Ferg’s Finds

This is a short weekly email that covers things I’ve found interesting during the week.

Article

Building energy resilience is set to take the baton from Net Zero.

Why the Next Billion Barrels of Oil Demand Could Come From Storage

Many countries, especially in the Asia Pacific, are looking to build new reserve capacity to boost their energy security and never again be caught off-guard by a massive supply disruption like the one triggered by the closure of the most important oil and LNG chokepoint.

From India to Australia, energy importers are looking to expand capacity to hold crude and fuel reserves to be better prepared for the next energy crisis, which, in this fragmented geopolitical situation, is a matter of when, rather than if.

India needs to move from ad hoc crisis response to strategic oil stockpiling: analysts.

India needs to urgently fortify its energy security by transitioning from an ad hoc crisis response to a strategy of sovereign crude oil stockpiling, thereby guarding against future disruptions in global oil supply chains, think tanks and advisory agencies said.

While the country has initiated efforts toward building Strategic Petroleum Reserves, the existing storage capacities are quite insufficient and must be augmented to serve as a true macroeconomic shield, they added.

Podcast/Video

I got a lot out of this discussion between Louis-Vincent Gave and Anatole Kaletsky: The Ceasefire And Mad Markets.

Quote

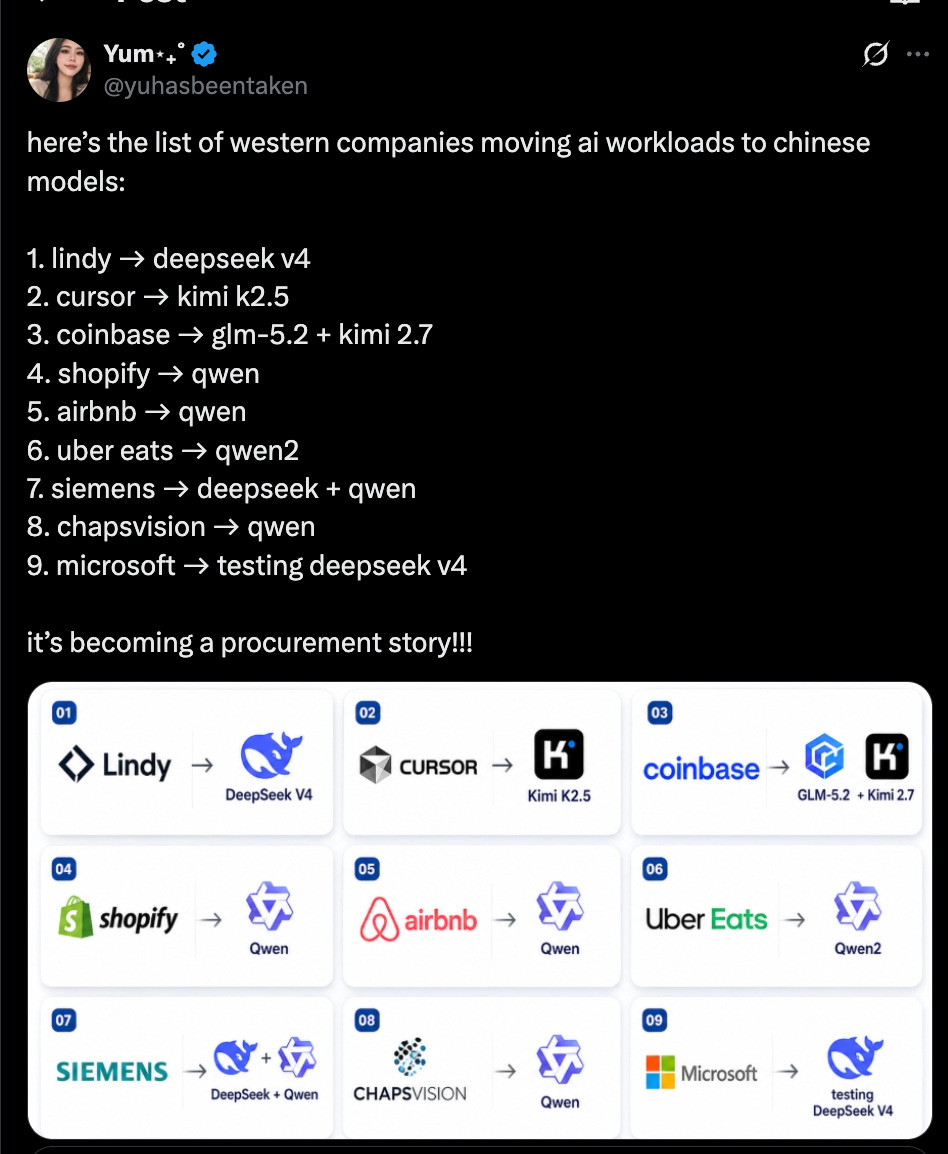

China’s AI playbook: kill OpenAI and Anthropic with great free models. Make it free. Then use cheap electricity to export compute as well. Currently, the blocker is the chip, but Huawei will catch up soon. Imagine a world where instead of paying hundreds of billions to OpenAI and Anthropic, you pay almost zero to similar level of intelligence with cheap, cheap inference. What’s gonna happen?

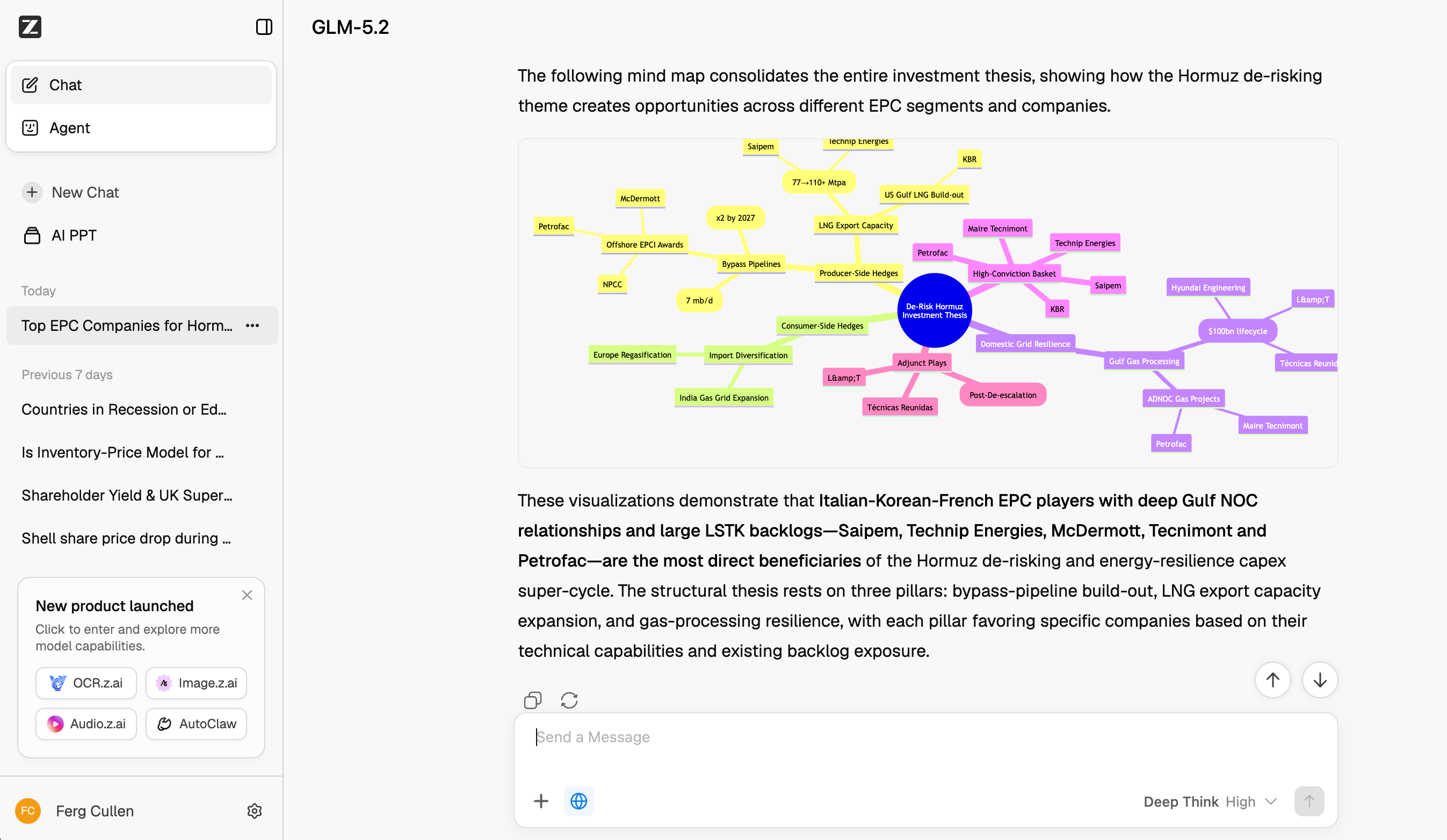

Rather than opine about Chinese LLM’s I downloaded GLM-5.2 and dropped the same queries in Claudes Opus 4.8.

Opus 4.8 clearly still has the edge I’d say GLM-5.2 is a close second.

The question is how much you’re willing to pay for that edge? 5x more for Opus, 12x more for Fable 5? The below companies have already made their decision.

Tweet

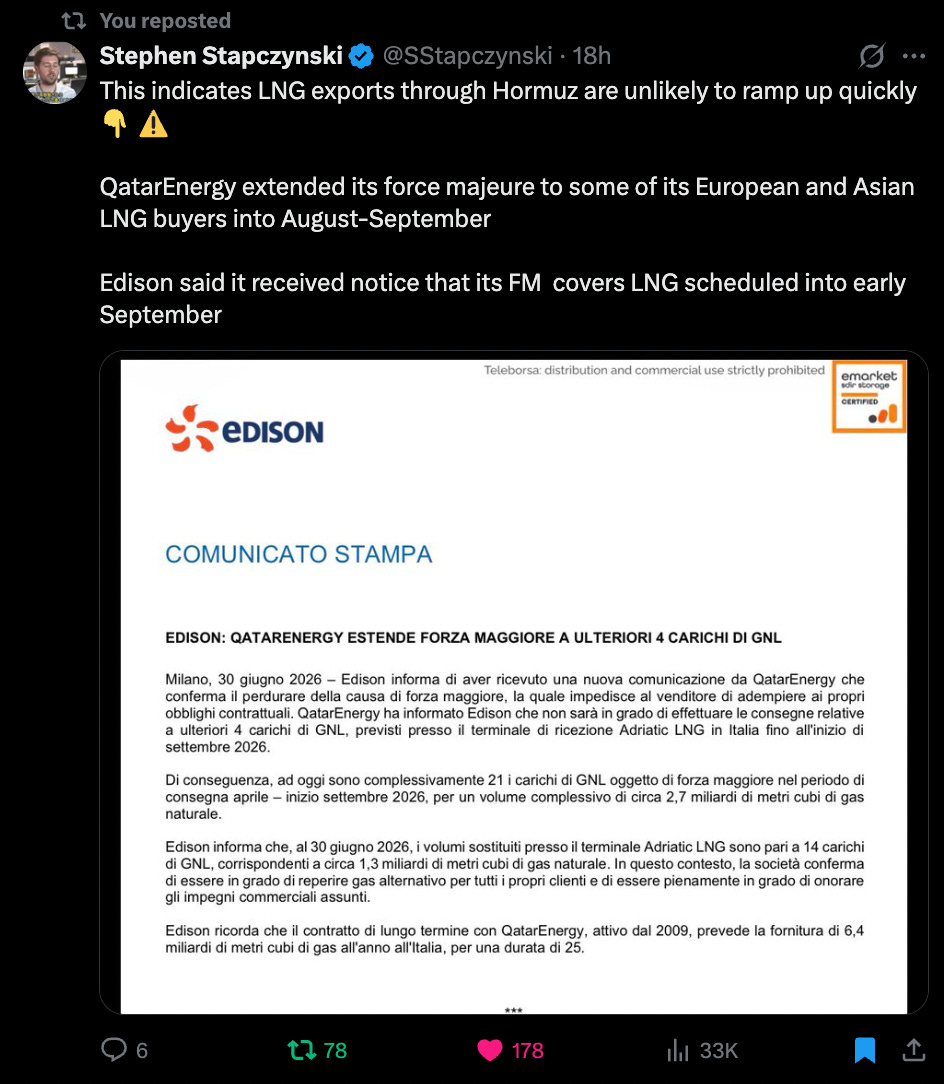

Stephen Stapczynski is a great follow for LNG/energy news.

This QatarEnergy notice was interesting as it suggests they’re set to miss the entire Asian cooling period, against early reports that Ras Laffan could be at full capacity by mid-August.

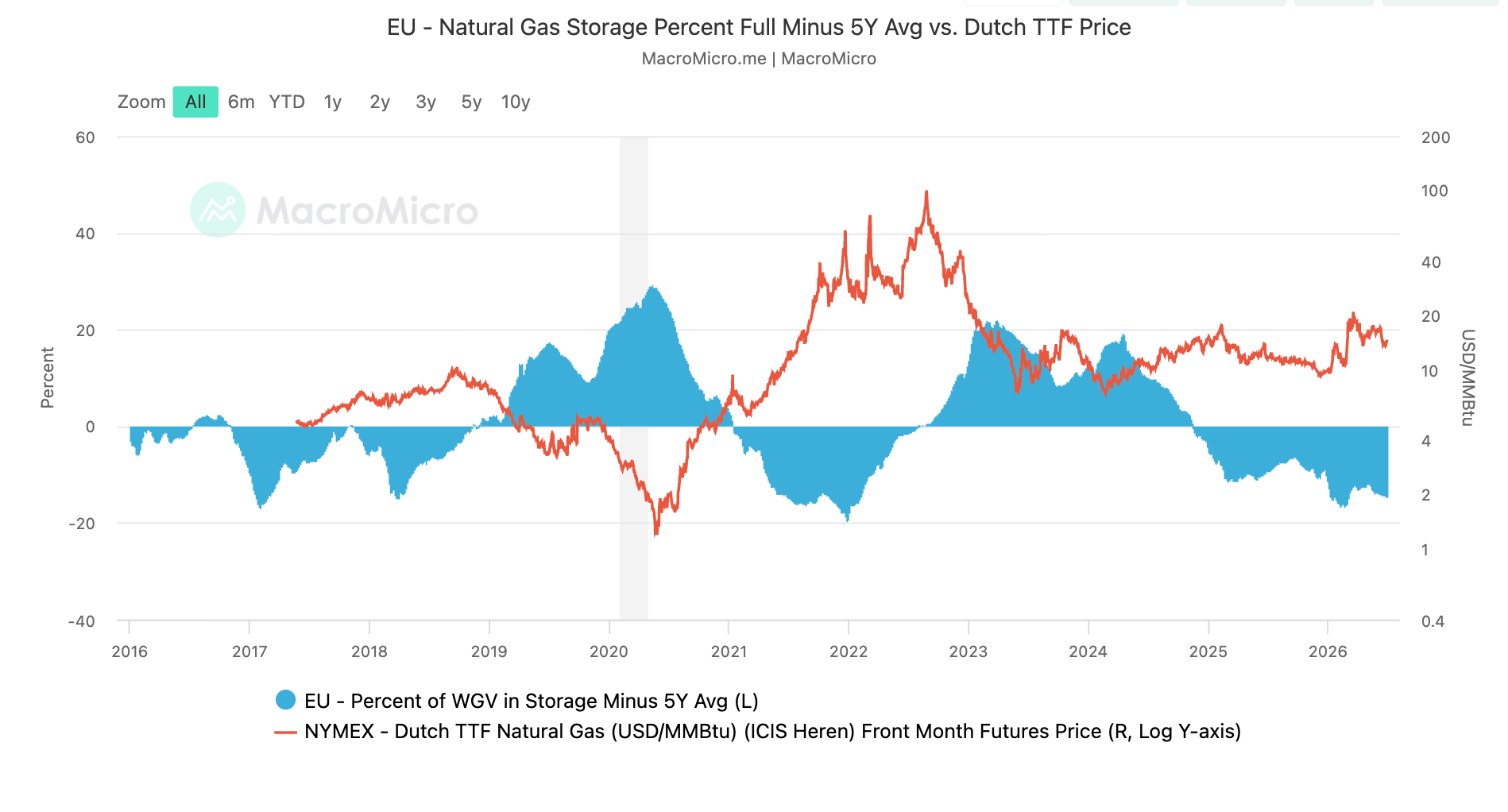

Charts

This chart illustrates that the EU storage issue has been cumulative, following two winters of insufficient storage refills. Europe is at its lowest gas storage in 15 years

Something I’m Pondering

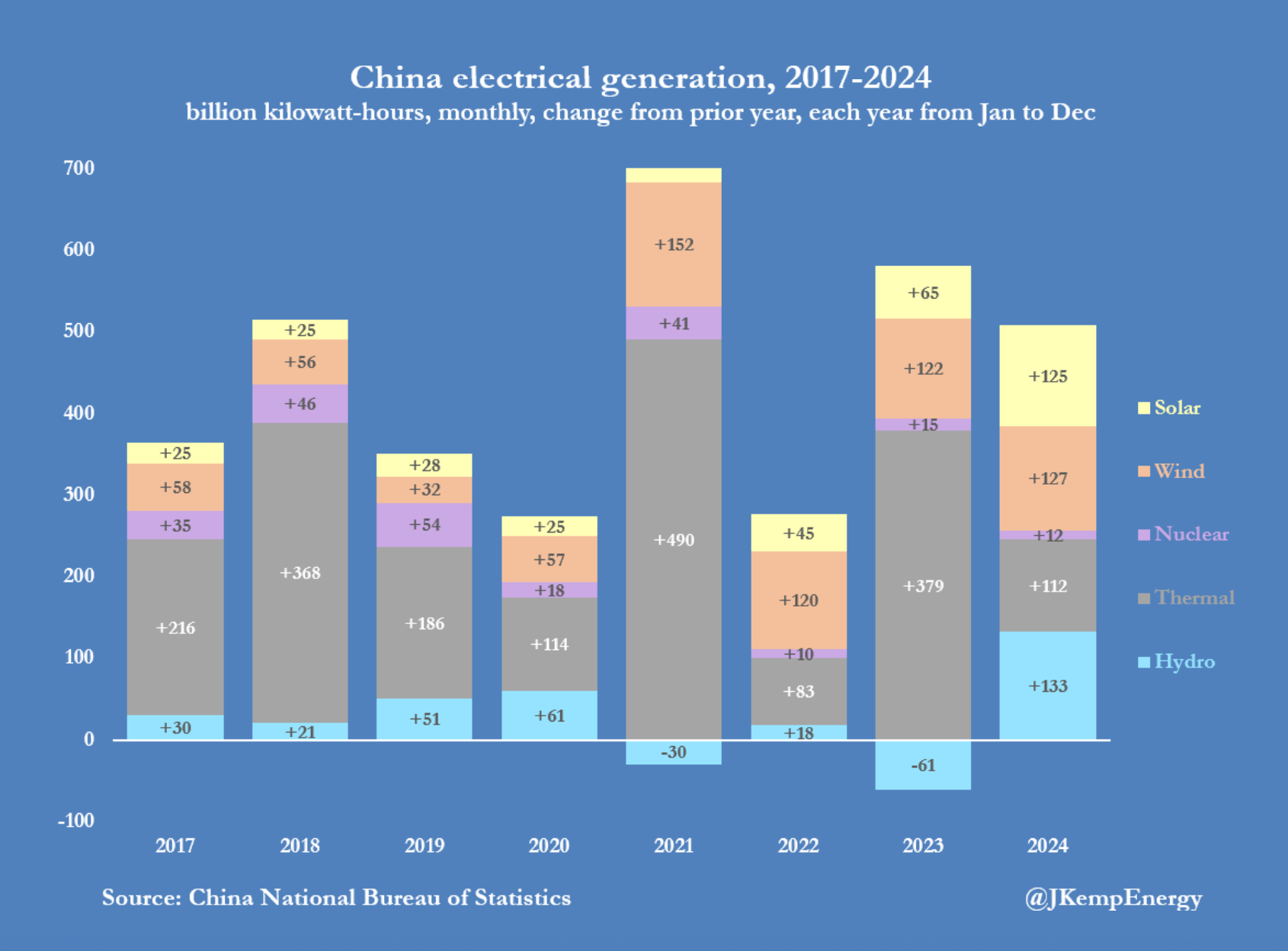

I’m pondering where China’s energy demand will land this year (we will only know with hindsight).

A lesson from the last few years has been to be careful about drawing conclusions from China’s low-growth years, when coal utilisation as a percentage of generation dropped only to roar back the following year (2021 and 2023). That said, current Chinese consumption data isn’t very encouraging.

As mentioned in last week’s Ferg’s Finds (China Has a Powerful New Oil Price Weapon), Chinese oil demand has proven to be surprisingly flexible.

If 2023 is anything to go by (similar to coal), the rebound can be substantial.

Hope you are all having a great week!

Cheers,

Ferg

P.S. Today I was lucky to have Martin Tavella of Somar Capital walk me through his thesis on the almond market and how he’s playing it. It’s a fascinating little sector in which I couldn’t help but draw parallels to other cyclical sectors I’ve dug into. An almond tree takes five years to reach full maturity, leading to periods of oversupply and underinvestment, creating supply constraints, where we find ourselves today.

We are in Ada Bojana, Montenegro (on the border with Albania) for the week, enjoying the beach and seafood restaurants along the estuary.

It’s almost like the world is figuring out that storing hydrocarbons is the most economical battery system 🤔

What kind of computer do you have that can run GLM locally?