Ferg’s Finds

This is a short weekly email that covers a few things I’ve found interesting during the week.

Article

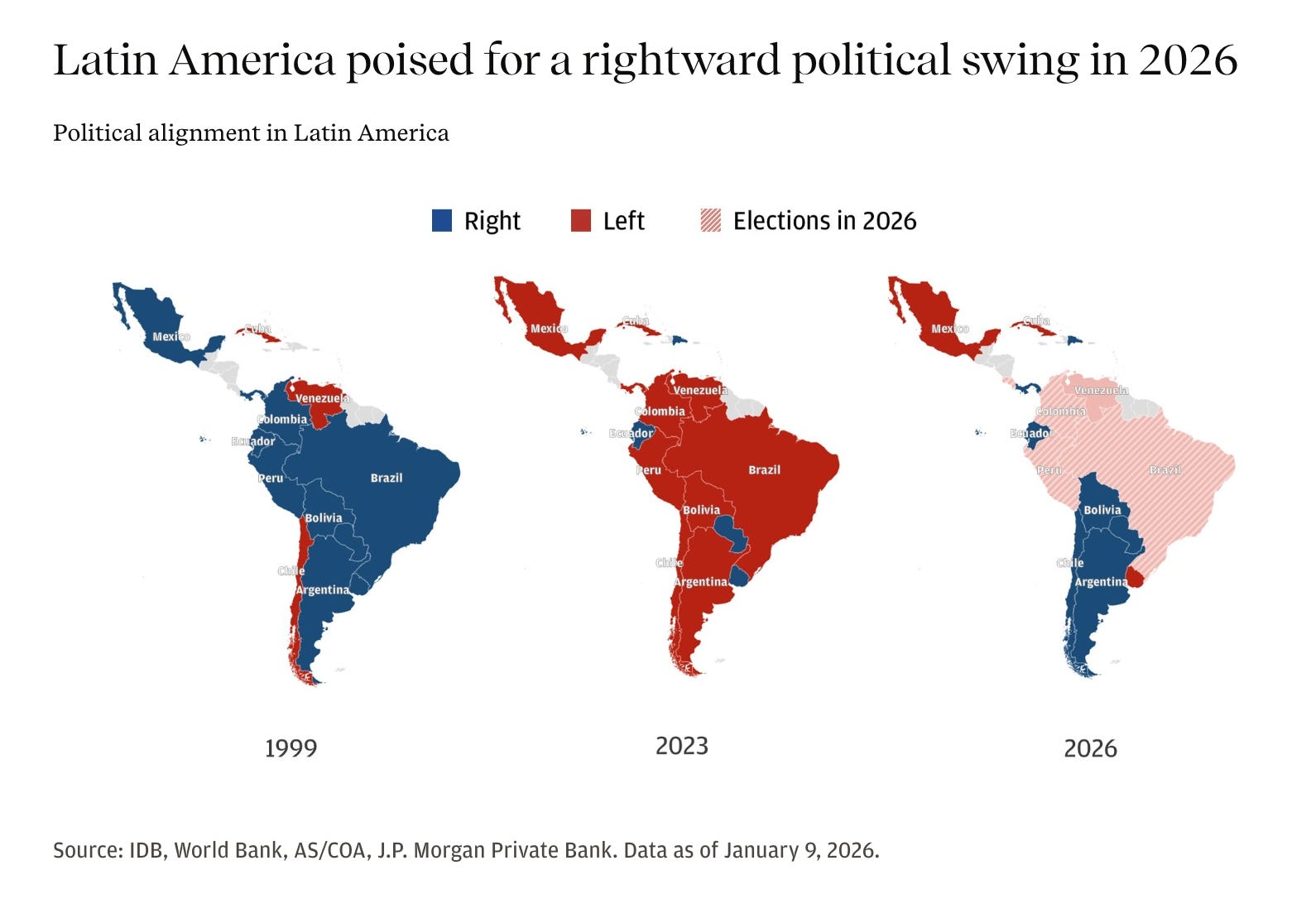

JPMorgan: Latin America in 2026: Between promise and pressure, the answer is optionality (Jan 14, 2026).

I added current results to the JPM election table, which was published in January 2026.

Podcast/Video

I continue to be a big fan of Kevin Walmsley’s YouTube channel: Inside China Business.

Quote

“Rule No. 1: Most things will prove to be cyclical. – Rule No. 2: Some of the greatest opportunities for gain and loss come when other people forget Rule No. 1.”

-Howard Marks

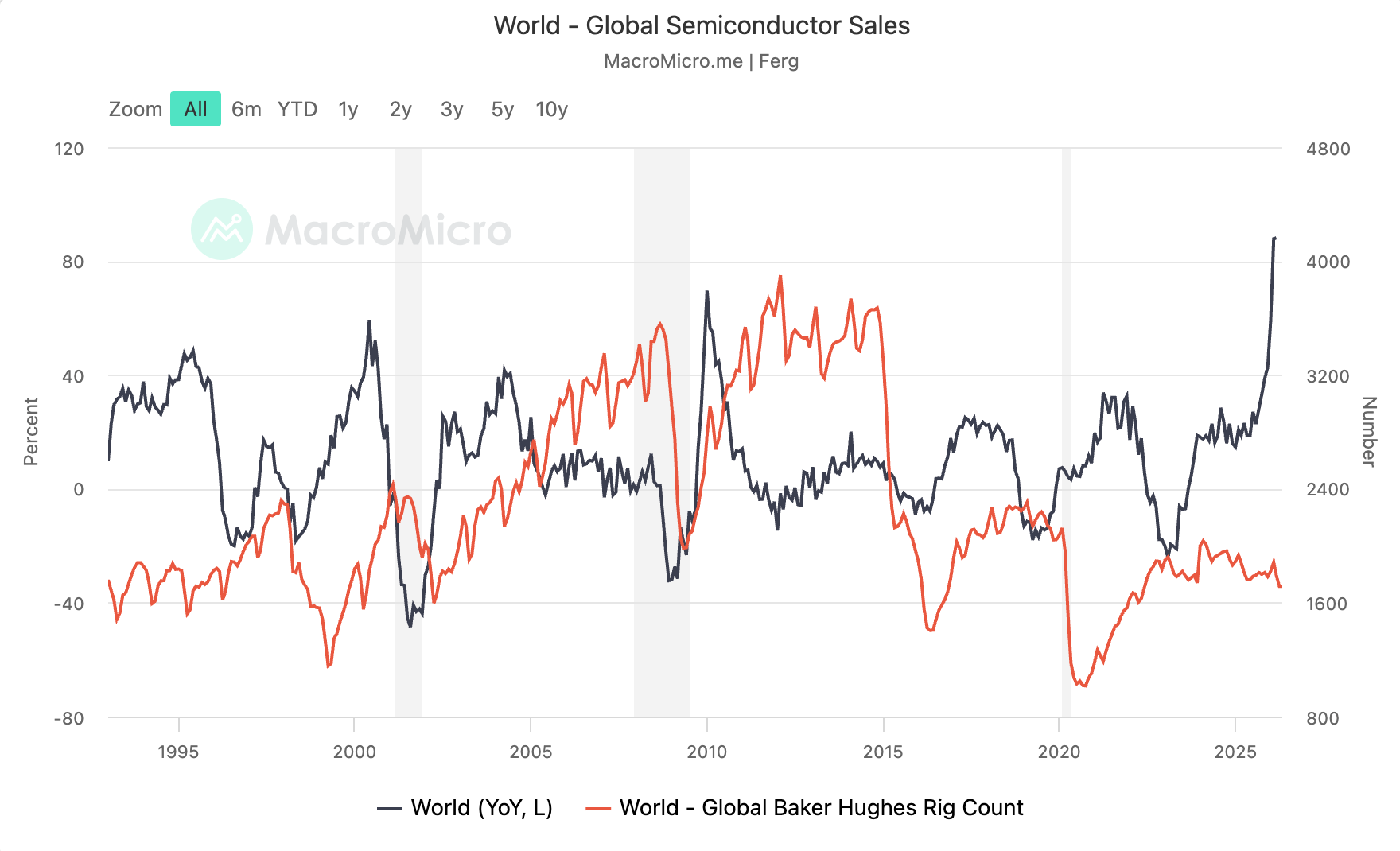

Charting semis against global rig count makes for quite the illustration of cyclicality.

On that note, Kuppy wrote a great piece on On Semis…

With this section hitting the nail on the head for me:

As my good friend Louis-Vincent Gave always reminds me, “when China enters a room, profits walk out.” I can think of dozens of such situations. Everything from steel to aluminum, from chemicals to solar panels, and shipbuilding to electric vehicles. China has historically followed a recurring pattern—they show up, they use cheap funding and they glut the industry.

Then once everyone’s margins (including their own) are deeply negative, they ramp capacity to many times global demand, before they break international players, yet their utilization levels continue to drop as they keep building even more capacity. It really is the runaway assembly line. I’ve seen this over and over, in dozens of industries. Over time, I’ve learned to get out of the way when China is coming for a sector, because they simply will not stop.

Interestingly, China has repeatedly told the world that they plan to follow this playbook in semis, yet the world seems oblivious to the danger. Some seem to doubt that China has the technological knowhow (they said the same about EVs, but have you driven the newest BYD??). Some say that the West will never transfer the technology—have you seen China respect patents?? Some just think that semis are somehow special. I can assure you they’re not any more special than solar panels were. The Chinese are coming, and the glut will be legendary. In my opinion, no matter how many datacenters get built, they will NEVER be able to absorb the coming supply.

Tweet

I’d always figured PE/multiple compression would be on the back of structurally higher inflation. Lyall Taylor wrote a great piece on it a few years ago: Why P/E multiples are (justifiably) lower in periods of high inflation.

It’s interesting to consider whether AI disruption could have the same effect or deliver a one-two punch with inflation.

Here is a scenario worth taking seriously: AI lowers the cost of disruption so dramatically, and raises the pace of innovation so relentlessly, that no company can credibly project its free cash flow beyond five years. Because, in the time you use AI to disrupt an incumbent, someone is laying the foundation to use a better model to disrupt you.

Charts

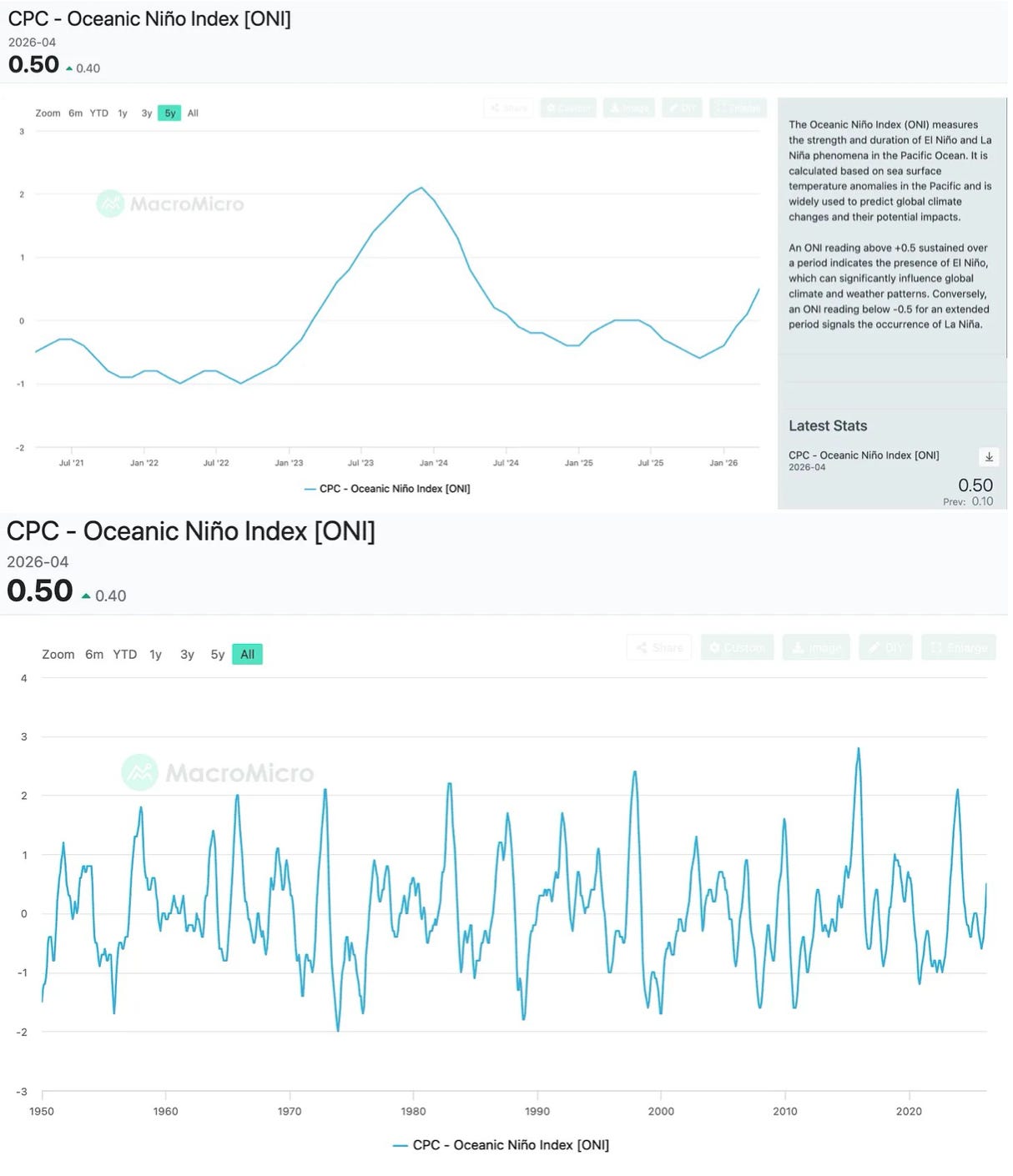

I was looking for a way to track the “Super El Niño” and came across this Oceanic Niño Index, which, while only reporting monthly, is now breaking out (yeah, it’s noisy, but it tends to trend when looking at its history).

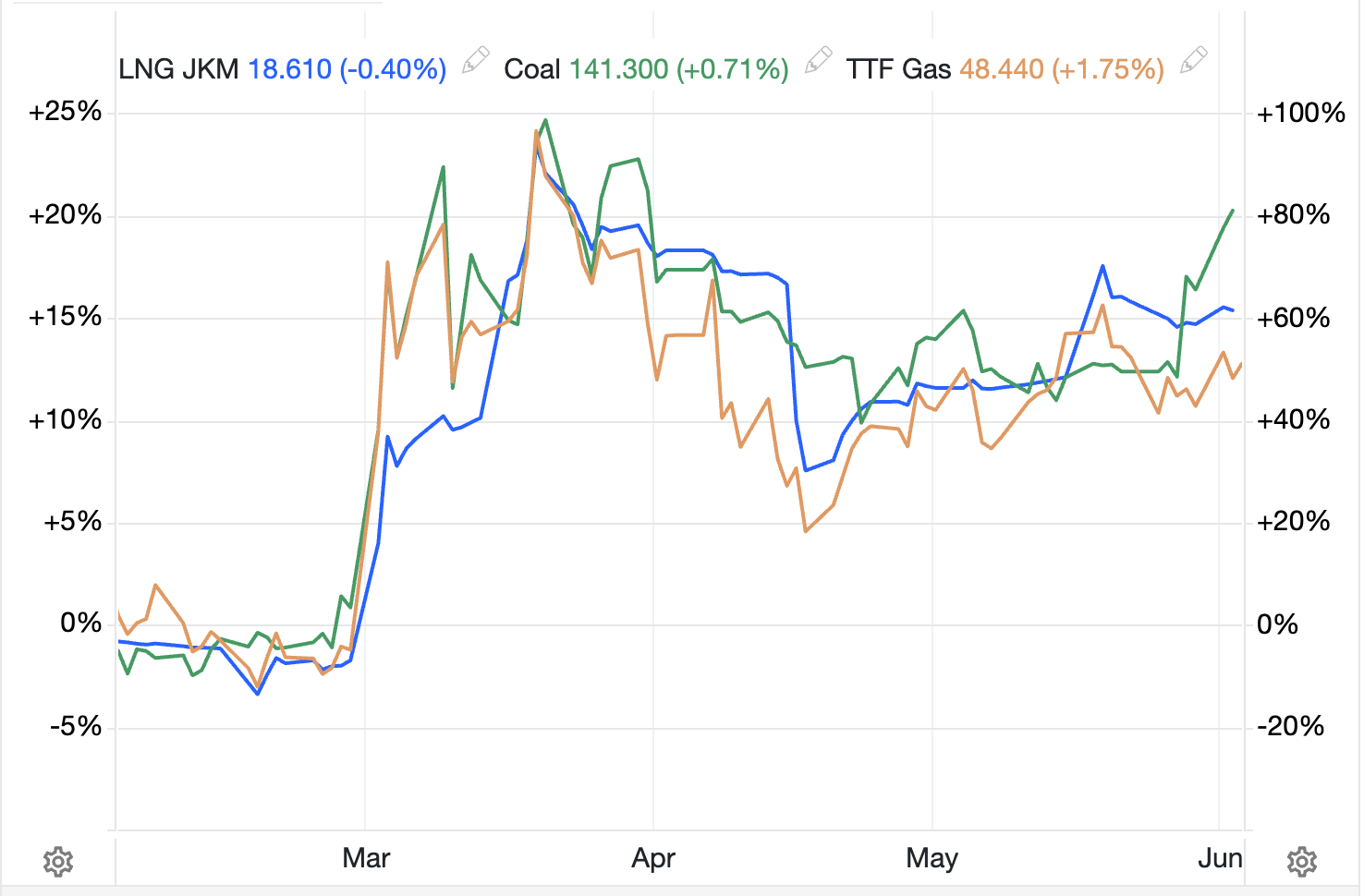

I remain a thermal coal bull here as we head into peak Asian cooling demand with Qatar LNG still offline.

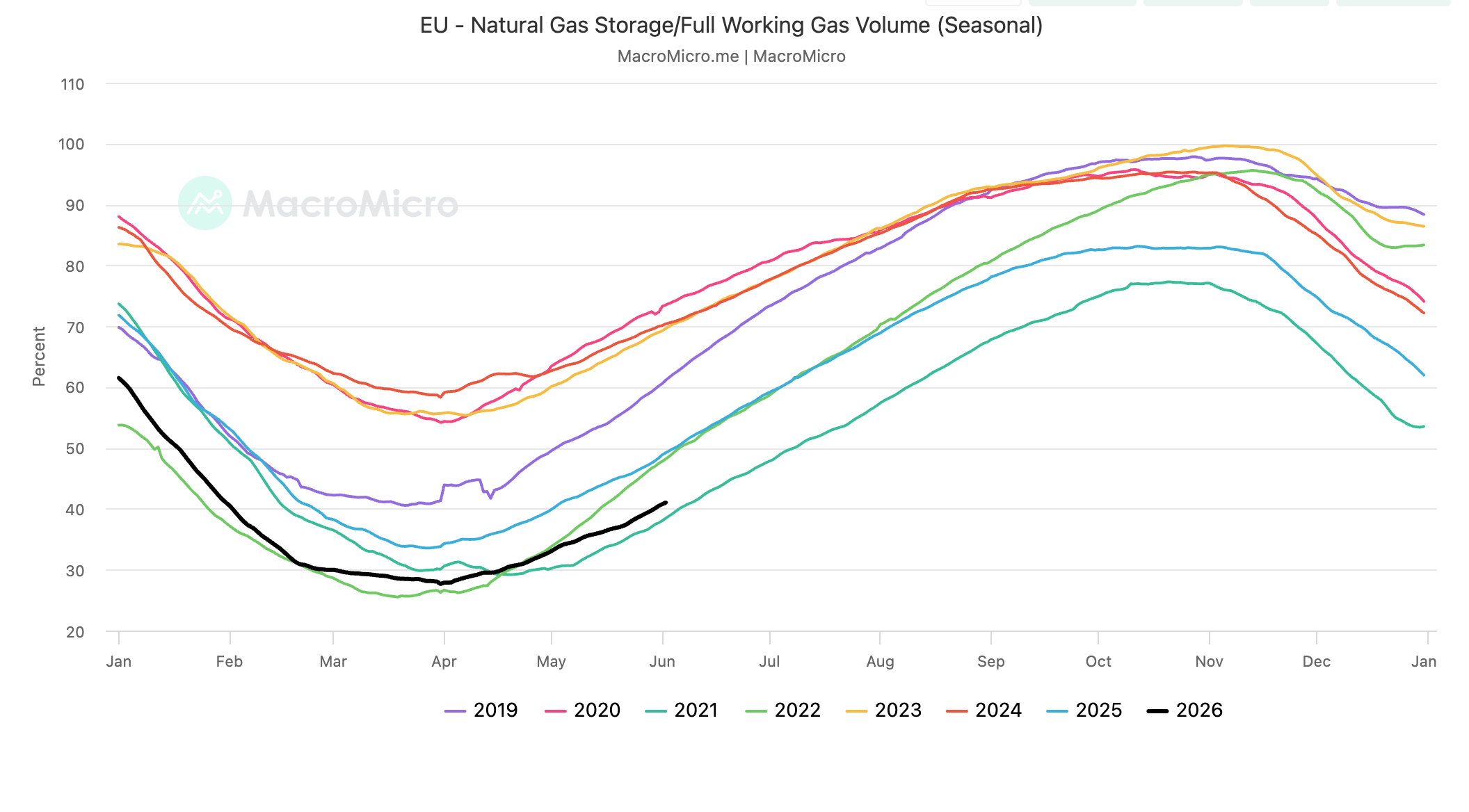

The EU gas storage is tracking the 2021 path, and that isn’t going to change unless they start outbidding Asia for destination-flexible (US) LNG.

Something I’m Pondering

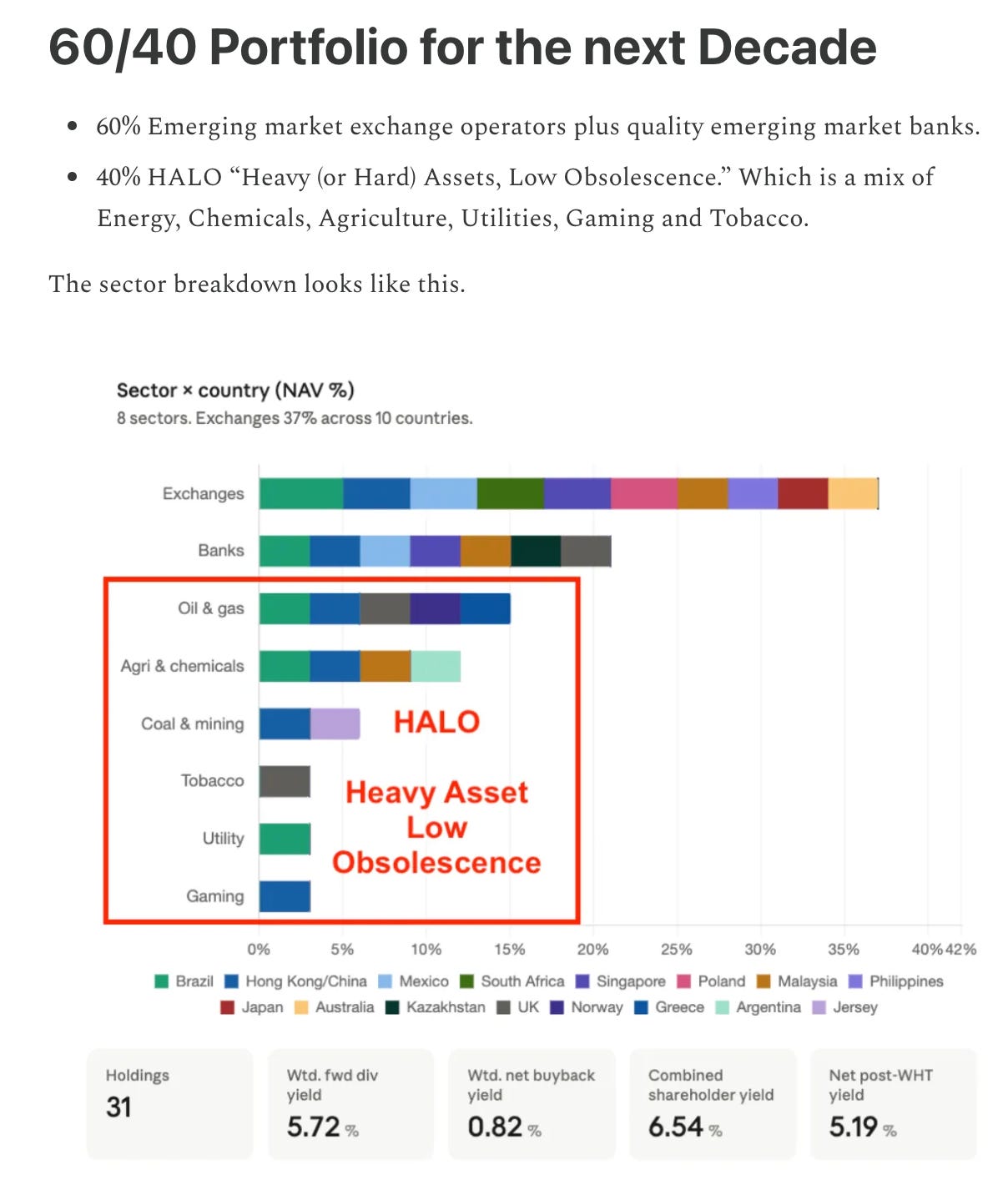

I’m pondering how it is easier to avoid “disruption” by buying sectors where consensus is that the sector is in terminal decline and will never achieve any multiple expansion, despite solid cash flows, i.e., coal and tobacco.

I’ve spilled a lot of digital ink on why this isn’t the case with coal, namely, China being in the process of adding 17-40% to its existing coal fleet.

China’s coal fleet is all but guaranteed to grow 17% by 2029, probably 23% with permitted projects and possibly 40% if planned plants are permitted.

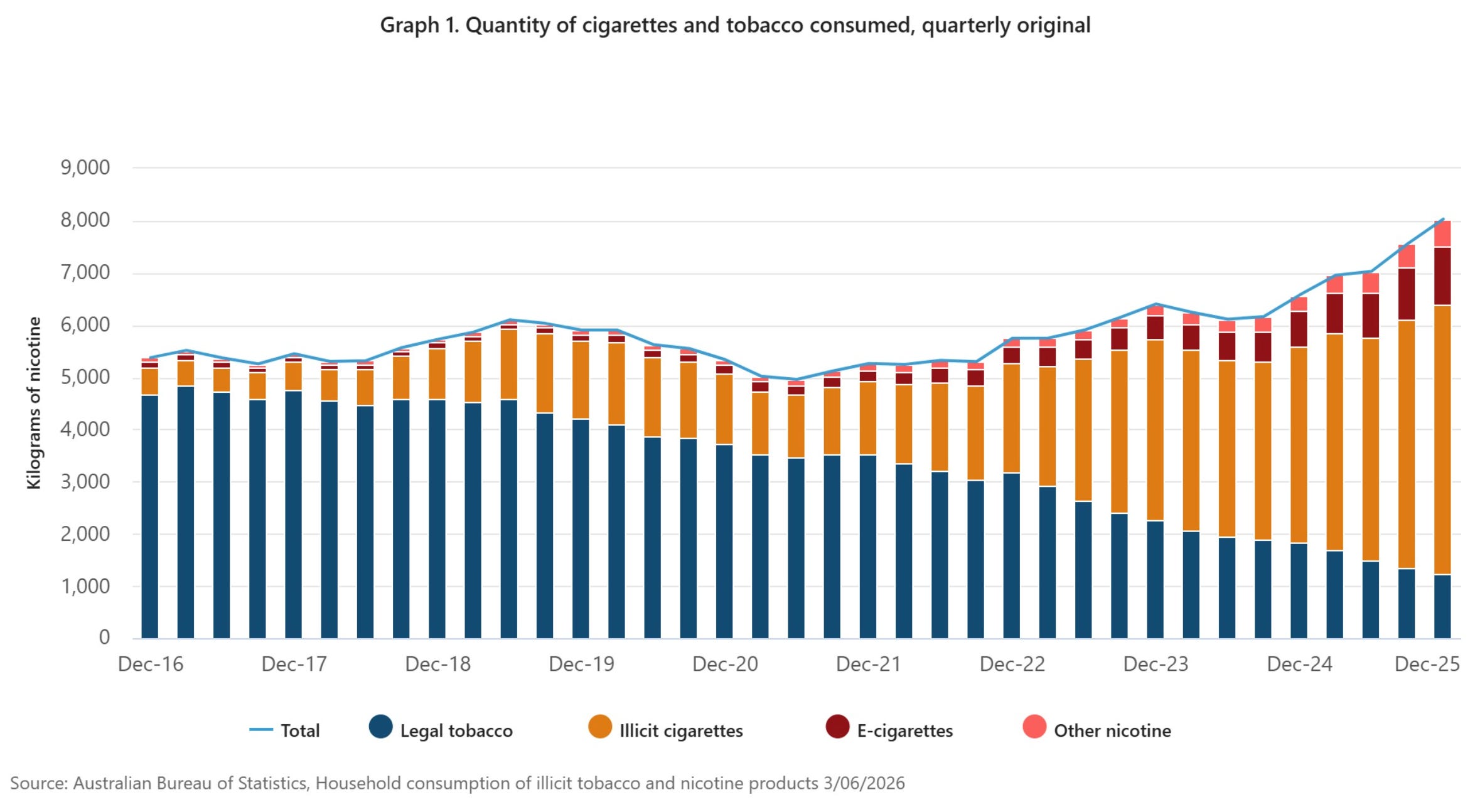

I’ve never spent any time looking into tobacco companies (up until I bought one for Hugo’s portfolio), which is why the below caught my attention.

Having lived in Australia and seen how expensive cigarettes had got, I’d assumed they’d been successful in disincentivising tobacco consumption.

Apparently not: ABS estimates 80pc of tobacco consumed in Australia last year illegal amid ‘rapid growth’ in black market.

I dug up this old article Lyall wrote on tobacco, as I remember it being insightful and well worth your time.

The art of worldly wisdom, smoking, and British American Tobacco

Most developed markets have tobacco advertising bans. This means that it is almost impossible to launch a new, competing tobacco brand. In many countries, you are not even allowed to engage in display advertising at the point of sale (cigarettes sometimes even need to be hidden from view behind the counter). Customers therefore wouldn’t even know your new brand existed. Furthermore, because regulators want to reduce tobacco consumption, they are actually more than happy for tobacco companies to acquire each other and keep raising prices. Unlike most industries, antitrust concerns are therefore non-existent - quite the reverse. Meanwhile, the highly addictive nature of nicotine makes consumers not particularly price sensitive.

However, while all of the above is fairly obvious, it would be rendered irrelevant if smokers all just decided to stop smoking, or if regulators were to ban tobacco entirely, and it is the systematic over-estimation of these risks by investors that has driven the undervaluation of tobacco stocks over most of the past 30 years. This has allowed the companies to buy back tonnes of stock at cheap prices, or pay high dividend yields which investors have been able to reinvest at high returns (whereas most industries with great economics have traded at high valuations, preventing this opportunity).

Hope you are all having a great week!

Cheers,

Ferg

P.S. I finally pressed send on this piece!

Hi Ferg, loved your AMA again. Allthough I brought no question to the table, I want to echo your take on Shell. Plus I want to add something: They had an M&A with Arc resources that, in my opnion, is huge. You did not mention that in your ama but I do think that is important for future oil & natural gas production & trading of the company. On my own substack I wrote an article on it, if you like you can read it here: SHELL steps on the gas! https://investorassistance.substack.com/p/shell-steps-on-the-gas?r=2ovz6x&utm_campaign=post&utm_medium=web&showWelcomeOnShare=true

Do you think the rise of GLP-1s poses a unique risk to tobacco firms?