Why Energy is a Fat Pitch here

Writing has often helped me clean up my thinking on a topic, so I’ve decided to dust off the keyboard. It’ll mainly be broad energy/oil today, and then I plan to revisit coal and offshore oil over the next month.

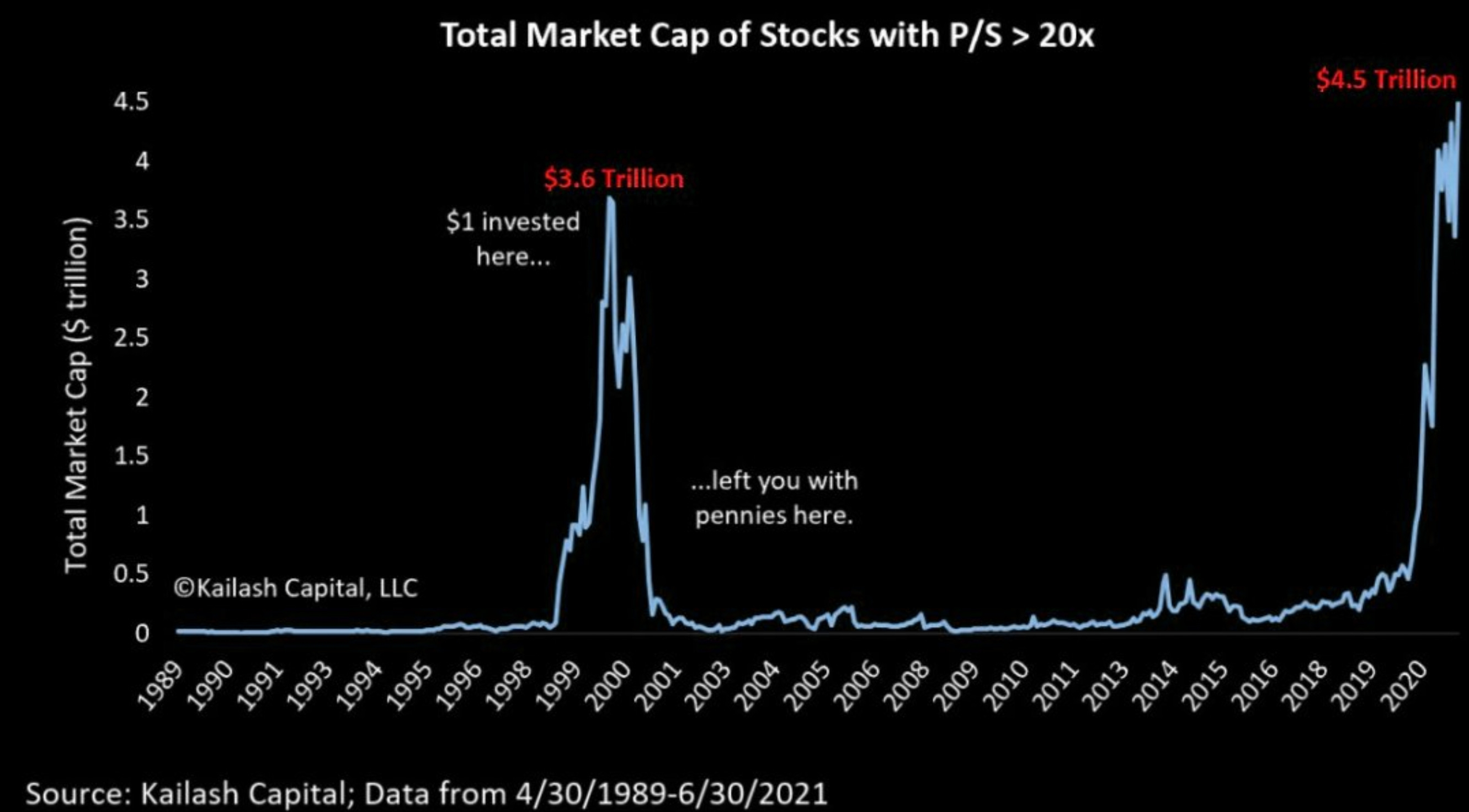

Over the last decade of abundant energy, low inflation, and easy money, anything that could provide growth was priced to perfection hallucination.

But then again, what did we expect handing out free money to a generation getting their financial advice from TickTok.

My bet is the decade ahead will be the polar opposite, with scarce energy, high inflation and tight money. The sectors that will outperform are those that were starved of capital yet are essential to humanity’s progress. Energy and progress go hand in hand, or as Vaclav Smil put it:

“To discuss energy and the economy is tautology”

Knowing where we are

One of those most important things is knowing where we stand in the cycle. I don’t believe in forecasts. We always say, “We never know where we’re going, but we sure as hell ought to know where we are.”

-Howard Marks

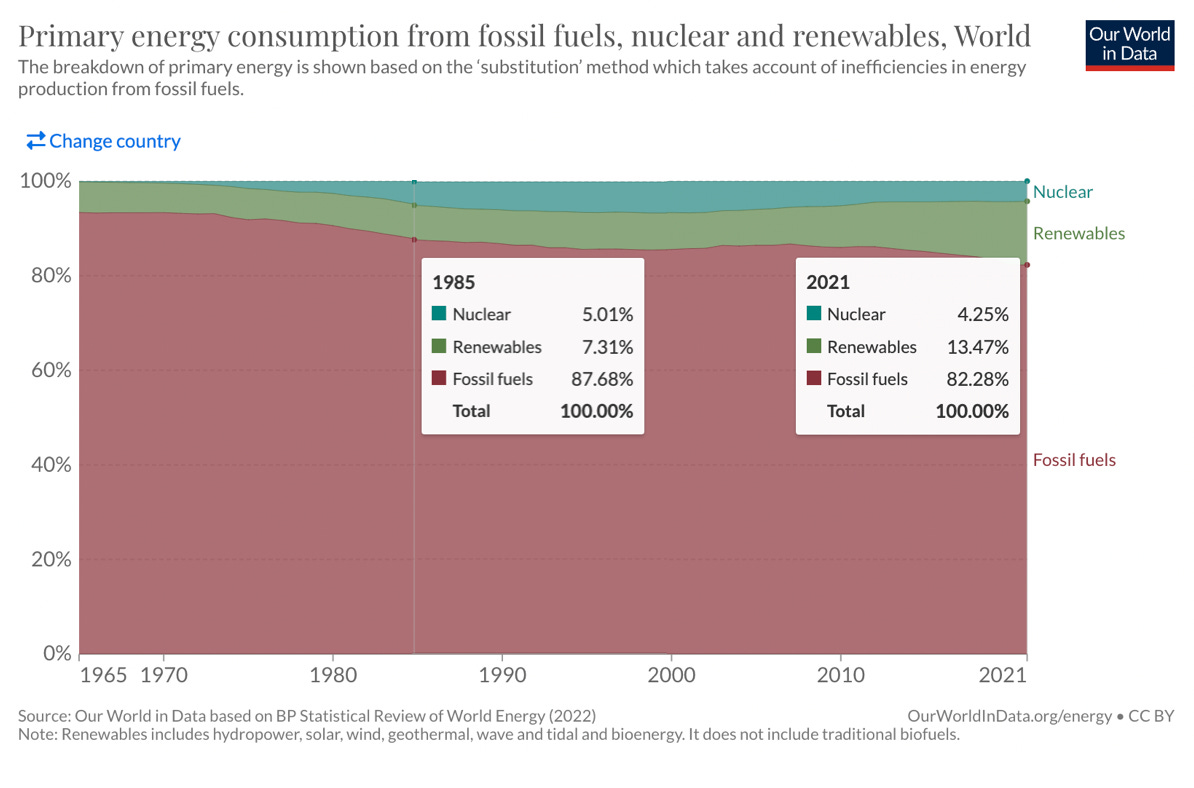

Knowing where we currently stand with global primary energy is important since the numbers we are fed often play to a narrative.

Take these examples of misdirection:

Showing the percentage of electricity consumption vs primary energy consumption (electricity is 20.4% of primary energy consumption).

Showing percentage growth instead of percentage of the total.

Using LCOE (levelised cost of energy) instead of fully integrated cost (storage, distribution, balancing etc.)

It's rare to see the primary energy system displayed clearly, like the below chart, since it shows how little things have changed over the last few decades.

Breaking it down further, the “transition” is based on wind and solar, which represent 4.63% of primary energy and have been a complete failure for those that have aimed to run their grid on them, i.e. Germany and California.

The person who has explained this best is Lars Schernikau (who I interviewed here). Yes, Germany, at a massive cost, has added +93% to their net power generation (55% wind & solar), yet when looking at gross power production, it has barely increased at 1.8% due to the low capacity factor of wind and solar.

Now that I’ve illustrated, we live in a fossil fuel-dominated system and will, for the foreseeable future, we can dig into how the supply and demand currently stack up.

Supply

For now, I’ll mainly focus on oil which is the master commodity that feeds into everything else (I do plan to do an update on this coal article I wrote at the start of 2021).

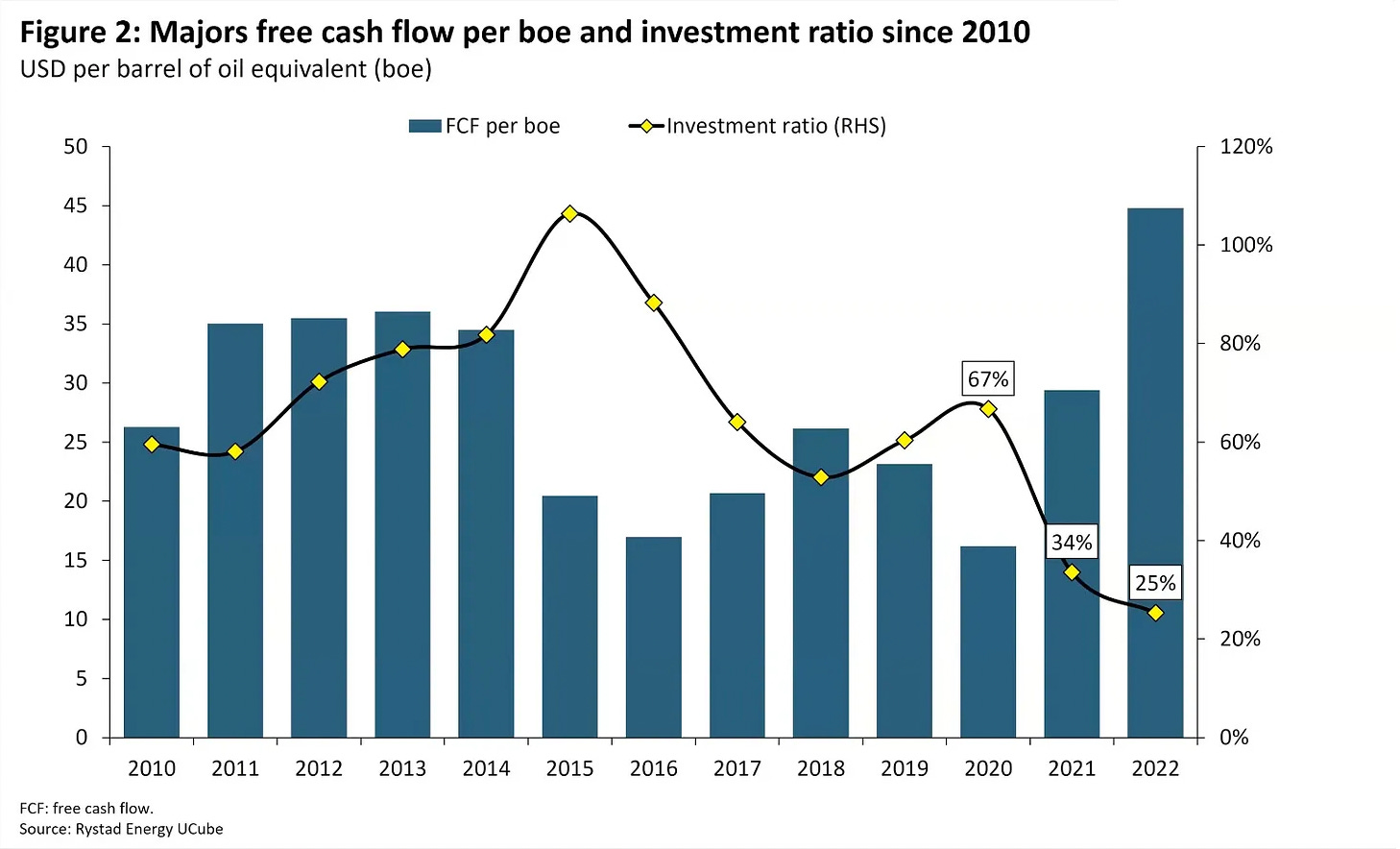

We currently find ourselves with the highest free cash flow per boe since 2010 and the lowest investment ratio on record.

Starving the sector of CAPEX means we are facing steep decline rates moving forward, with oil forecast to drop 70% and natural gas not far behind it at 60% over the next 20 years.

This is way in excess of what even the most fanatical transition junkies have projected.

Projections for how we plug this gap have largely leaned on shale extrapolations. This extrapolation has taken a severe beating as the shale space struggles to maintain production with DUCs (drilled but uncompleted) wells having been worked through and the majority of the tier 1 assets having been high-graded.

This leads to my bullish argument for offshore, which makes up ~45% of the oil major’s proven liquid reserves, but I’ll leave that for another post.

If we dive into petroleum inventories, it’s the same story.

Demand

The demand story is fairly straightforward in that we in the developed world consume the equivalent of 13 barrels per person per year. While the developing world consumes 3 barrels per person per year (and makes all our stuff with that).

Even if they kept the status quo for 3 barrels per person per year, there will be two billion more people in developing countries by 2050, which adds 50% to the energy system. Assume developing countries increase to 4 barrels per person per year and the energy system doubles.

Now take this observation and scroll back up to compare to the oil and gas supply declines, and you will see what a pickle we have got ourselves in.

It also doesn’t help the IEA is in persistent denial of developing countries’ effect on oil demand, as can be seen from the below chart. If you thought they’d have figured this out by now, you’d be wrong.

There is also the inconvenient fact that oil is the master commodity, and the transition will increase demand due to the need to dig a heap of stuff up.

Lastly, EVs only make up 1-2% of the global fleet and passenger vehicles, in turn, only make up 27% of oil demand. EVs hit 10% of global sales last year, meaning 90% of passenger vehicles sold are still ICEs with a minimum life expectancy of 15 years. Even if you assume 100% of cars sold from now on are EVs, it doesn’t move the needle for a long, long time.

Timing

The next question is timing, as there are plenty of compelling supply-demand imbalances in the commodity market, be it gold, copper, uranium, etc. As Howard Marks likes to say;

“Being too far ahead of your time is indistinguishable from being wrong.”

One of my favourite pieces of research on this issue was from Wesley Gray

Retail investors are often sold the fantasy of out-performance with low volatility. In reality, out-performance goes hand in hand with higher volatility; it’s the price you have to pay.

One of the few time-tested ways to manage timing and volatility is to scale into a sector slowly. This helps lessen the chances of the kick in the nuts from building a position only to see it draw down heavily from what you thought was a great entry. Slowly allocating capital also has the benefit of the optionality of increasing allocations if you have a liquidity event or something similar (think March 2020).

Another approach to timing is when you witness a cyclical sector go through a bankruptcy cycle. Offshore services are the most recent example, with one needing to wait for relistings and assess the attractiveness of the company post-restructuring. For a case study, here is a video I did on Diamond Offshore post-relisting and the aftermath of it relisting.

How to play it?

For oil, there are three separate vehicles for playing the theme as I see it.

Playing the oil directly (An example being CL WTI future options on the NYMEX).

This is appealing as it removes the operational and jurisdictional risk of investing in oil companies. You side step, nationalisation risk, profit taxes, cost inflation, dumb management, dilution, etc. If anything, you stand to benefit from many of the above risks materialising as they will ultimately contribute to a higher oil price.

Oil being in backwardation makes this trade attractive as WTI is as priced in the low sixties going out a year or two, so you get substantial leverage if oil trades up to $100barrel + range over the next two years, which is hardly a stretch.

The cons of playing oil directly are the technicalities of dealing with futures and future options for the average investor. Also, having a set expiry and the risk of the options trading below that point at expiry leads to a complete loss of capital need to be considered. There is also a valid argument that quality companies stand to outperform the direct commodity over time and provide a wider margin of safety.

Producers (Majors right through to small oil sands plays).

This area has been trickier, with shale being a dumpster fire for shareholder capital up until recently and the oil majors being commandeered by Green activists. That said, it was one of my big regrets not diving into oil sands plays in a big way in 2021. Those with low-decline assets will be absolute money printers over the next few years. The tough part, as with all commodity companies, is having the know-how to wade through all the sub-optimal projects and snake oil.

Oil Services (Rigs, OSVs, Sesmic, and Engineering)

Services are easily the most hated corner of the oil market, for good reason, following a bankruptcy cycle that saw equity holders wiped out and debt holders equitised. These two charts tell the story of $20B of debt evaporated and sector consolidation from the 15 below companies into four (this chart was published before Seadrill relisted and acquired Aquadrill).

Needless to say, this sub-sector has been where I’ve focused the past year and been allocating new capital. Many names have only recently started to move, with there being some crazy in the micro-cap (<$300m) market cap space that are off 99% of investor’s radar.

A lot of it is hunting out the below chart pattern, ensuring there is a decent margin of safety with either cash or assets trading for cents on the dollar, and then joining the insiders and deep value investors buying these companies (as they are too illiquid for funds and institutional money to touch). A bonus of being illiquid is they are largely uncorrelated to the broad market or even the energy sector since there is no retail presence.

That’s a wrap for now; I do plan to revisit the offshore thesis in more detail as offshore is where future oil supply growth will have to come from, with the services being the major beneficiary with all the consolidation and restructurings positioning them for a great few years of outperformance.

Cheers

Ferg

Thanks Ferg, great to have your thoughts in extended written form to contemplate as a complement to your awesome content on Crux / Opens. Will look forward to the next write ups.

Cheers, Chris

Great write-up Ferg, thank you!