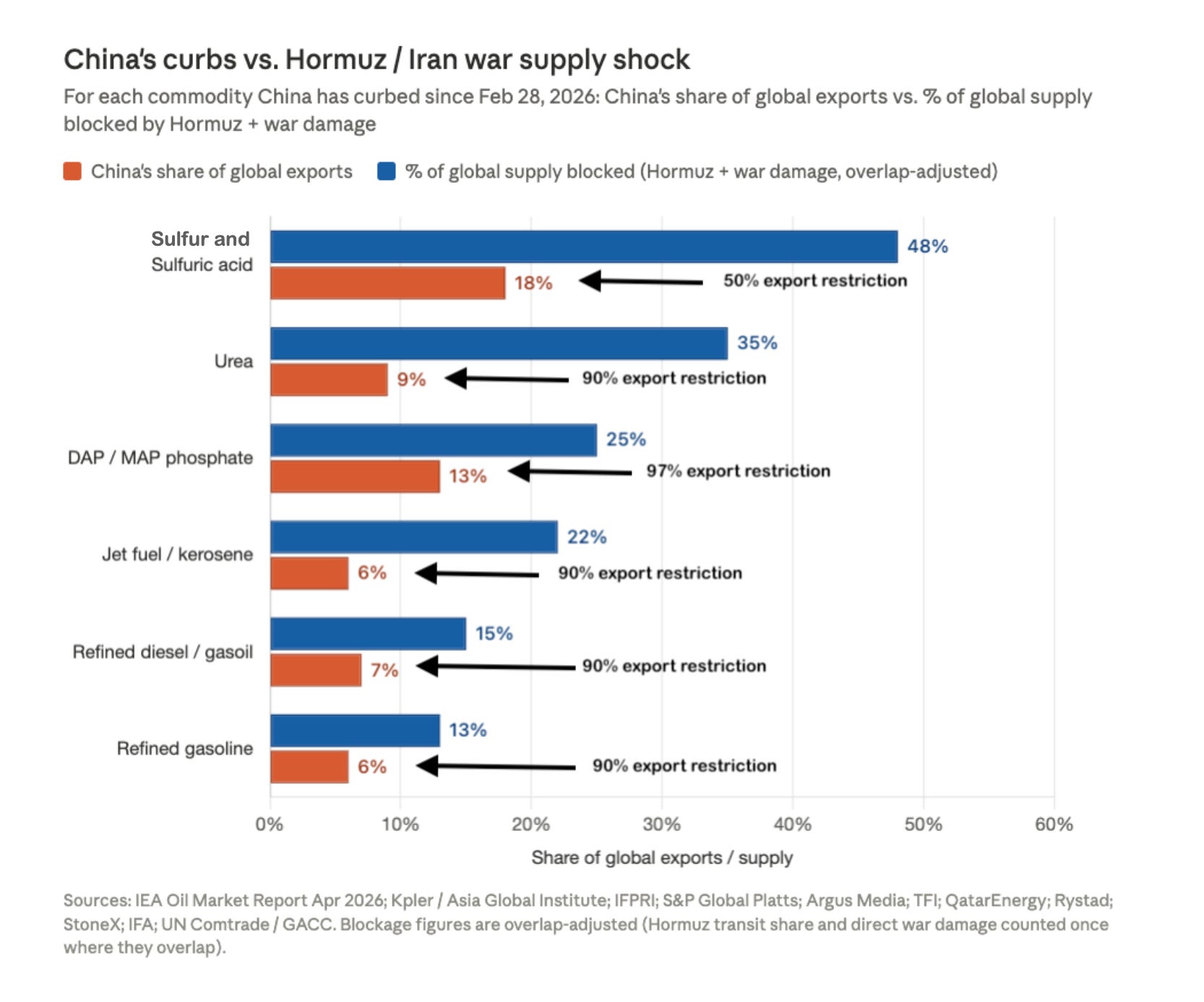

China restricts fertiliser exports, further crimping war-tightened supply.

That would mean between half and three-quarters of China’s exports last year are restricted, potentially up to 40 million metric tons, according to a Reuters estimate.

‘Fortress China’ shows cracks as Iran war strains supply chains.

Beijing implemented a de facto ban on exports of diesel, jet fuel and some fertiliser products in the early days of the war in order to protect domestic supply. Analysts and diplomats have warned that a protracted conflict could trigger further export bans on products including plastics, fertiliser blends and industrial inputs such as sulphuric acid as China’s supplies start to run thin. This could threaten foreign countries that rely on Chinese trade.

When you add these Chinese restrictions to the Hormuz Strait blockages, it’s going to exacerbate the issues we are already seeing globally.

Podcast/Video

This was great, Ed is a class act: Iran War Has Pushed Global Shipping Markets To The Brink | Ed Finley-Richardson

Michael Howell: We Are Coming To An Inflection Point — Where Liquidity Is Headed

Takeaways:

Global liquidity peaked around Q3 2025 and is now in a downtrend, pointing toward a trough in 2027, which historically aligns with tougher conditions for risk assets.

The current equity rally is described as “phony” because it is occurring against deteriorating liquidity conditions; prices look strong, but the monetary backdrop is weakening.

We are in a classic speculation phase of the cycle: economies feel strongest right before things get difficult, and that is when investors tend to over‑allocate to risk.

Quote

“There’s a clear way to sort noise from signal here, which is the movement of troops and the movement of forces. So what you are seeing is a steady progression of American forces, one unit or another, moving toward Iran. You’re seeing no force moving away from Iran.”

-Robert Pape (time stamp in interview)

Talking of escalation, this headline caught my attention: Pentagon approaches automakers, manufacturers to boost weapons production, WSJ reports.

Tweet

With so much misinformation and resulting volatility (the latest being the Strait open on the 17th at 8:57pm and closed on the 18th at 6:42pm), it pays to focus on a few ‘knowables’.

For example, has a single loaded LNG carrier managed to transit the strait?

The answer is still no.

Charts

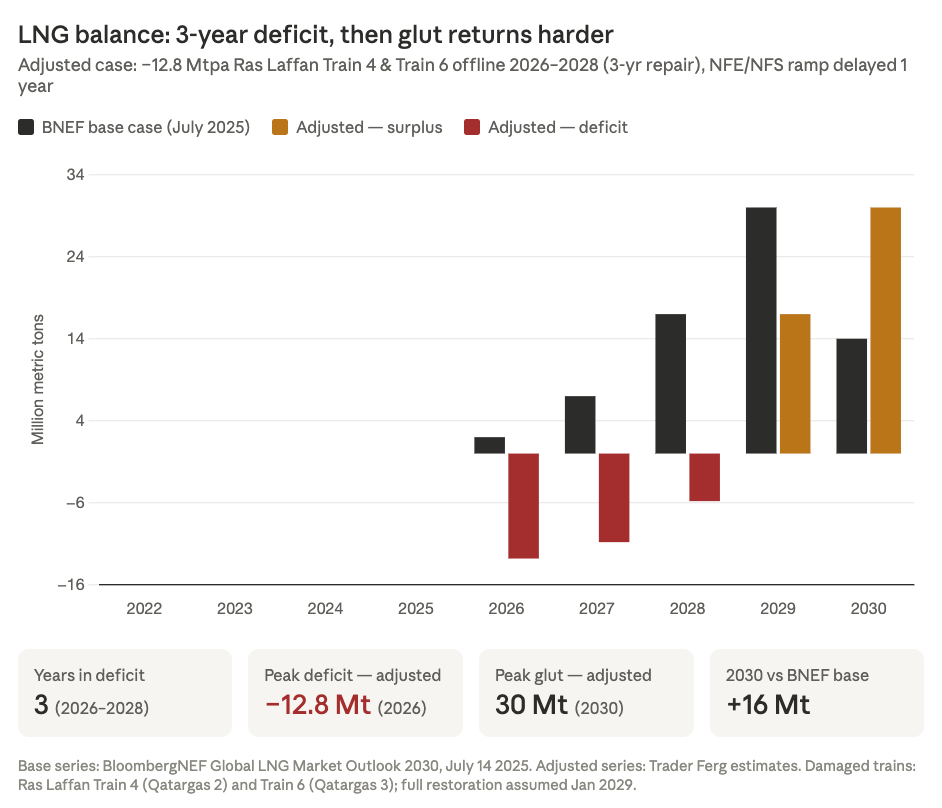

I dug into this in depth in my recent piece, with a key observation being that with 12.8Mtpa damaged at Ras Laffan and NFE/NFS both delayed, the LNG glut has flipped to a deficit out to 2029 (assuming the T4 and T6 can be repaired in 3 years and the delays to NFE/NFS are a year).

The black bars above show the glut the sector faced prior to the Iran war.

A tight LNG market will price out emerging Asian countries, and with an ever-growing percentage of the LNG (especially ex-Qatar), it is destination flexible, meaning it heads to the highest bidder, with poorer nations priced out. Strong coal demand and a push for solar and nuclear are clear takeaways.

Something I’m Pondering

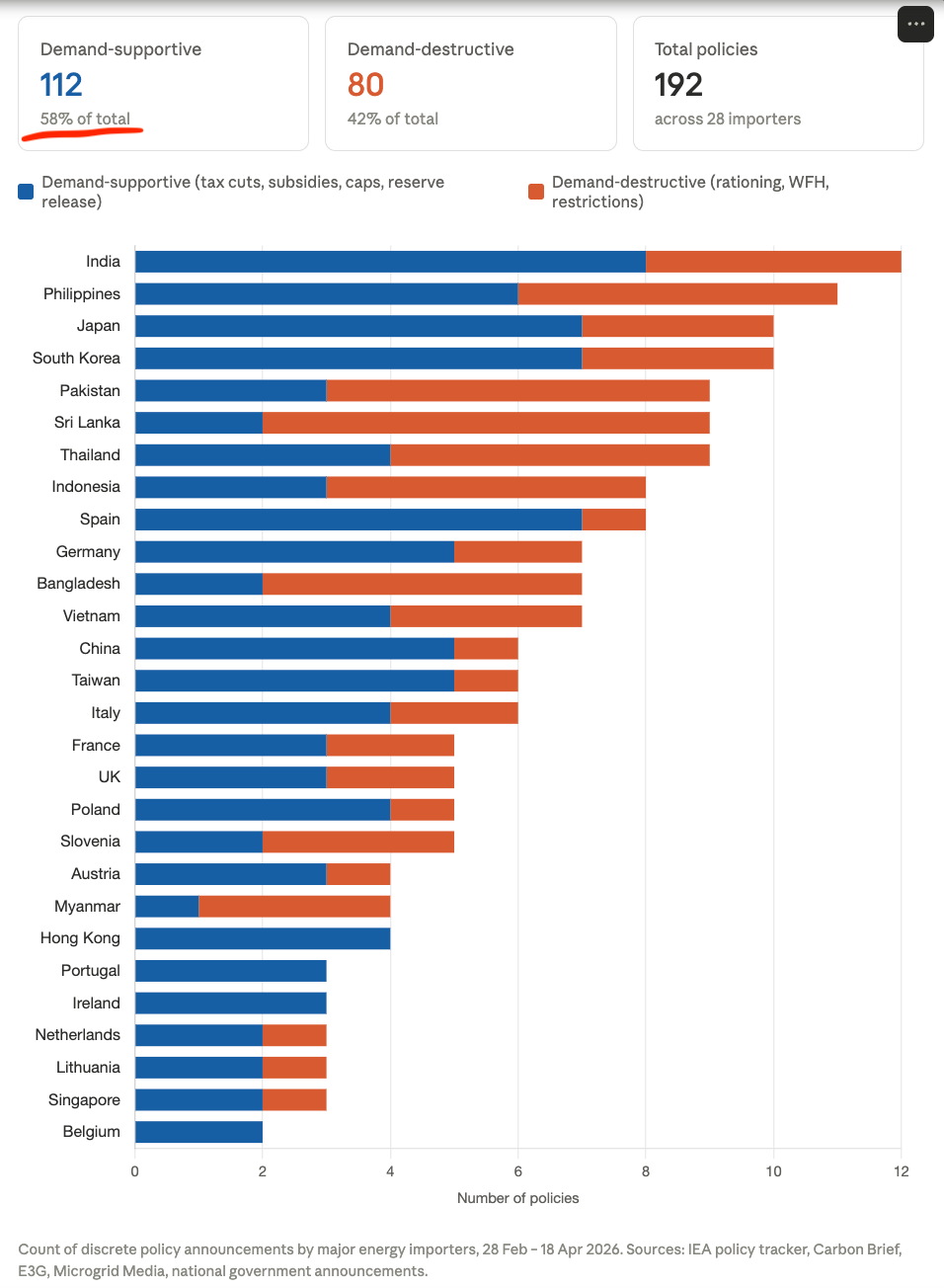

I’m pondering what percentage of policy responses have been demand supportive vs demand destructive?

Analysing the energy policies announced by major energy importers since 28th February provides an interesting overview. Unsurprisingly, wealthy countries are implementing far more demand-supportive policies, while poor countries like Pakistan, Sri Lanka and Myanmar are forced to push demand-destructive policies (or Blackouts Pakistan Faces Extensive Blackouts as Gas Shortfall Worsens).

Hope you are all having a great week!

Cheers,

Ferg

P.S. I wrote this piece to outline a few of the rules I stick to religiously to protect myself from a dose of FOMO…

In regards to CT’s comments on sulfuric acid’s use in ag products/ food shortages. Asia and Africa look to take biggest hits.

In the China chart, I’m not clear if you add the two bars together or if one is a subset of the other. Which is it?