I always try to simplify things as much as possible in the portfolio, as from experience, the more complex an investment thesis, the more likely I’ll screw it up.

I loved Lyn's piece, Three Things Never to Fade, as an example of this. She always ensures she is on the right side of these three things when investing.

Thing 1: Energy Density

Thing 2: Computation

Thing 3: Network Effects

I’ve spilled a lot of digital ink on the energy density side of things (coal, uranium, and oil), which dominate my portfolio.

Humanity has progressed by climbing the energy density ladder, and the current deviation to lower energy density will be seen as a misstep in history.

I've got all the energy density exposure I need, even too much, judging by last year's performance.

Computation and Network Effects

I'd largely neglected them in the portfolio, as every man and his dog were aware of how powerful they are and had assigned valuations that reflected this.

Well, up until February 2021, that is.

It’s wild when you consider an equal investment at the start of 2012 would have had you sitting on a 400% return in both Chinese and US tech by 2021, yet 4 years on there is a 700% difference.

Prior to 2020, US and Chinese tech moved in lockstep with a correlation of 0.8 (which now stands at 0.2 or essentially uncorrelated).

I wrote about this gap between Chinese and US tech here (Hated Tech?) Yet I still feel underexposed to this theme and that I made some mistakes in how I applied the trade, which I am correcting in this piece.

Is US tech superior?

Going back to the alien example, if you just arrived on the plant and reviewed US and Chinese tech objectively, is US tech really superior?

Higher multiples on earnings are usually justified via some mix of growth, profitability, and competitive advantage (moat).

Let me start with an example where none of these three are present.

Tesla

Tesla is being eaten alive in the Chinese market, which accounts for a quarter of their revenue. Breakingviews: BYD's outpacing of Tesla has only just begun.

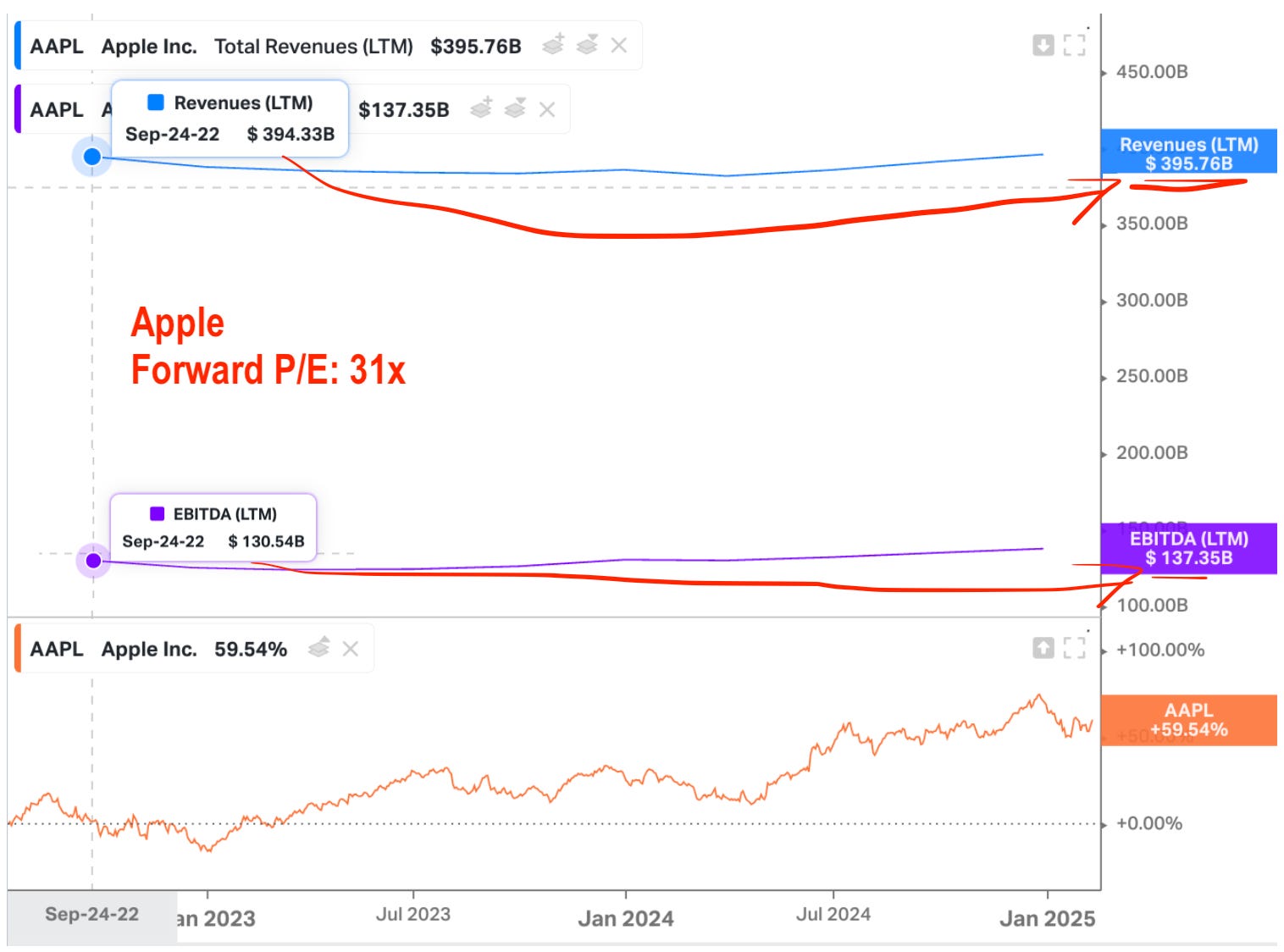

Apple

Apple is a great company; it's the growth part that's failing to show up (for a decade, this company traded on a 10-15 forward PE, now it's 31x forward PE with revenue and earnings having barely budged for over two years).

Competitive advantage (moat)

The problem with technology is that disruption is the norm.

There is nothing like a free, open-source model with comparable, if not superior, performance to get investors to ask the uncomfortable question.

Whats the return on all this AI CAPEX?

Sequoia had a crack at answering this.

September 20, 2023: AI’s $200B Question

June 20, 2024: AI’s $600B Question

I asked ChatGPT to read the article and estimate where this figure stands today (February 2025):

However, the corresponding revenue growth has not kept pace, suggesting that the current figure could now be approaching or even exceeding a "$1 trillion question." This reflects the critical challenge of aligning massive capital investments with actual revenue generation in the AI sector.

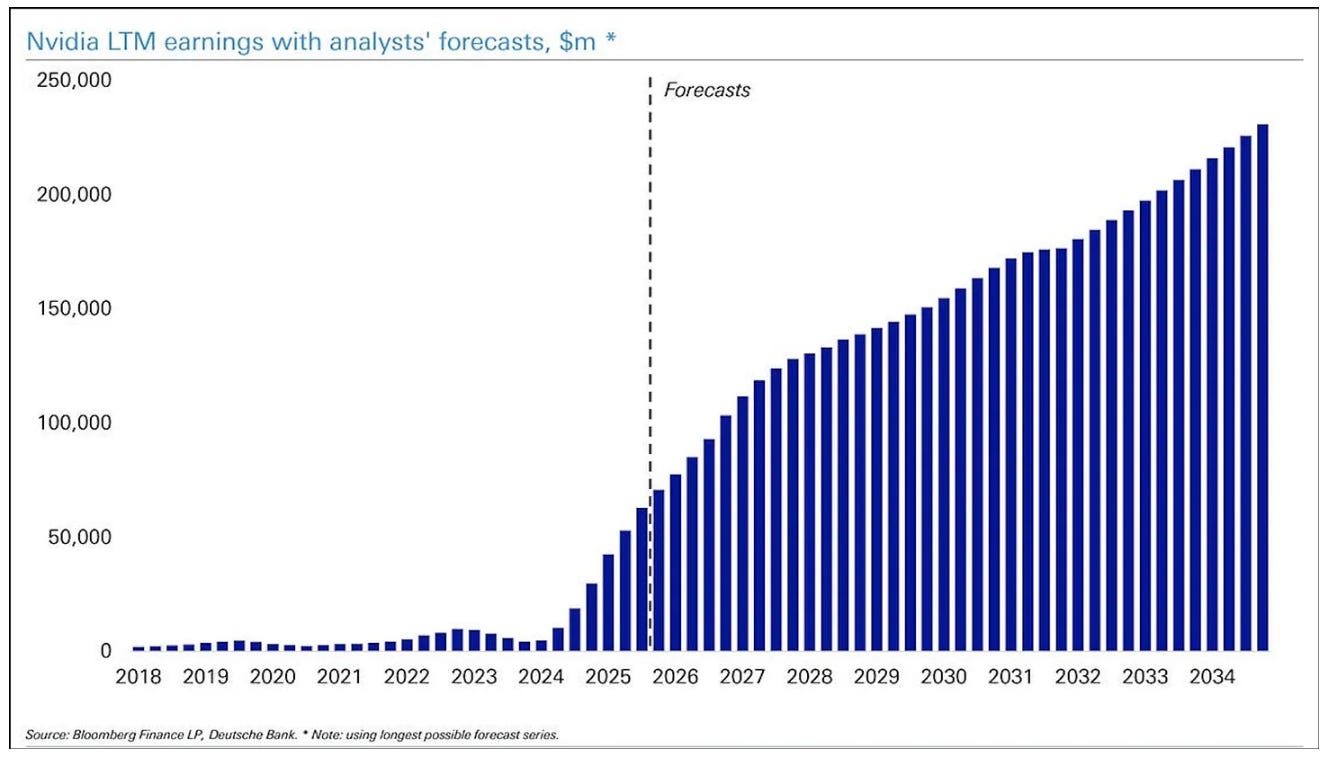

Which is how we end up with this earnings forecast.

Amy Hood, Microsoft’s CFO, shed some light on Microsoft’s expectation of return on its current AI expenditure:

“May take 15 years or even longer to obtain returns.”

Which begs the question: What if AI CAPEX is actually the cost of remaining competitive in their core business?

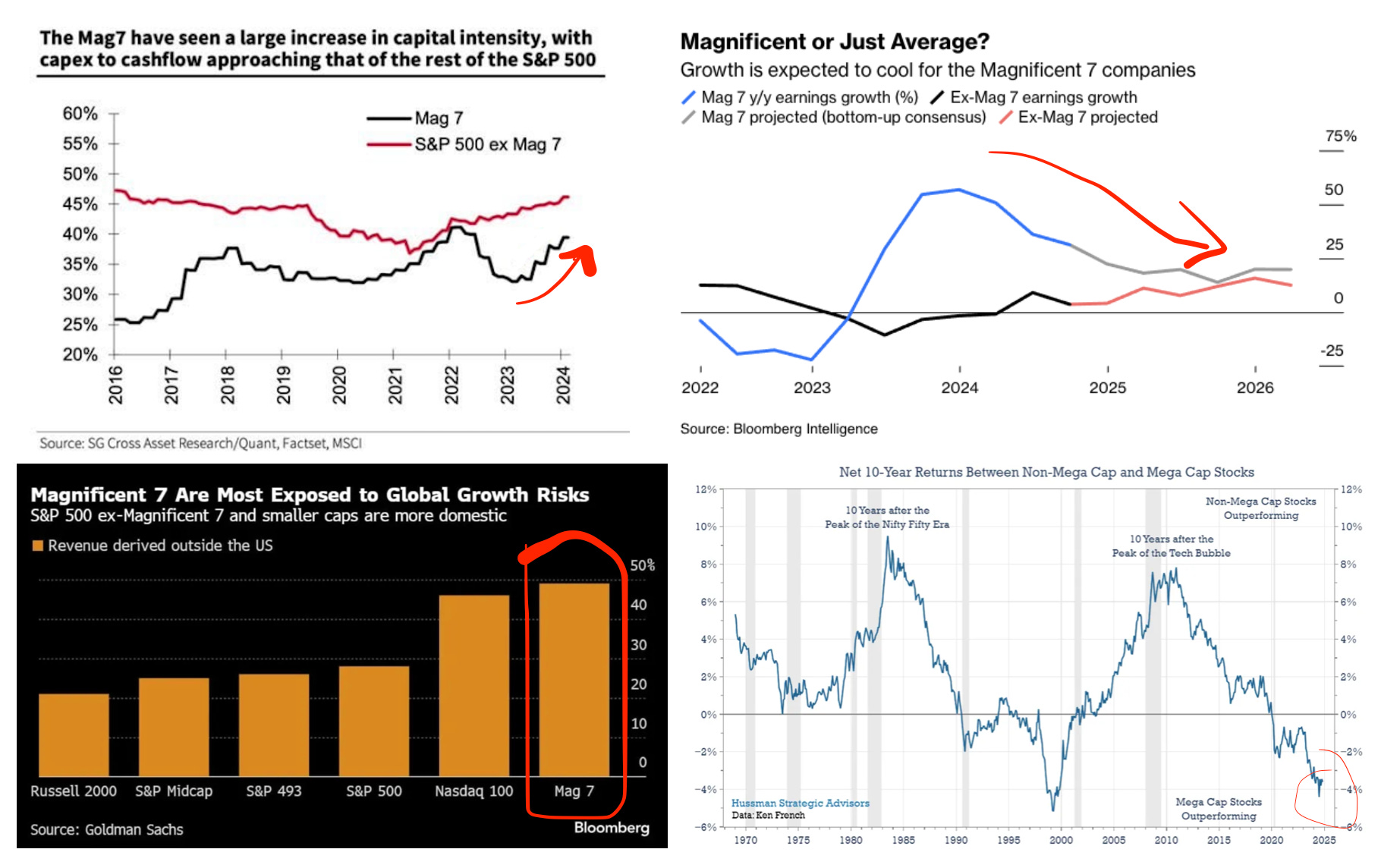

However you cut this looks all risk and no reward to me for the Mag 7.