Fergs Finds

This is a short weekly email that covers a few things I’ve found interesting during the week.

Article(s)

These are the big flows I’m trying to front-run.

China’s $1.2 Trillion Windfall Quietly Seeps Into Global Markets

The shift in China’s foreign assets from the central bank to the private sector is ushering in a new era of global capital flows, with risks of a sudden capital reversal and increased sensitivity to yuan appreciation, and potentially leading to a global financial system reliant on liquidity sourced from China.

Chinese Savers Have $23 Trillion and Few Options Beyond Stocks

The idea that China’s small investors will shift a chunk of their $23 trillion savings pile to the stock market is a tantalizing one for global firms, who are showing signs of returning after years on the sidelines.

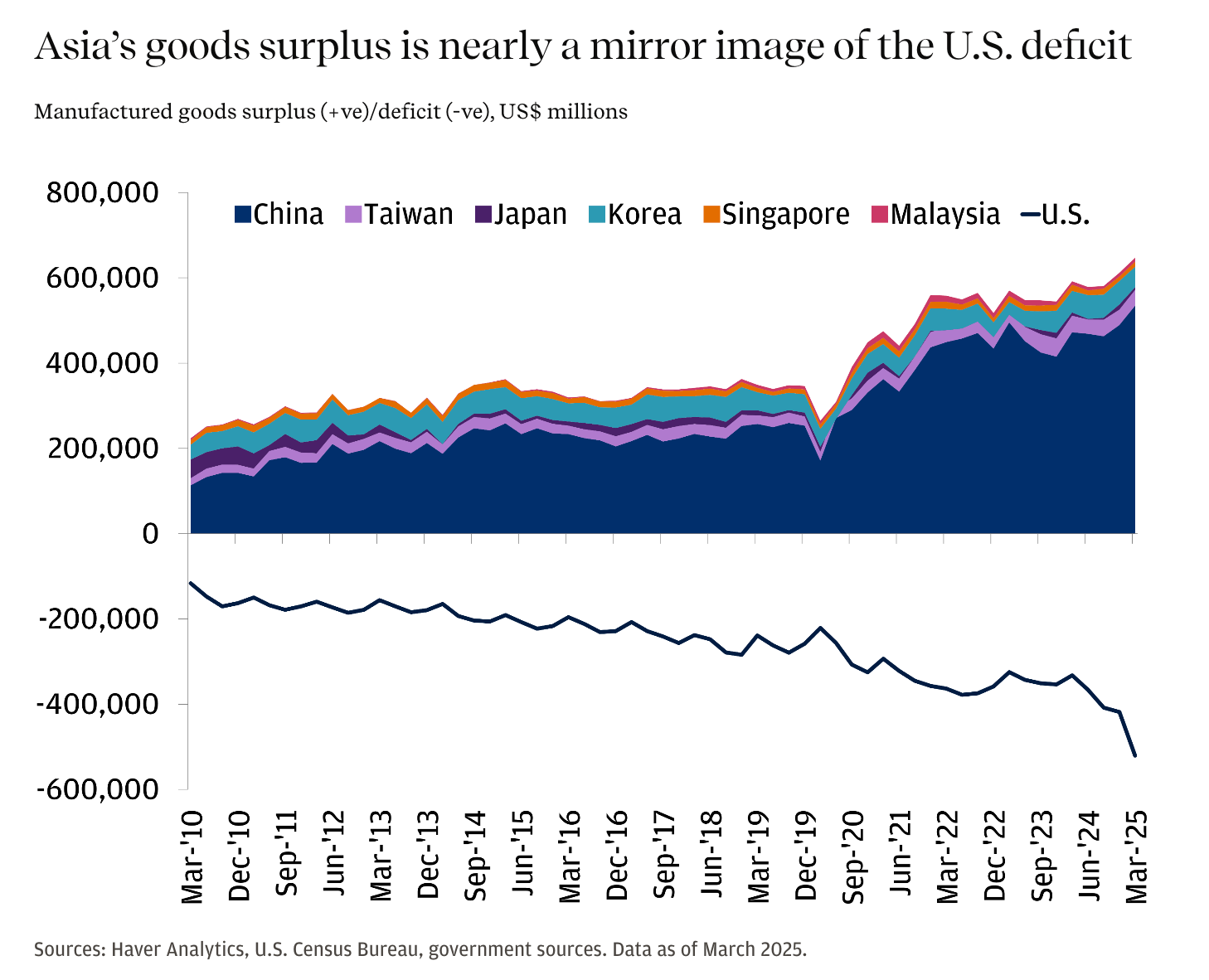

US and China Flip the Global Script as Capital Flows Reverse

China’s outbound investment is a consequence of a trade surplus that has continued to grow as efforts to increase domestic consumption falter and Chinese companies seek new markets. Where once China’s trade surplus ultimately ended up in US Treasuries via a state-controlled system, the capital is now funding new foreign factories.

It’s wild when you consider not only are China’s surpluses no longer being recycled into Treasuries, but the rest of Asia no longer needs to store their surpluses in USD to ensure they have access to the commodities they need to grow, since China/Russia is more than happy to do deals in their own currencies.

Podcast/Video

This had a bunch of great slides: Jeffrey Gundlach’s Just Markets: Clue

Quote

“While the West financializes deficits, rivals industrialize surpluses.”

-Craig Tindale

Tweet

I love Louis’s framing of the Chinese setup as reminiscent of the post-GFC United States.

Charts

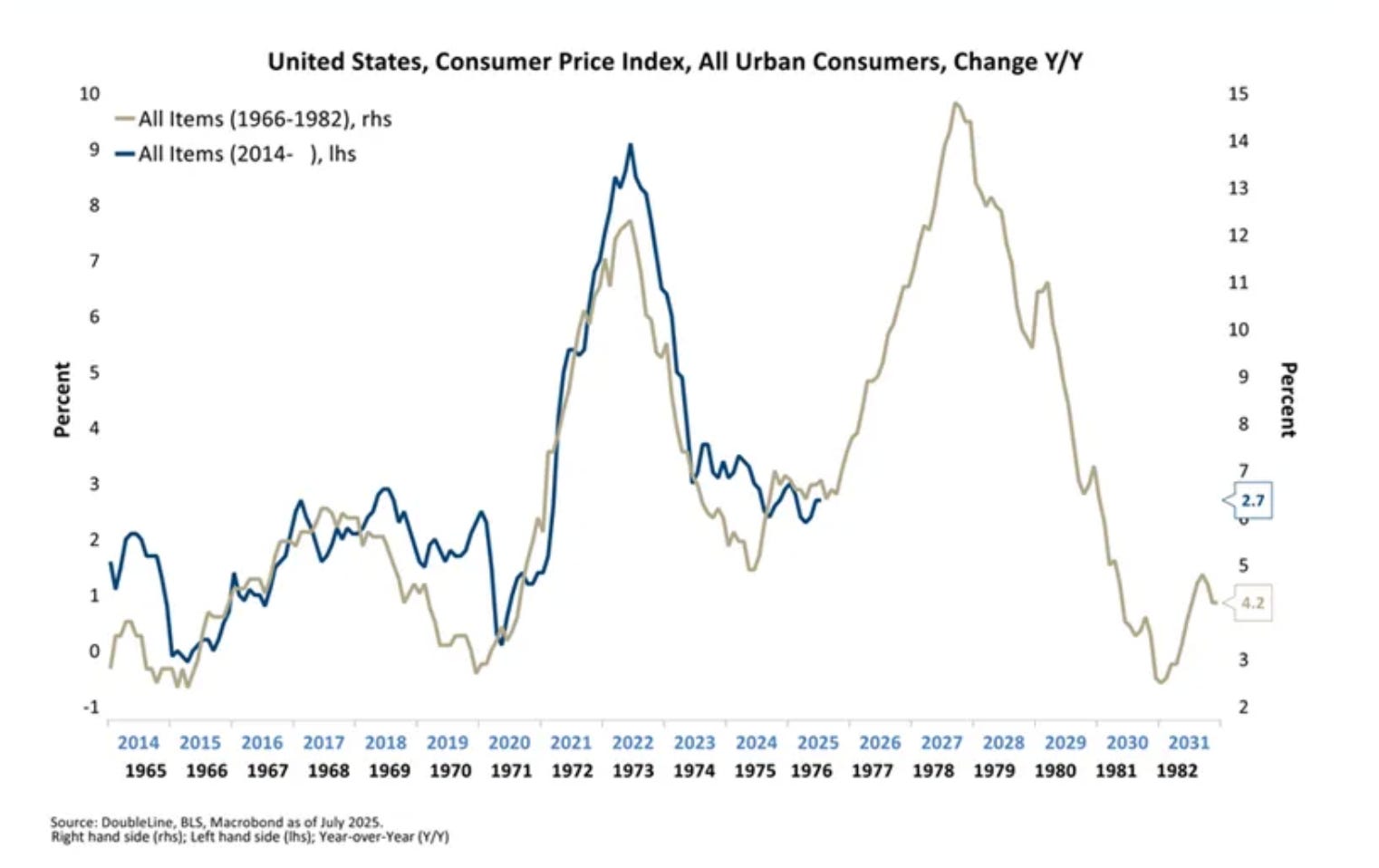

After watching Jeffrey Gundlach’s presentation, I dug up this chart from one of his previous presentations. Luke Gromen sums up the Trump/Fed drama in:

This fight is not about Fed independence; at its core, it is because the US debt and fiscal situation is going critical and neither the Trump Administration nor the Fed want to take the blame for what comes next.

Which is monetisation of US deficits i.e. print the difference while inflation rips.

Commodities are sniffing out this inevitability one by one.

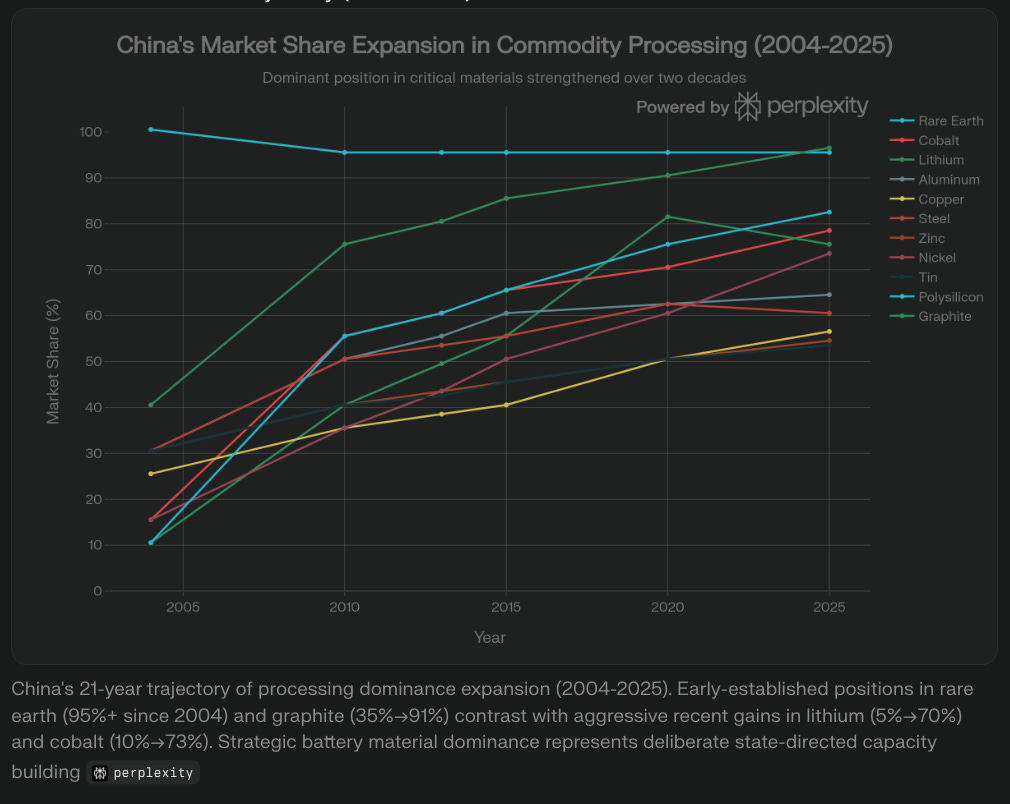

Something I’m Pondering

I’m pondering how many times I’ve read “excess capacity” in articles relating to China when what was really happening was China strategically undercutting global competitors to gain market share.

Craig Tindale touched on it in this piece, with the Quantified Asymmetry Between Market‑Led and State‑Directed Systems.

Take the chart below of China’s market share of processing across multiple commodities.

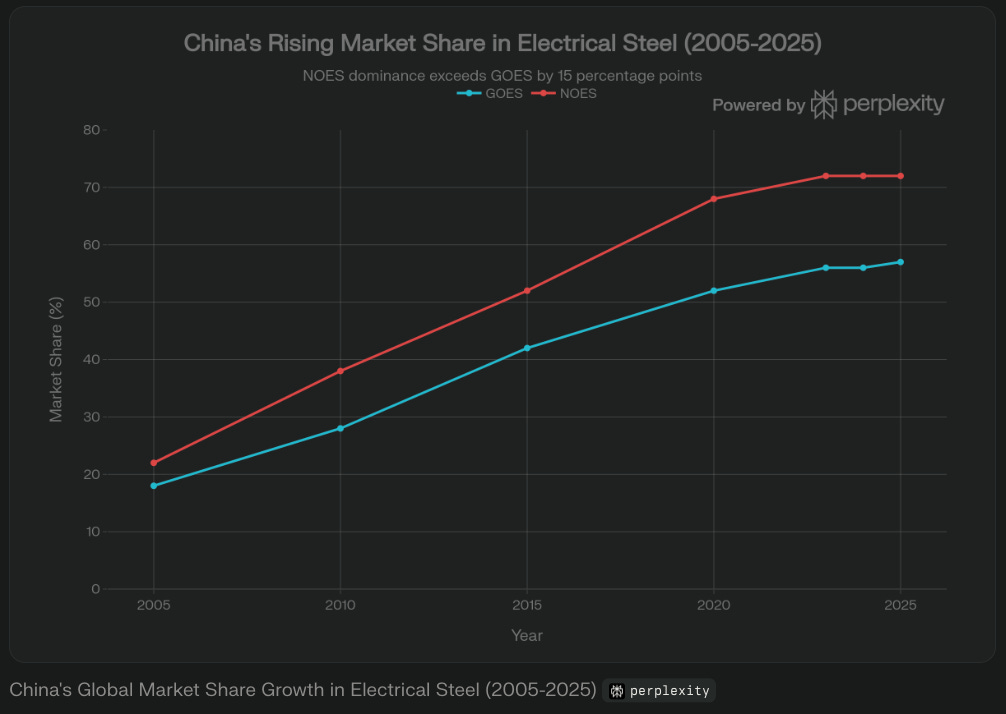

An example is 3-5 years transformer delays from where China isn’t cited as the main constraint with Siemens Energy, GE Vernova, Hitachi Energy, that is, until you peel back a layer.

Manufacturing facility limitations (40-50% of delay)

China represents approximately 60-70% of the "manufacturing facility limitations" constraint that causes 40-50% of transformer delays.

Specialised skilled labor shortages (20-25% of delay)

Copper windings sourcing and cost (10-15% of delay)

China represents approximately 30% of the “copper windings sourcing and cost” constraint.

Grain-oriented electrical steel (GOES) and tariff uncertainty (15-20% of delay)

China has dominant market share in both GOES (56%) and non-oriented electrical steel (NOES) (72%).

With any reshoring plans, it’s going to be a “blend of constraints”, be it skilled labour, manufacturing/processing, critical minerals, or energy.

None of which you can financialise your way out of.

I hope you’re all having a great week.

Cheers,

Ferg

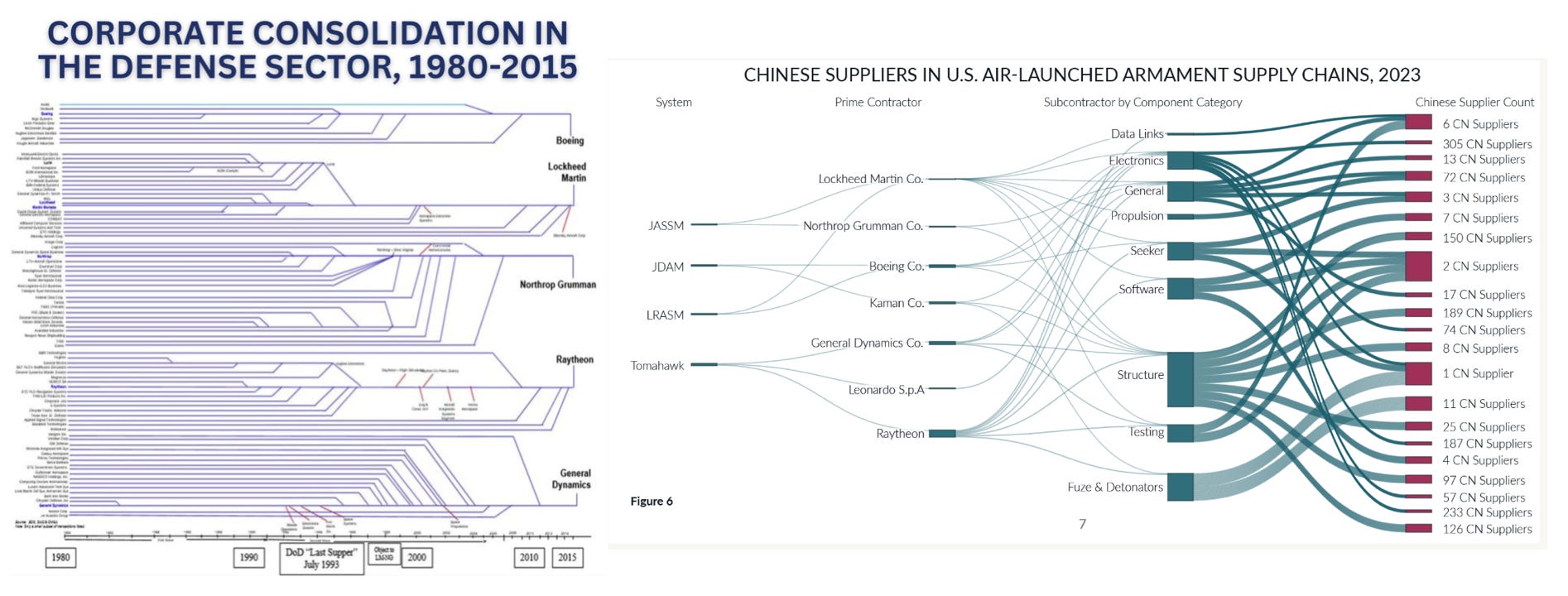

P.S. One of the more striking visuals is how the US defense sector consolidated into a few names while at the same time outsourcing the supply chain to China.

I wrote this piece to outline a few of the rules I stick to religiously to protect myself from a dose of FOMO…

Ferg-

I keep having a hard time balancing some "data streams" and opinions on the PRC. Yes, it is a bottleneck, and the sole source of entirely too many things. Great prospects for a rising future, etc. On the other hand, I see a tottering dictatorship undergoing a demographic implosion, exacerbated by an economic situation that makes frontier markets look like a safer bet. Maybe both are happening at once.

I am relatively certain that globalism (in its current form) is fading fast, and I suspect we are seeing the re-emergence of mercantilist trading blocs. This is leading me to "1% positions" in very scary places and things, and your output is extremely useful for this.

Thanks--

Rick

Great reminder re: China.

And when it comes to China strategically undercutting global competitors to gain market share, industries are often clustered city by city, which makes their supply chain SO much more efficient. Competition is brutal, which makes the best truly the best.