Ferg's Finds

This is a short weekly email that covers a few things I’ve found interesting during the week.

Article(s)

Charles Gave: Tariffs And The Platform Company Model

This process has probably only just begun, with the next logical step being to address the big internet firms. The same logic says these should be taxed not on the “profits” they make locally (they make none) but on the sales they make in markets like France, Britain and the US, even as the profits are booked to Ireland. A levy of 5-10% on such sales would seem reasonable.

This has significant implications when considering that the average tax rate across the S&P 500 (excluding Mag7) is 26%. The energy sector pays an average of 28% tax, and the materials sector pays 29%. The Magnificent 7 pays an average of 15% tax and has 50% of its earnings overseas. The trend has already started in France.

France Eyes US Big Tech in EU Retaliation to Trump’s Tariffs

French President Emmanuel Macron has previously flagged that while the US has a deficit with the EU in terms of goods, it runs a large surplus in services.

This also jogged my memory to hunt out this graph by Vincent Deluard, who pointed out the almost perfect inverse relation between companies' ESG ratings and their effective tax rate.

Podcast/Video

No one breaks down the current macro situation better than Luke.

Luke Gromen Sounds the Alarm of a Crashing Economy: Macro Update to Help Investors Prepare

Quote

In bull markets, the future gets a premium. In bear markets, reality gets a discount.

-Jim Chanos

Tweet

This diagram is the game at play now, and we will go around and around until the debt is inflated away. Great piece by Kuppy as well.

Charts

A lot of the stuff I've read lately underestimates how quickly China has been pivoting to BRI/emerging markets for exports and, by doing so, overestimates the leverage the US has in negotiations.

Which is why it’s been a focus of my writing lately.

A solid rule for the next decade is to invest along with Chinese capital flows or in things the Chinese need.

Something I'm Pondering

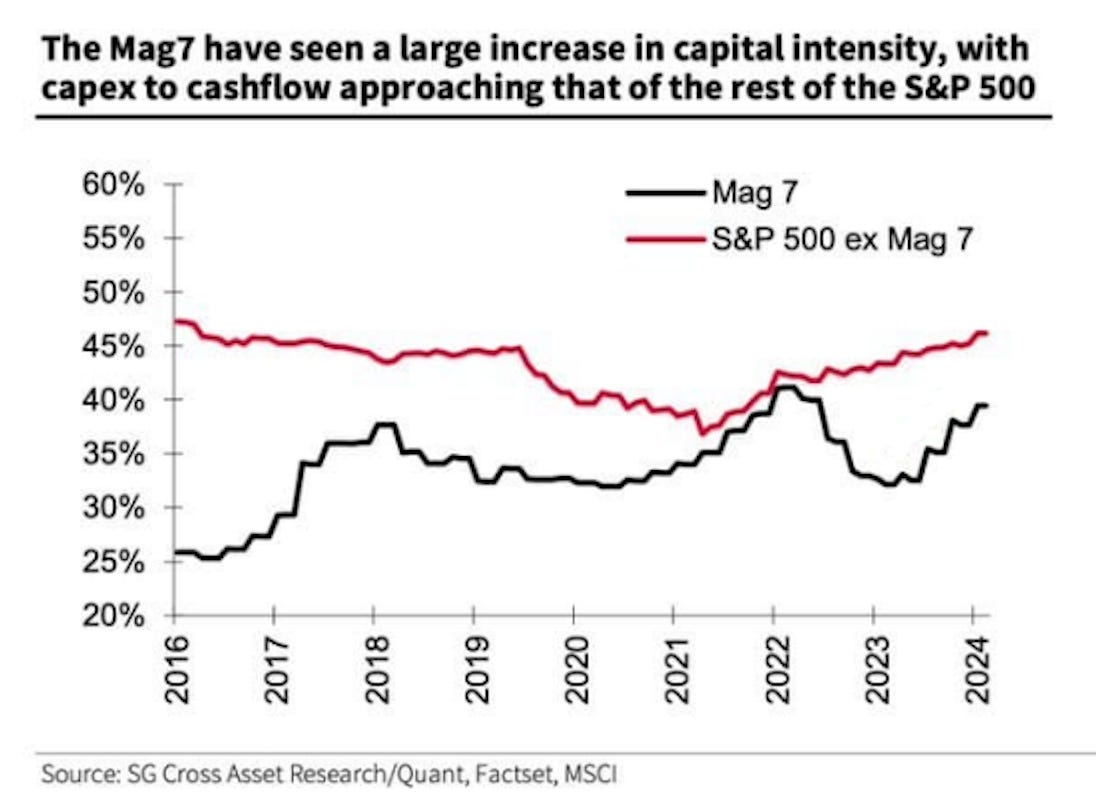

I’m pondering how many headwinds there are to many US companies' margins and their valuations as a result.

Those whose valuation reflects maintaining fat margins due to low taxes (think Mag7, which pays an average 15% rate and has 50% of revenue overseas).

Take the graph below. The S&P 493 has half the exposure that Mag7 has to global growth and trade war retaliation.

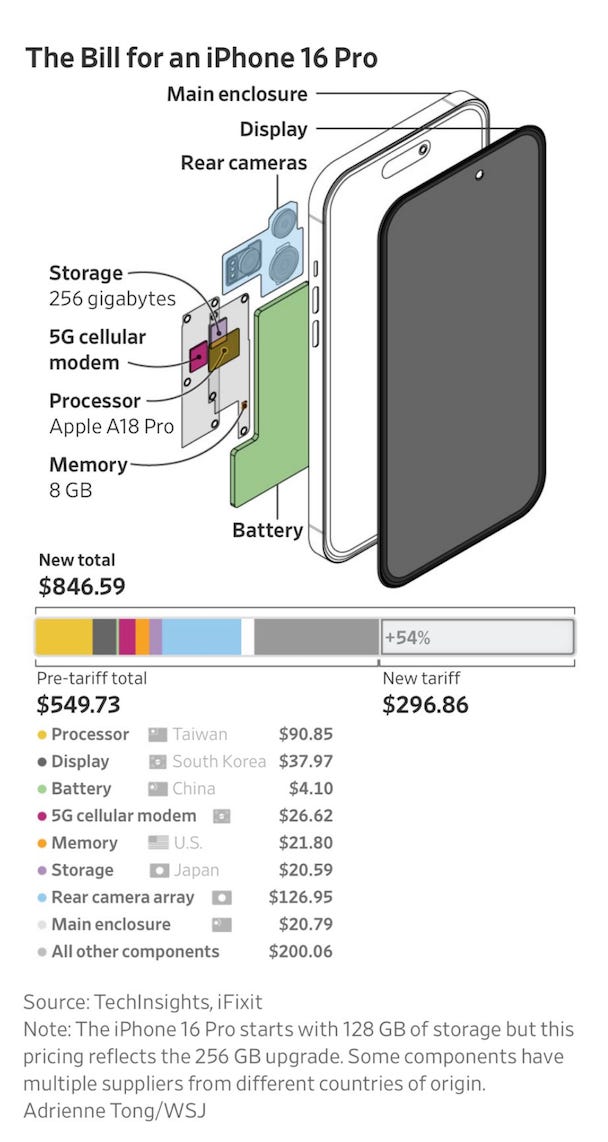

Those whose valuation reflects (or did reflect) them maintaining fat margins via outsourcing. Think Nike, Apple, and the entire US defense sector.

This was a great visual of the impact of tariffs on the cost of an iPhone.

Those whose valuation reflects their growing market share globally vs. ultra-competitive Chinese companies (think Tesla).

22% of Tesla's revenue is in China, and 10% is from the "rest of the world," where it has to compete with China's new energy vehicles without the help of tariffs. The 20% of revenue in Europe also has a question mark over it, depending on how negotiations go over the coming weeks.

Just look at analysts' average growth estimates for the company.

Those whose valuation reflects a capital-light business model. Grant William's chat with Fred Hickey highlighted the fact that AI CAPEX is depreciated over a few years, and every quarter that passes, it will be more obvious it is not providing a meaningful return.

Those whose valuation reflects overstated FCF due to stock-based compensation (works great in a bull market, not so much in a bear market).

One of the issues with SBC is that it’s a non-cash expense, so when you have companies mainly valued on EV/FCF or Free Cash Flow yield, you miss the dilution aspect of the equation. My argument would be that given FCF is the distributable free cash flow available to be distributed to investors, that the important dilution metric is how much of that FCF is being given back to employees as compensation.

I hope you’re all having a great week.

Cheers,

Ferg

Also, one last point is that passive indexing holdings reflect the optimal companies for the last decade, i.e., low inflation and abundant resources.

To illustrate this point, say you see higher structural inflation, so you buy the S&P 500 materials sector ETF as it should perform well in that scenario. This is true eventually once it rebalances to the outperformers.

Currently, it is primarily processors further up the value chain who have done well for the last decade. Only two of the top ten holdings actually mine anything…

Does your hate on ESG relate back to your Kiwi origin? Because that would make sense.

Kiwi's just don't seem to care. Moving from BC to NZ was horrifying in terms of environmental practices.

This is what ESG is cleaning up in NZ: In pastoral land 75 percent of river length has a D or E rating for swimming due to E. coli counts.

Some of the most polluted waterways in the world.

Any your pissed cause ESG is costing you a few bucks from trading account.