Ferg’s Finds

This is a short weekly email that covers things I’ve found interesting during the week.

Article

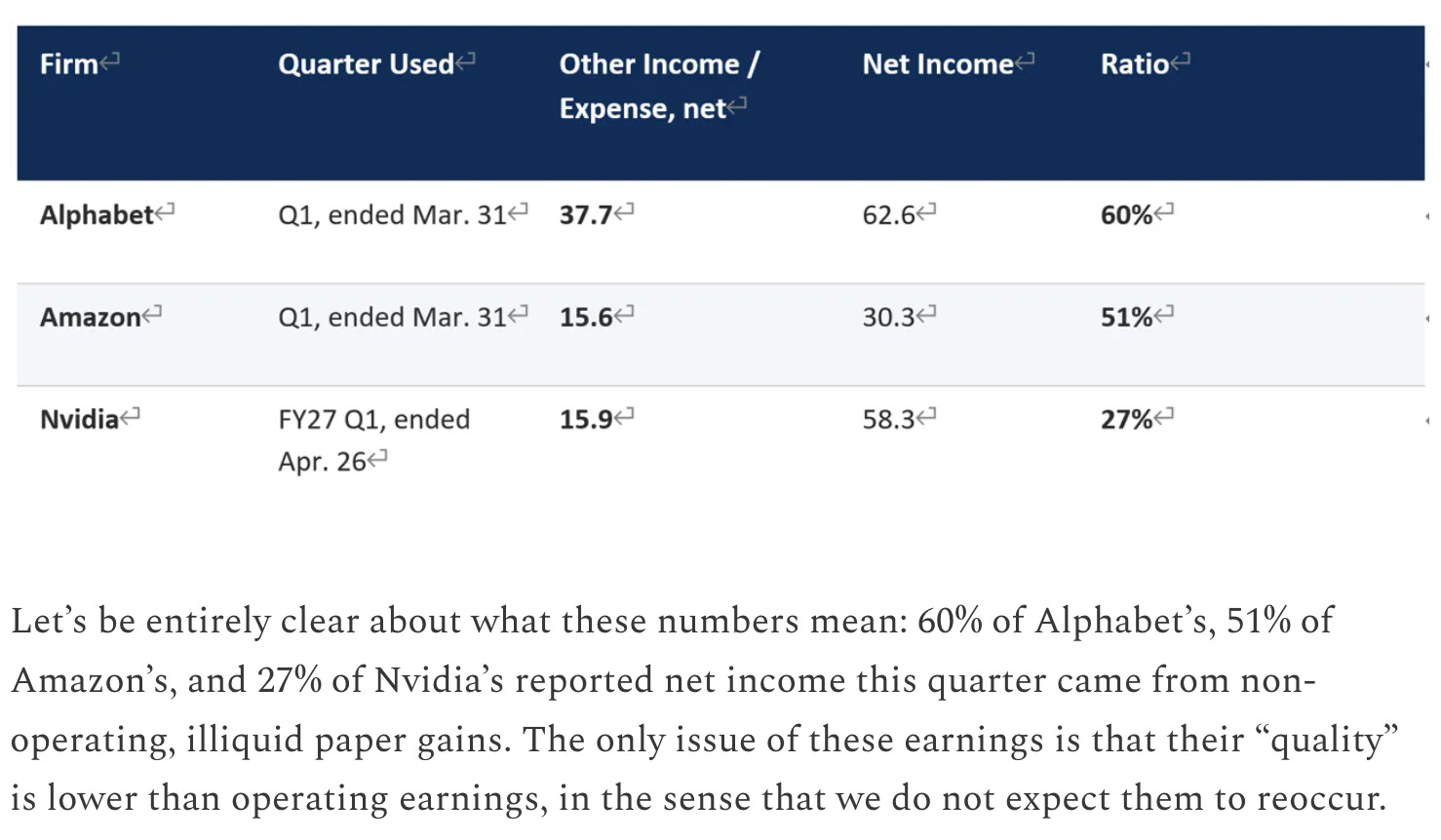

The $69 Billion Mirage: How an Accounting Rule Inflated S&P 500’s Q1 Earnings by 12%

A massive chunk of this quarter’s blockbuster “growth” didn’t come from selling more software, shipping more microchips, or delivering more packages. Instead, it came from an accounting rule that forced massive, illiquid “paper gains” onto the income statements of tech giants.

In Q1 2026 alone, just three companies—Alphabet, Amazon, and Nvidia—reported a staggering $69.2 billion in non-operating windfall under their Other Income and Expenses (OI&E) lines. When you run the macro numbers, this single accounting phenomenon artificially inflated the entire S&P 500’s quarterly earnings by about 12%.

Podcast/Video

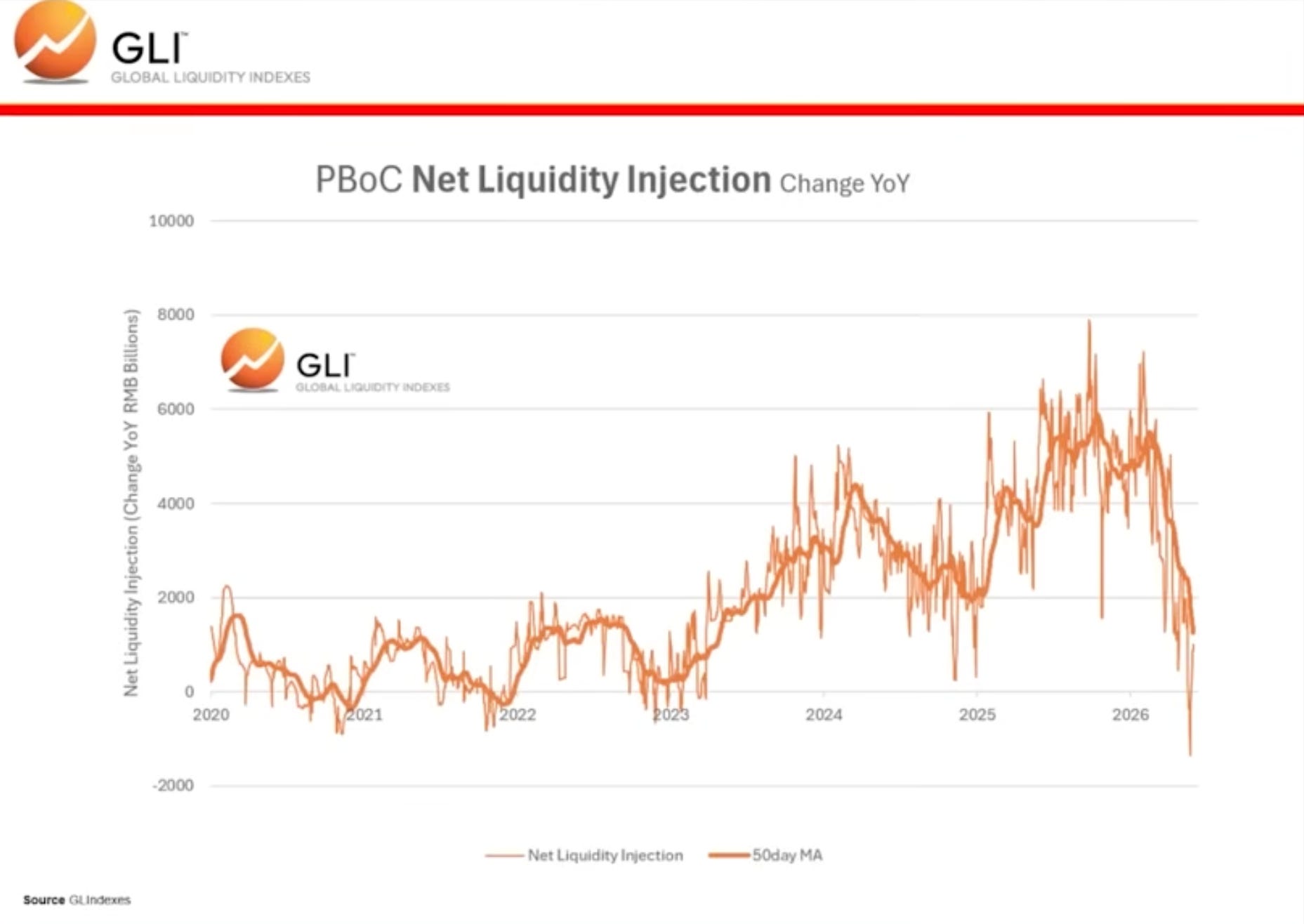

Massive Liquidity Shock Coming; Brace For ‘Wrecking Ball’ Warns Economist | Michael Howell

What happened on March 2nd was a surprise. You can see China has turned off the money tap. That is extraordinary. Why they did that is baffling, but there is probably a decent reason, and that decent reason is that it was when the Iran tensions blew up. Now, what is China doing here? In our view, they are deliberately trying to slow the economy to reduce oil demand.

-Michael Howell (Timestamp)

Quote

I find it incredibly simple: If you wait at a bus stop long enough, you’re guaranteed to catch a bus, but if you run from bus stop to bus stop, you may never catch a bus.

-Howard Marks

I thought of this quote when reading takes on Terry Smiths letter (struggling value fund pivoting to growth).

Or if you want one of the most stunning charts of sticking to a strategy through brutal volatility look at trend-follower Bill Dunn (Dunn Capitals) drawdowns!

Tweet

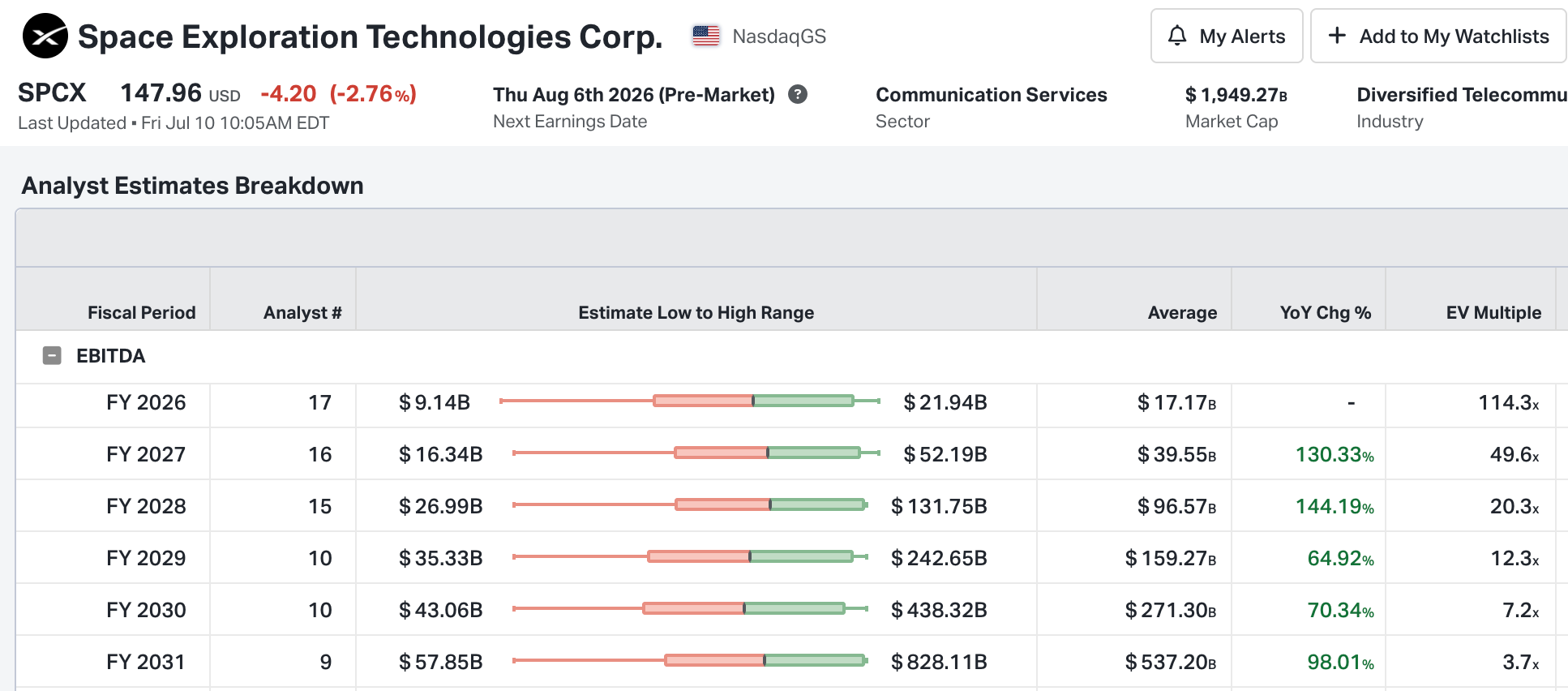

When you have AI/Tech companies valued at hundreds of billions, or even trillions, with high growth assumptions, losing entire markets to ‘sovereignty concerns’ becomes consequential very quickly.

$84 billion per year in external capital requirements…

The average analyst estimate assumes it will (nearly) double earnings every year for 5 straight years.

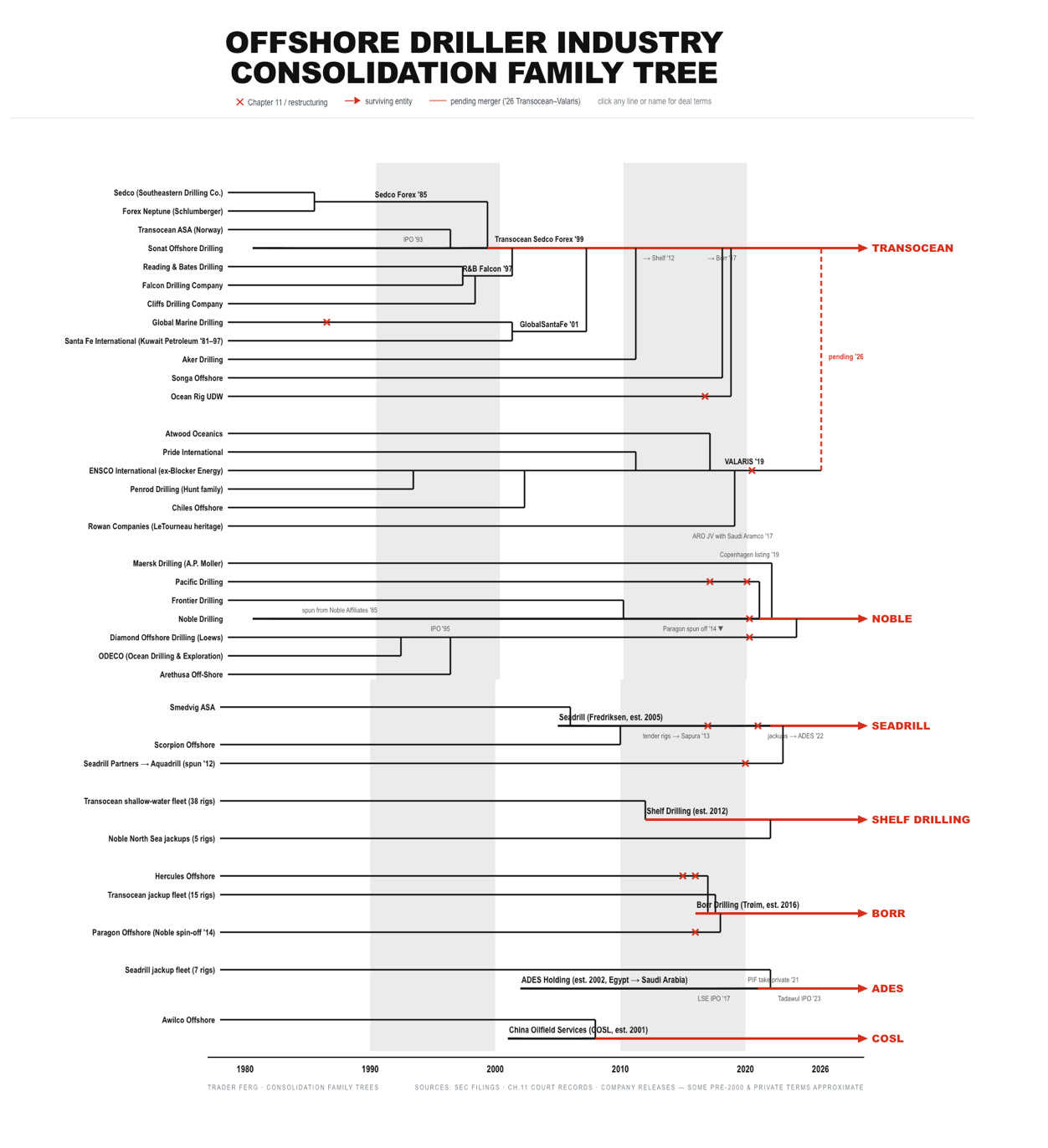

Charts

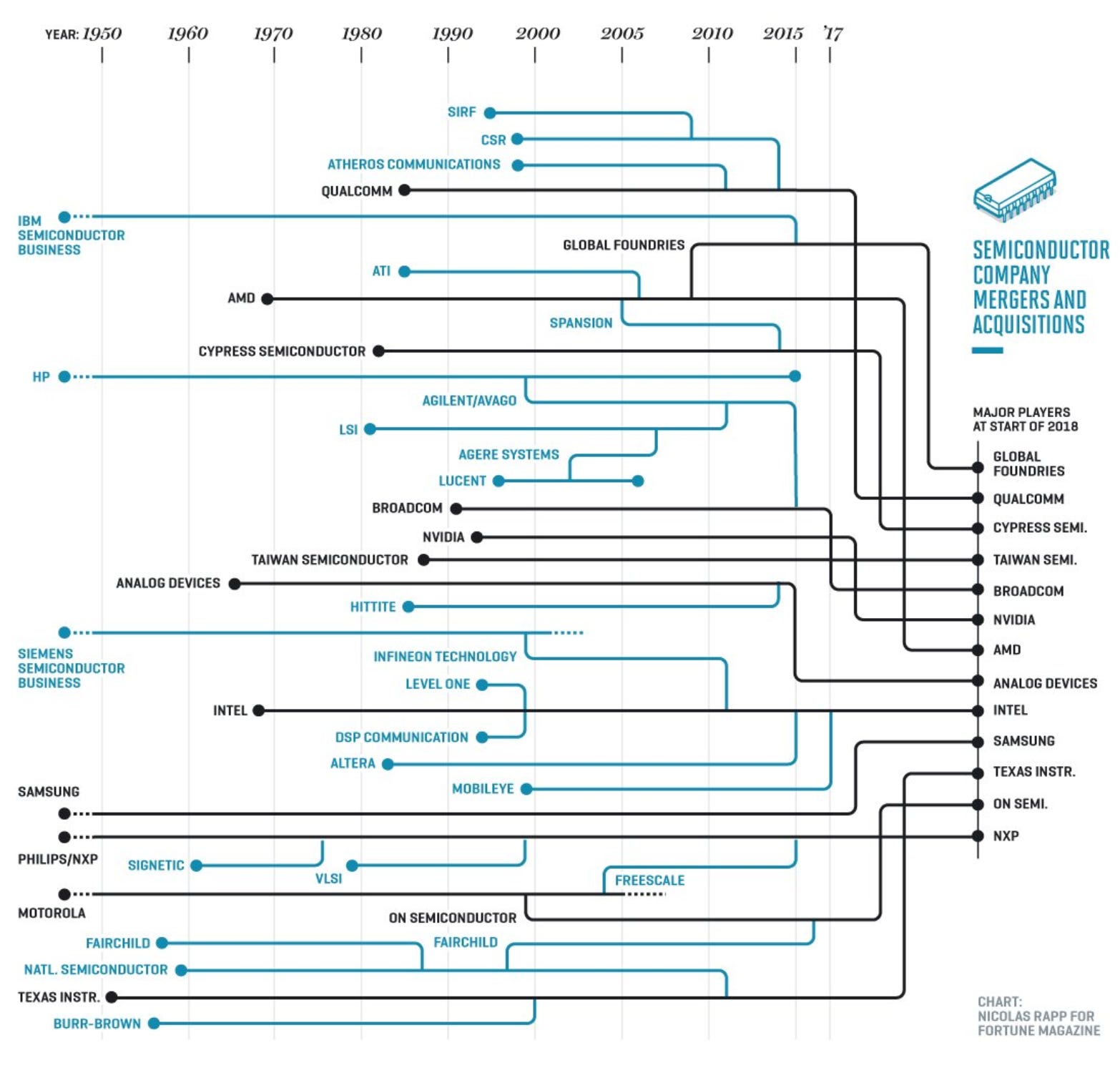

I love these historic industry consolidation charts.

My latest piece broke down four subsector consolidations within Oil services (Offshore drillers, Subsea EPCI, Tubing & Casing and Seismic Contractors).

All of which have had a similarly rough time as the offshore drillers below.

Something I’m Pondering

I’m pondering the margin of safety you can achieve via stress testing a high shareholder yield.

A company telling you they intend to buyback 40% of their float by 2030 of which you can use some really bearish assumptions and still end up around 20%, seems highly asymmetric, especially when the “average analyst” expects the companies earnings to go nowhere.

Shells is my favourite example of this currently which I’ve gone over here and doubled down here.

Hope you are all having a great week!

Cheers,

Ferg

P.S. As a tourist in many commodities, I’m always looking to bring on the veterans, especially when I’m questioning my read on the sector. Matt Warder and Joe Aldina are those two veterans who have forgotten more than I’ll ever know about coal. So it was good fun bringing them both on to discuss how they view the setup for thermal and met coal here.

For this week’s “Where in Montenegro am I?”, it’s a little village in Kotor Bay chasing these two around.

” …losing entire markets to ‘sovereignty concerns’ becomes consequential very quickly.”

That is what happen when those entire markets start thinking about the ”resilience premium”.

Hi Ferg ,excellent again ,have you done any work on why the crack spreads are blowing out ,if you have, ignore this ,ive missed it some were, my take after listening to everyone ,and im probable wrong , is the worlds oil sysmtem has gone from a set pathway ,well oiled machine,low margins on routes,ships,turn around time,low margin ,tankers ,to chaos with oil flowing from spr,so ships contracted at the margin , because ,its not routine they have to add in excess charges to cover things they didnt antipate ,therefore cost of shipping blows out due to added unknows, so this shipping gets added to each barrel , hense cost of barrel blows out delivered to refinery , hense crack spreads blow out. No one ive seen has gone into any detail on this issue so im guessing .my take is its never going to end , this oil fertiliser ,sulphur goes off line , new projects come forward to replace GCC supply (takes time),eventually Trumph will TACO,or itll work it self out , new prjects will over supply ,and the cycle goes around again ?? thats if we dont have a world collapse from the crack spreads blowing out,but its a interesting time in oil as i love it,listening to everyone and when we come out the other side,see who got it right and see who got it wrong ....lol...i cannot see how the penny wont drop soon that the only way we replace this oil is with the drillers ...im holding cheers