Ferg's Finds

This is a short weekly email that covers a few things I’ve found interesting during the week.

Article

Last week I linked JPMorgans latest Energy paper; this archive is also worth working through:

Podcast/Video

I love a dose of Kuppy calling it as he sees it: Oil To Triple Digits As Crisis Unfolds, Economic Boom Continues | Harris Kupperman

Quote

"Every past market crash looks like an opportunity, but every future market crash looks like a risk"

-Morgan Housel

Tweet

When you Google Hypocrisy, this tweet should pop up as the first example.

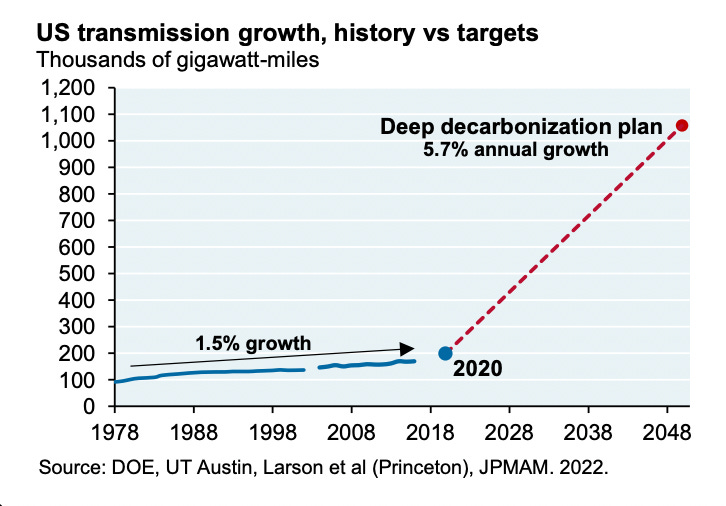

Charts

We need to hit 5.7% annual growth in the grid, but recently, growth has slowed from 1.5% to 1% (for a deeper dive into this, I recommend my interview with Dr Michael Kelly on Engineering Realities).

“But as we have explained, grid expansion is way below a deep decarbonization trajectory. The last two charts show the history of the US grid and how the pace of expansion slowed from 1.5% to 1.0% in the last five years, including rebuilds and upgrades.”

Something I'm Pondering

I'm pondering certain words' role in narratives to justify price action.

Take the word "exponential", which has been used to hype the retail lemmings and distract from silly valuations and faulty investment processes.

I liken Cathie Woods to the golfer who got a hole-in-one after hitting a seagull flying overhead. Of course, you can't deny the hole-in-one, but the repeatability of the process needs to be questioned.

All I think when I read exponential now is premature extrapolation.

It’s also not to say certain technologies won’t experience exponential growth; it’s a fallacy that returns will also experience the same exponential growth.

Take Cisco, which was perfectly positioned for the rise of the internet. It lived up to all its revenue projections yet lost ~90% from its March 2000 high. Valuations matter.

Dan Ferris does a great job of breaking this idea down here: Destined to Become a Long-Term Loser

For example, Cisco Systems (CSCO) was the No. 1 darling of the dot-com era. The company sells the routers and switches that make up the "plumbing" of the Internet. So everybody thought it was a surefire way to profit from the exponential growth of Internet users.

Cisco went public as a penny stock in 1990. It peaked at around $80 per share in March 2000. Then, it crashed to roughly $8 per share in 2002. And it still hasn't returned to its peak.

Cisco earned $2.7 billion in net income in the fiscal year that ended in July 2000. At $80 per share, it was valued at around $560 billion – a little more than 200 times earnings.

At that moment, Cisco had 200 years' worth of earnings baked into its stock price. It could never live up to that kind of wildly irrational expectation.

No business has ever truly been worth that much. Even an amazing, growing technology business serving a new, rapidly expanding market isn't worth that much.

Everybody who bought Cisco's stock anywhere near that level lost money. And more than two decades later, they're still waiting for the investment to pay off...

When you factor in the dividends that Cisco has paid over the past 23 years, the cumulative total return for investors who paid $80 per share in 2000 is a loss of about 25%. Put simply, investors paid too much – and after 23 years, they're still 25% shy of breaking even.

I hope you’re all having a great week.

Cheers,

Ferg

Exponential growth vs valuations matter. Four most expensive words, this time is different. NVDA at 28.5x revenue. Doesn't seem like the best buy.

I believe Germany, in a couple of years, will become a case study on energy absurdity! It´s just incredible the amount of absurd things they are doing.

Thanks for your Ferg´s Finds