The Resilience Pivot

Biggest beneficiaries of a pivot from Net-Zero to Strategic Resilience

The usual disclaimer: my record of forecasting geopolitical events is unblemished with success (similar to my short-term trading abilities…)

I do my best to combat these shortcomings by positioning where the investment outlook is largely baked in at this point.

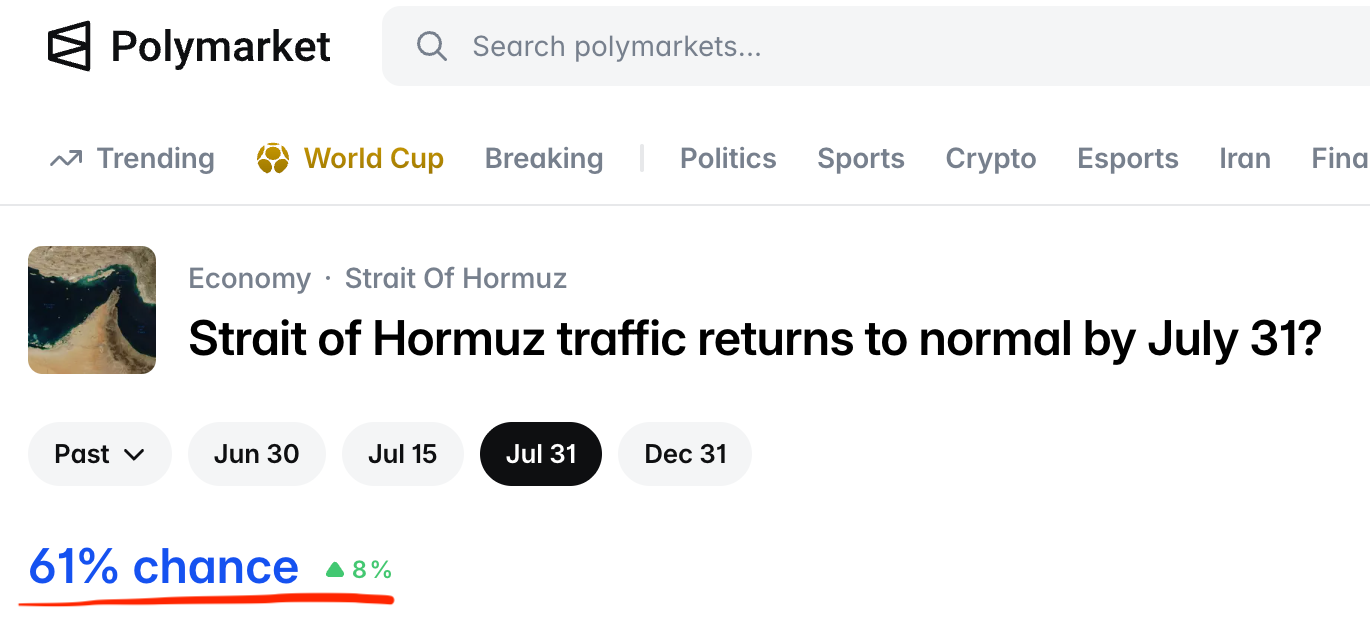

Polymarket has odds of 61% that Hormuz Traffic will be back to normal by 31st July*

You’ve got to give it to Trump for managing market expectations;

“It” has worked every time…

While those of us (like me) who dabble outside AI/Semi’s have been left channelling our best Ron Burgundy.

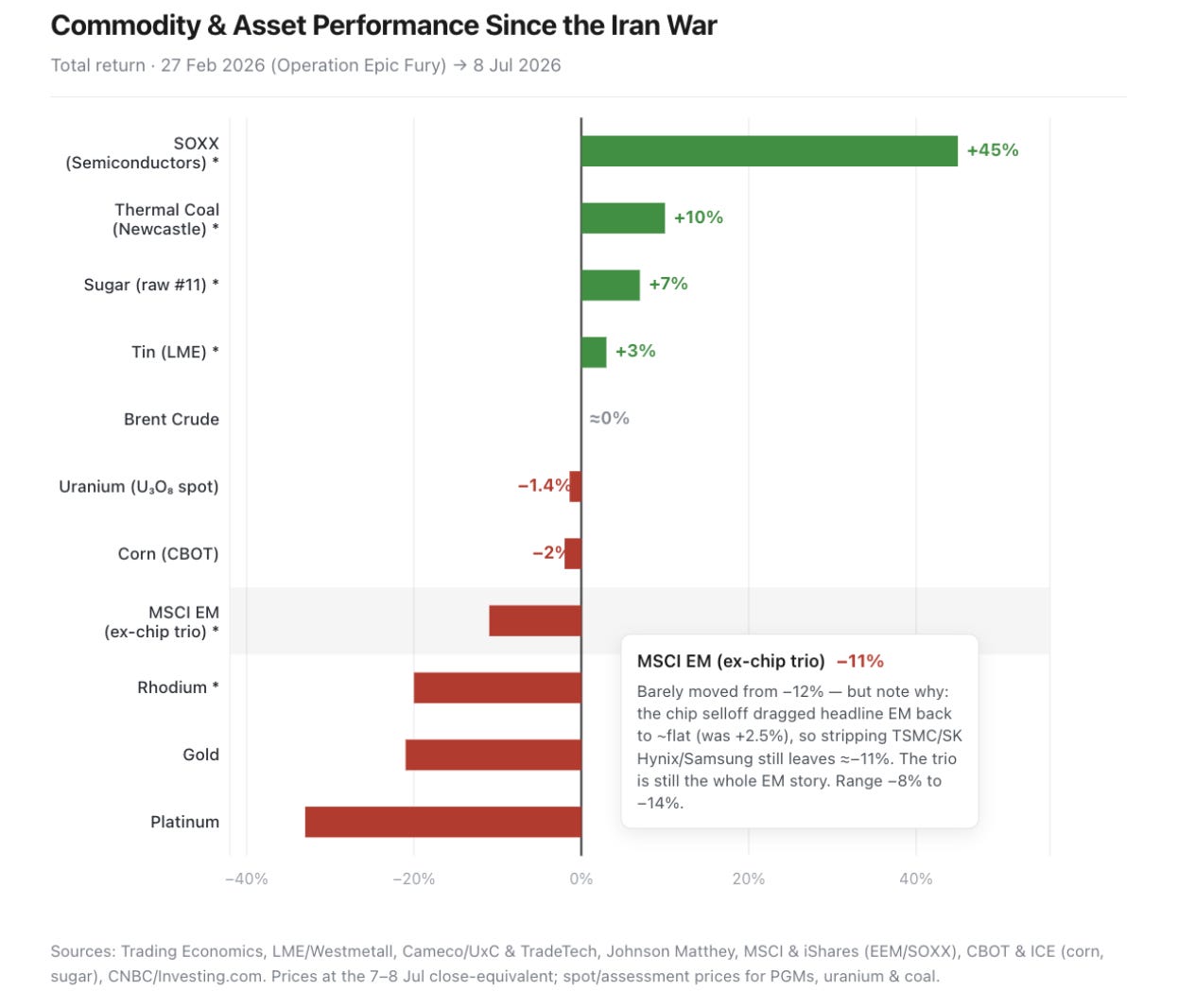

Adding to the embarrassment is that I’m heavily long emerging markets, yet since I don’t own TSMC, SK Hynix and Samsung, so I’m also in the hole on my EM holdings (while coal was my favourite play heading into this war, I’ve got nothing to show for the below outperformance.

Playing a Messy Reopening

My take (remembering the disclaimer) is that the worst is behind us, mainly because there are too many constraints on Trump to allow a full-blown re-escalation.

SPR drawdown approaching critical levels

US Munitions drawdown: Last Rounds? Status of Key Munitions at the Iran War Ceasefire

US Munitions replenishment: China sanctions 10 U.S. defense companies in tit-for-tat response to Pentagon’s Chinese military list (June 22nd 2026)

US Midterms approaching

Not that my view matters at all…

One of the first lessons my mentor Brad taught me.

“It’s the expression of the view that matters, not the view itself.”

The best expressions today are those that work with the current outlook while giving you optionality as things get even messier. Shell, being a recent example, in it does just fine with LNG and Brent prices here, while any further uplift is gravy (as I edit this, a Qatari LNG carrier just took a direct drone hit…)

Engineering, procurement, construction and installation (EPCI) companies operate under a similar setup; there is no undoing the effects of a second energy crisis in four years, and countries are now set on improving energy resilience. Plus, if more stuff gets blown up in the Middle East, it just gets added to their backlogs…

No going back…

We are not going back to a world where countries are comfortable with a large percentage of their oil, LNG, or fertiliser being ‘just-in-time’ transits through the Hormuz Strait.

Resiliency Trend

This trend will see policymakers looking to boost resilience via:

Stockpiling: Why the Next Billion Barrels of Oil Demand Could Come From Storage.

De-risk/diversify/boost domestic oil & gas/LNG

Coal (Asia’s quick fix).

Nuclear (world’s long-term fix)

Renewables (medium/long term fix, especially solar, for Asia & Middle East)

Battery storage (buffer renewables’ intermittency)

EV/Hybrids (Boost domestic resiliency if a net oil importer).

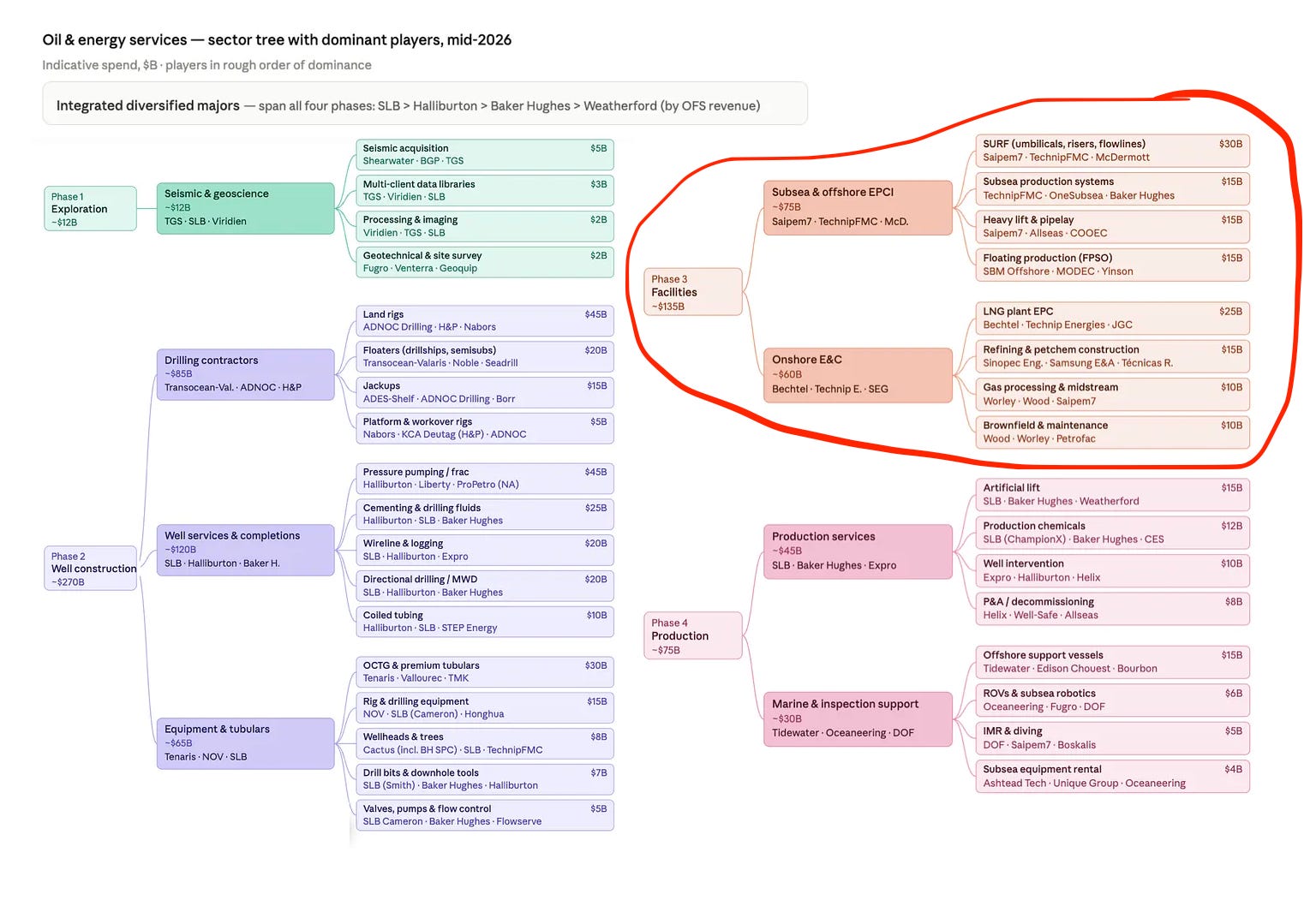

De-risk/diversify/boost domestic oil & gas will heavily benefit oil services as a whole, with EPCI arguably one of the best-positioned.

Engineering, Procurement, Construction and Installation

EPCI is one of the deepest pockets of value in oil services following heavy consolidation; the surviving companies have cornered their respective niches and built substantial backlogs, which will continue to grow with the resiliency tailwind.

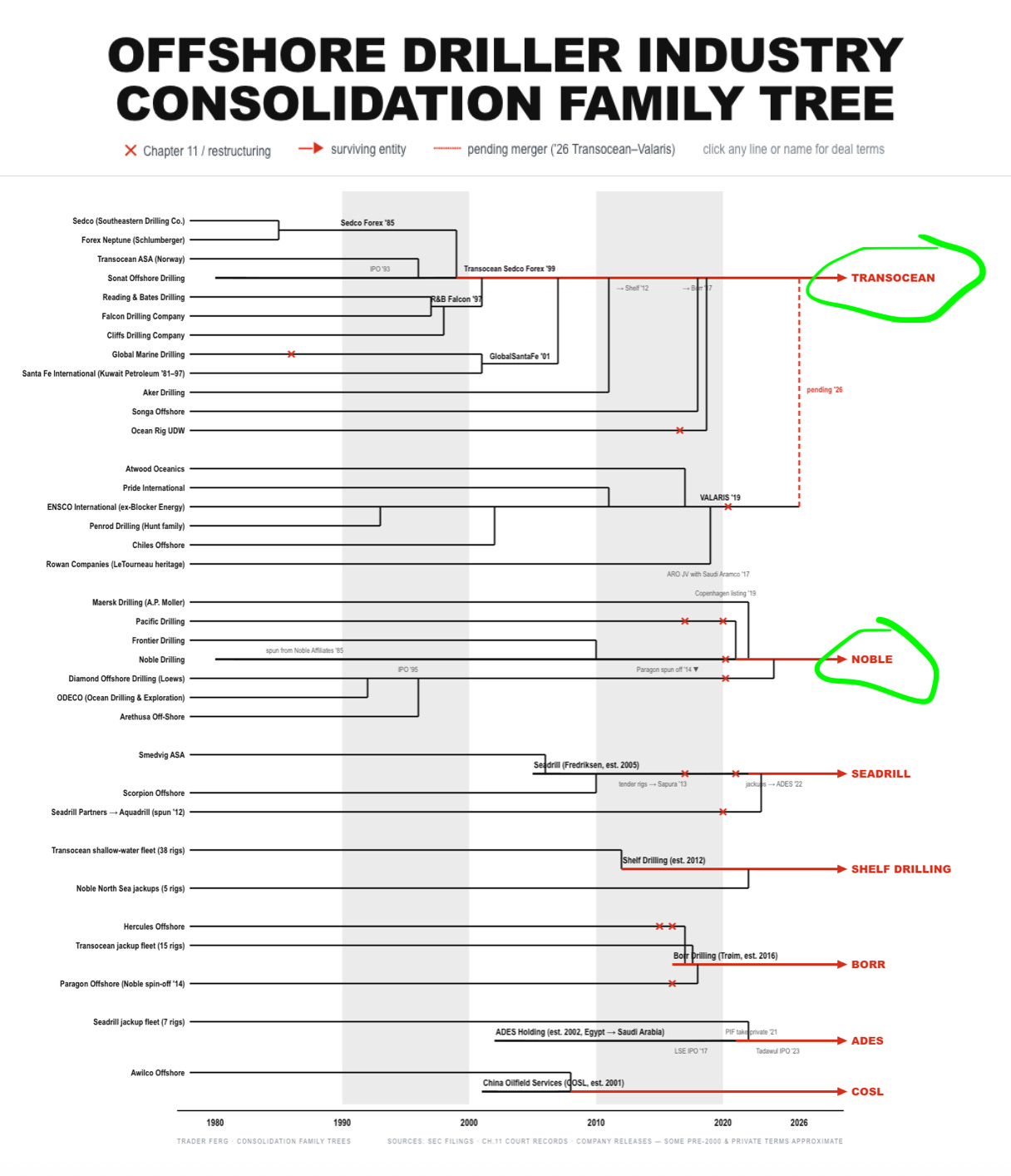

Extreme Consolidation

The oil services sub-sector I’ve spilled the most digital ink on is offshore drillers, where I continue to like the outlook (Driller utilisation is on target to hit 90% in 2027).

This can be summarised as a brutal game of survival of the fittest…

EPCI Consolidation

Subsea EPCI has arguably had it just as tough as offshore drillers, with a third of the companies still in restructuring/private hands. Vantris is hanging on for dear life, and Saipem effectively went bust in 2022 via a massive recapitalisation (of which I had the pleasure of partaking).