Fergs Finds

This is a short weekly email that covers a few things I’ve found interesting during the week.

Article

While I referenced this brilliant piece: The Return of Matter: Western Democracies’ Material Impairment in my latest post, I skipped over what I believe is the ultimate scarce asset in skilled labour (in the West that is).

The Human Bottleneck

Real smelters, SX lines, calcining trains, and high‑temperature chemical plants are run by people with tacit knowledge that does not live in textbooks:

Metallurgists who know how to nurse an unstable furnace back into spec without cracking a refractory lining.

Process engineers who have personally tuned a 200‑stage SX train rather than just modelling one.

Maintenance crews who have spent a decade keeping acid plants, off‑gas systems, and high‑vacuum equipment alive in dirty conditions.

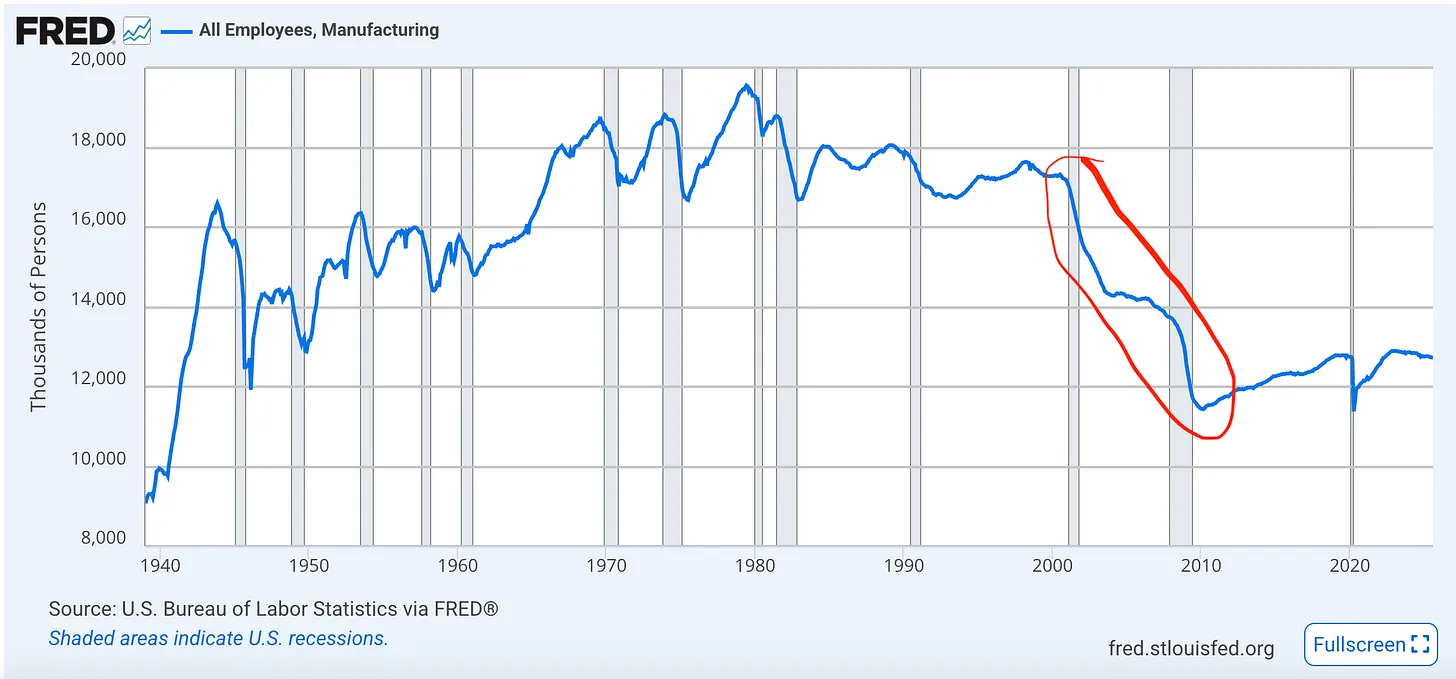

Those people are thin on the ground in the US and EU because we paid them to retire or move to other industries. Their apprentices were never hired. Universities still teach metallurgy and chemical engineering, but graduates are pointed at batteries, software‑wrapped “process analytics,” or ESG consulting instead of refineries and smelters. When we talk about “rebuilding the midstream,” we are implicitly assuming a labour force that does not yet exist.

It took a decade for the US to lose six million manufacturing workers, and it will take as long, if not longer, to attract them back, IF the incentives are right (pay a high real wage), before touching on robots, etc.

Yes, historically, the US doubled manufacturing jobs when on a war footing between 1940 and 1945 through the conversion of civilian industries to military production, government incentives, low-interest loans, accelerated depreciation allowances, and access to government-financed facilities.

A crucial factor that enabled this was that the unemployment rate stood at 17.2% in 1939 (the back end of the Great Depression), with approximately 9.5 million Americans still out of work (by 1943, unemployment reached a mere 1.2%). The war economy essentially absorbed the entire Depression-era unemployment pool into manufacturing and related industries. Not exactly the set-up we have today, with 4.6% unemployment, before questioning how many of those are actually fit (obesity, drugs, etc) to work in manufacturing.

Podcast/Video

Luke Gromen: Some thoughts on BTC and silver

Unless the Fed and/or Treasury pre-emptively begin post-COVID-sized liquidity injections, financial conditions in the global economy will likely continue to tighten until a crisis forces said “nuclear printing.”

Quote

Capitalism works not just by allowing upward mobility, but by accelerating its downward equivalent.

-Nassim Taleb

Tweet

The question for me is straight to nuclear printing, or crisis, then nuclear printing?

Charts

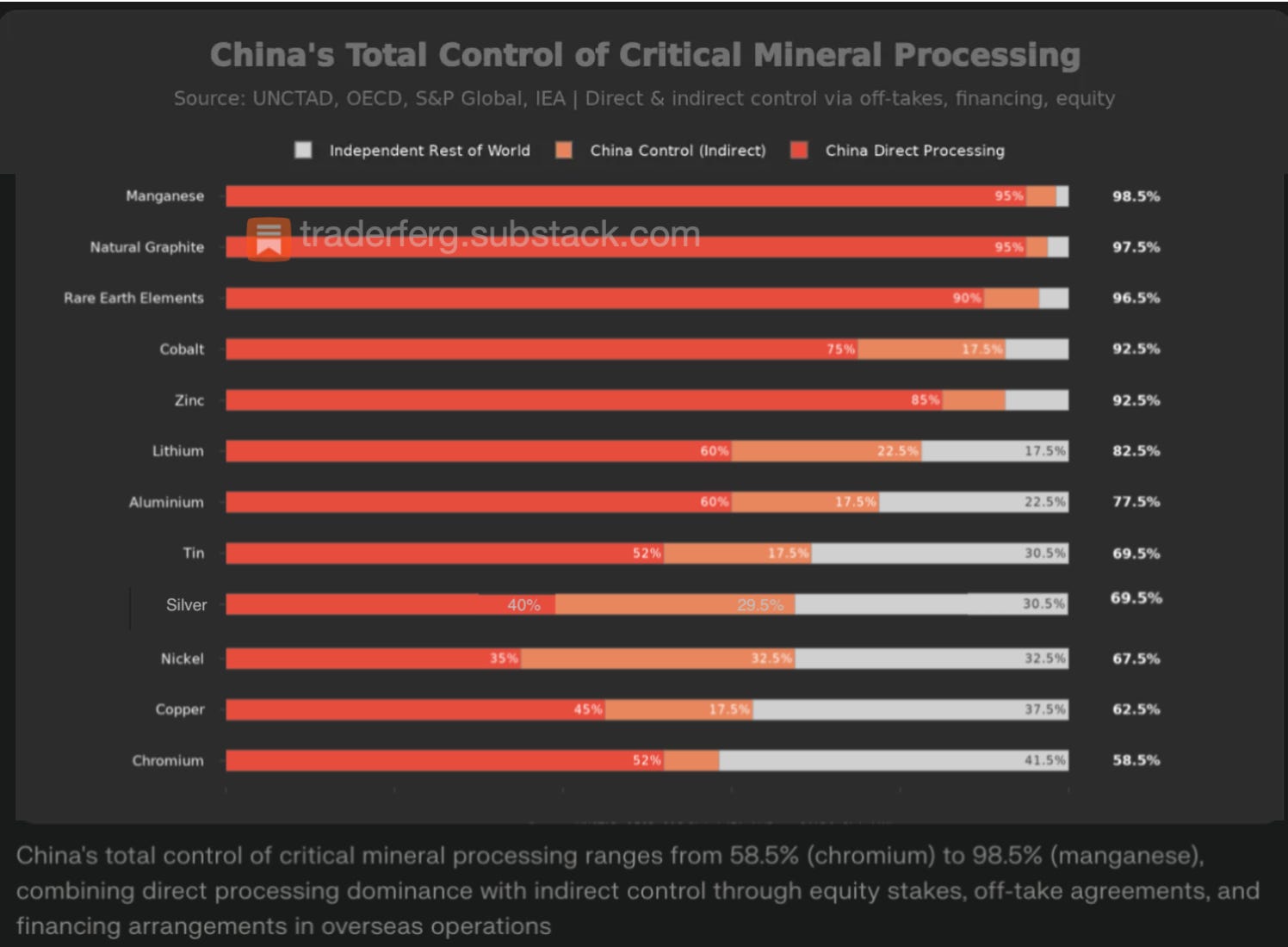

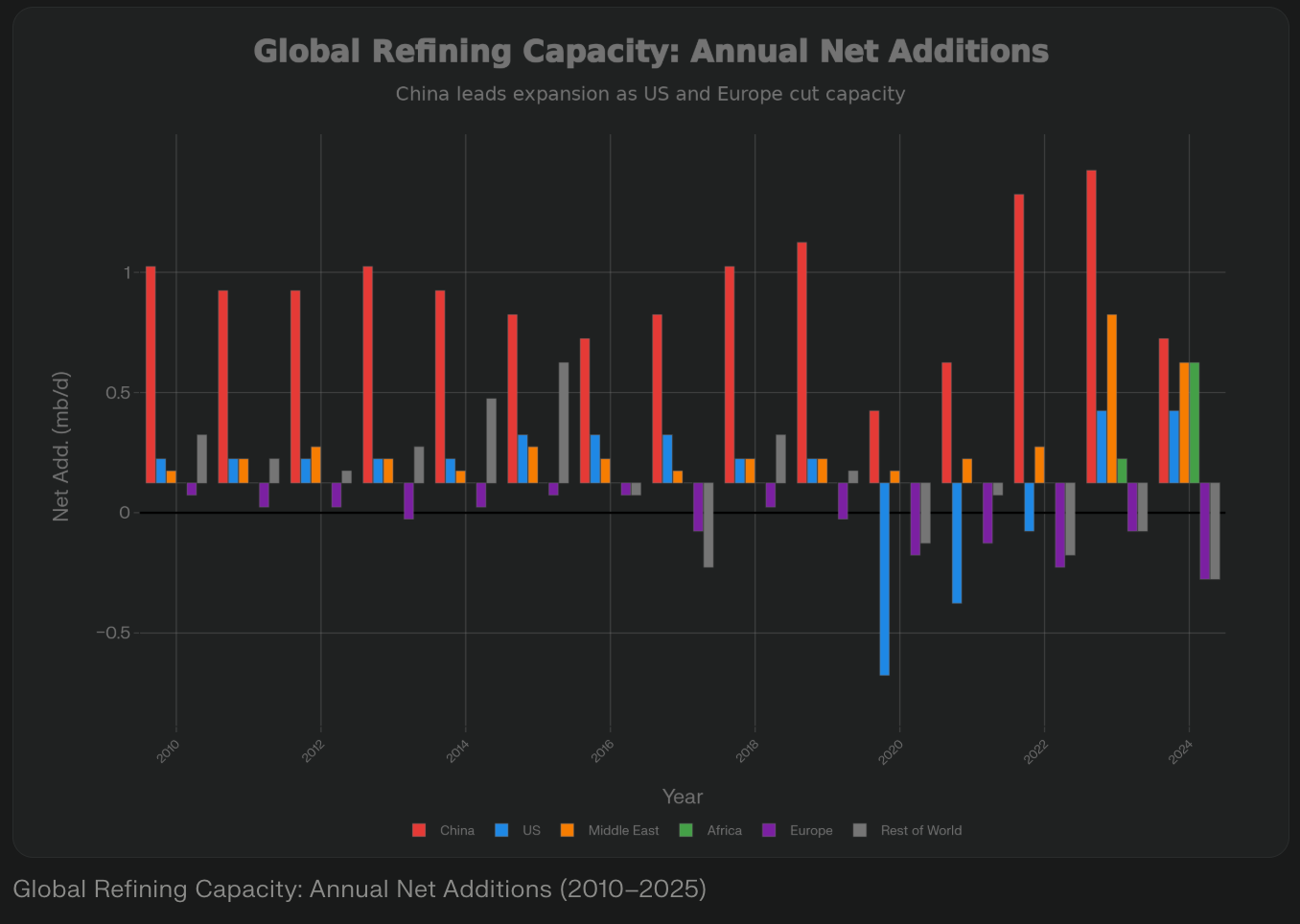

As I was working on my latest piece and creating the chart below, it struck me that there is very little commentary on Chinese control in another form of processing in refining.

While on the surface, China’s 18.5% of global refining doesn’t seem a cause for concern. Once you start to piece together their control via financing, the amount of oil they have “encumbered” via long-term contracts, equity investments, loans-for-oil deals, and active stockpiling paints a different picture (especially when considering the US inability to refine its own light sweet, as 70% of US refining capacity is optimised for heavy, sour crude).

Something I’m Pondering

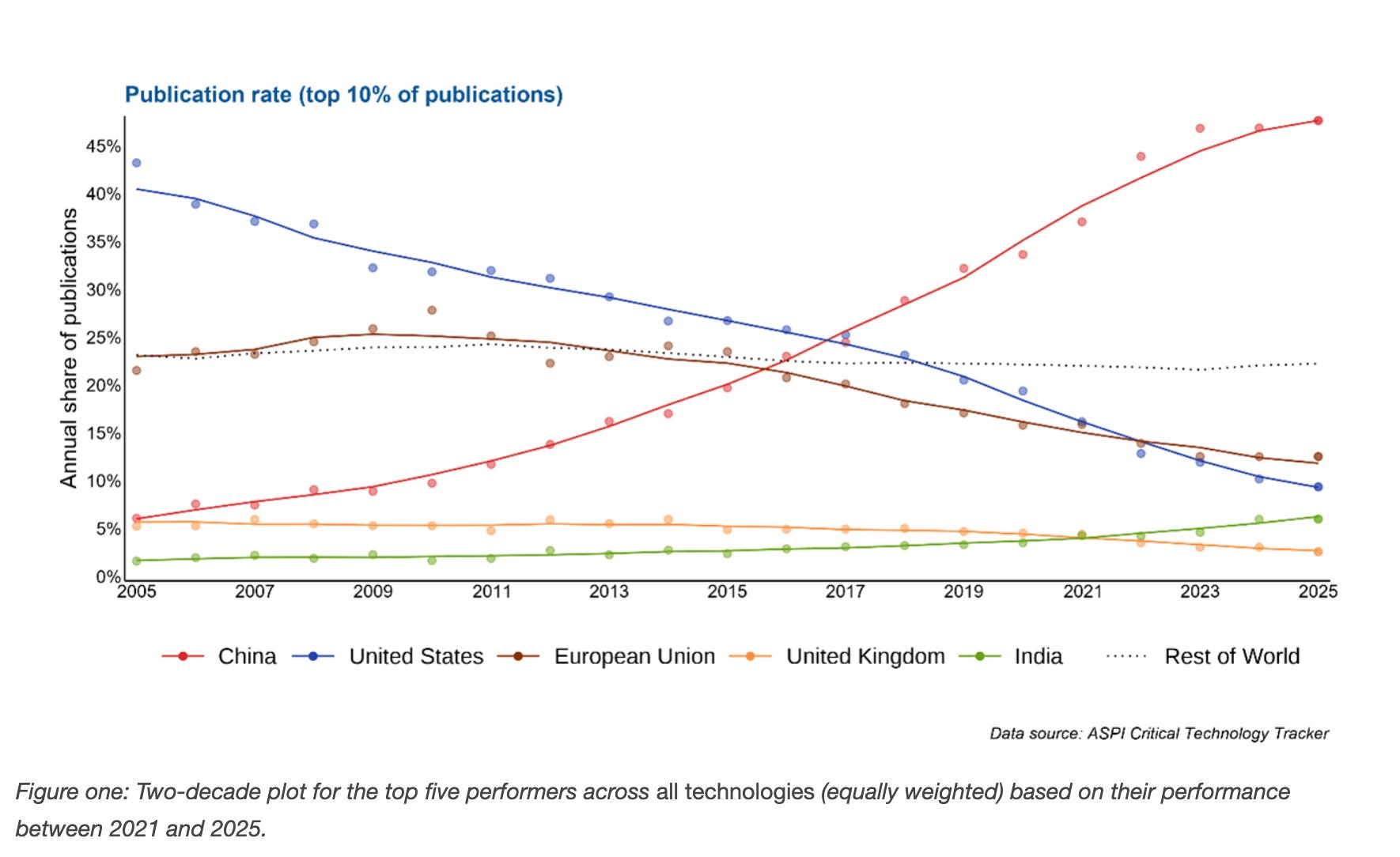

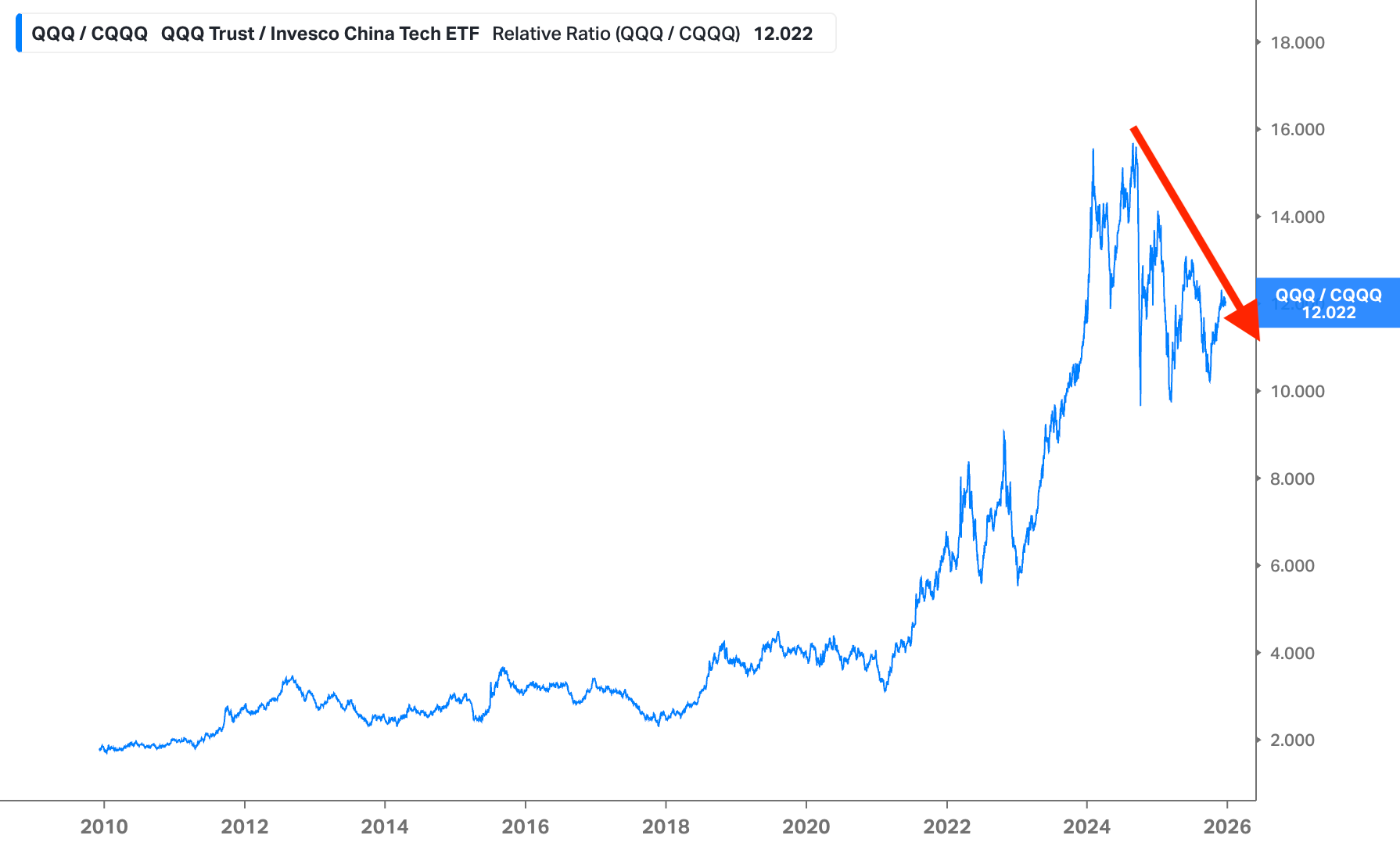

I’m pondering how tech leadership has quietly passed from US to China.

ASPI’s Critical Technology Tracker: 2025 updates and 10 new technologies

In eight of the 10 newly added technologies, China has a clear lead in its global share of high-impact research output. Four—cloud and edge computing, computer vision, generative AI and grid integration technologies—carry a high technology monopoly risk (TMR) rating, reflecting substantial concentration of expertise within Chinese institutions.

The historical data for these new technologies tells a familiar story: an early and often overwhelming US lead in research output in the opening decade of this millennium, eroded and then outmatched by persistent long-term Chinese investment in fundamental research. In total, China now leads in 66 of the 74 technologies tracked, with the United States leading in the remaining eight—an imbalance that underscores why trusted partners need to act together to leverage comparative advantages, reduce concentration risk and shape the trajectory of critical technologies together.

The ratio of US tech to Chinese tech suggests the market is rapidly repricing this reality, as I’m trying to capture in (Hated Tech, Hated Tech 2.0 and The Coming Asian Boom).

I hope you all had a great Christmas and wish you all a happy New Year!

We managed a little getaway with friends.

Cheers,

Ferg

P.S. While I did my best to explain whats happening this Youtube breakdown on silver is fantastic: PANIC MODE: Shanghai Hits $78.49 — $10 Arbitrage Gap Next (h/t Chris M) and most recently SILVER HITS RECORD $85 IN SHANGHAI — Comex Losing Control

The human bottleneck is real, no shortage of accountants, lawyers, economists, consultants, advisers, business managers, bankers and so on... When it comes to actually getting something done that doesn't involve pixels on a screen, talking or writing, ie real matter in the physical world then tough luck.

Happy Christmas Ferg and family. That'd be you in the Santa outfit, no?