Ferg’s Finds

This is a short weekly email that covers a few things I’ve found interesting during the week.

Article

JPMorgan: Security redefined: from peace dividend to resilience premium

The result is what we call the "resilience premium"— a sustained commitment by governments and private capital to harden the systems on which modern economies depend. The central investment question is where capital will concentrate as urgency meets industrial scarcity—and who can address these bottlenecks reliably and at scale.

Podcast/Video

Seth Klarman: “This Is a Bubble” | The Legendary Investor’s Brutal AI Warning

I liked Seth’s framing of:

AI winners

AI losers

AI agnostic (where I’m hunting).

I had the pleasure of jumping on Palisades Gold Radio with Stijn yesterday.

As mentioned in the interview, I’m halfway through my write-up on oil services, in particular the offshore EPC (Engineering, Procurement, and Construction) niche. This sector has had a rough decade, as illustrated by Saipem below and the likes of McDermott (Chapter 11) and Petrofac (Administration/C11). As I work through the remaining players in this sector, their backlogs are building, as they were already looking great before the “de-risk Hormuz” theme turbocharged the thesis.

Quote

It’s all countercyclical. You know the thing: whatever makes sense, never makes money. If it made sense, everyone at Harvard would be a multi-zillionaire.

Another version he sometimes shares is “If it’s obvious, it’s obviously wrong.”

-Mark Fisher

Extracted from this excellent piece by Kevin Muir; IF IT'S OBVIOUS, IT'S OBVIOUSLY WRONG.

Tweet

A quick check of LLM leaderboards shows Chinese open-source GLMs 5.2 Z AI’s in the top 5 spot at 15-25% the cost of the US models, of which we can’t even access the top-performing Fable and Mythos currently. The kicker is that Z.ai trained GLM-5.2 with only Huawei chips. Which reminded me of this from April.

This is the kill line. Jensen isn’t worried about China having AI. He’s worried about China having AI that runs on Chinese hardware. Because if China’s models optimise for Huawei chips instead of Nvidia chips, and those models are open-source, and they diffuse to every country in the Global South — India, the Middle East, Africa, Southeast Asia — then the entire world’s AI stack runs on Chinese infrastructure. Not American.

Computing ecosystems are sticky. Jensen compared it to x86 and Arm — architectures that persist for decades because switching costs are enormous. If the developing world builds its AI infrastructure on Chinese chips running Chinese models, that’s a lock-in that lasts a generation. America doesn’t just lose the Chinese market. It loses every market that China reaches first.

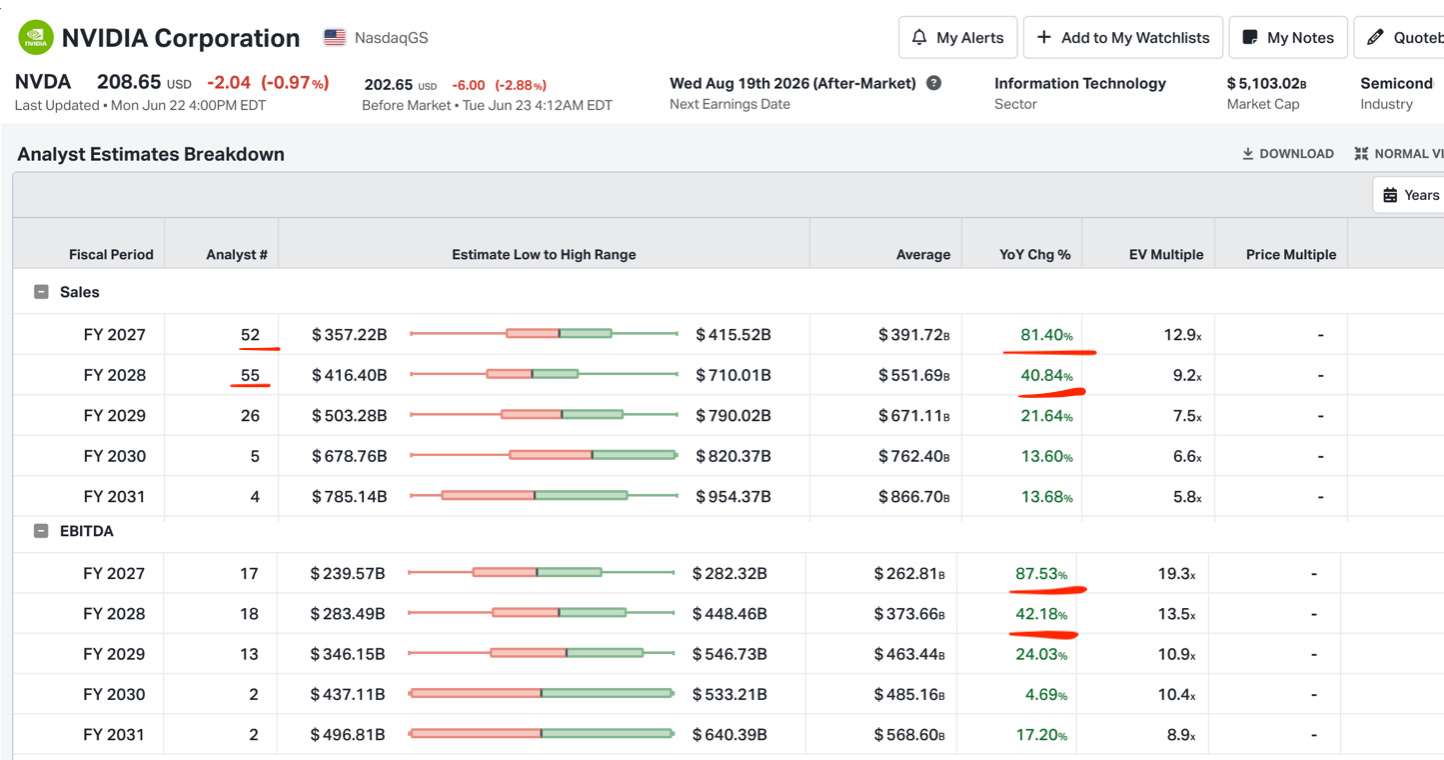

This is a tall order for Nvidia, as the average of 52 analysts expects it to grow sales by 81% in FY2027, 40% in FY2028, and another 21% in FY2029, even as Nvidia is already leaning on circular deals to maintain revenue (Circular deals, analysts say, will account for less than 15% of Nvidia’s projected 2027 revenue). Before considering the US energy/equipment bottleneck, 50% of US data centres are now delayed or cancelled and the potential competition from Huawei, which won’t be running Nvidia’s margins!

Charts

OPEC has released 2026 World Oil Outlook 2050, which has dozens of interactive energy charts.

Something I’m Pondering

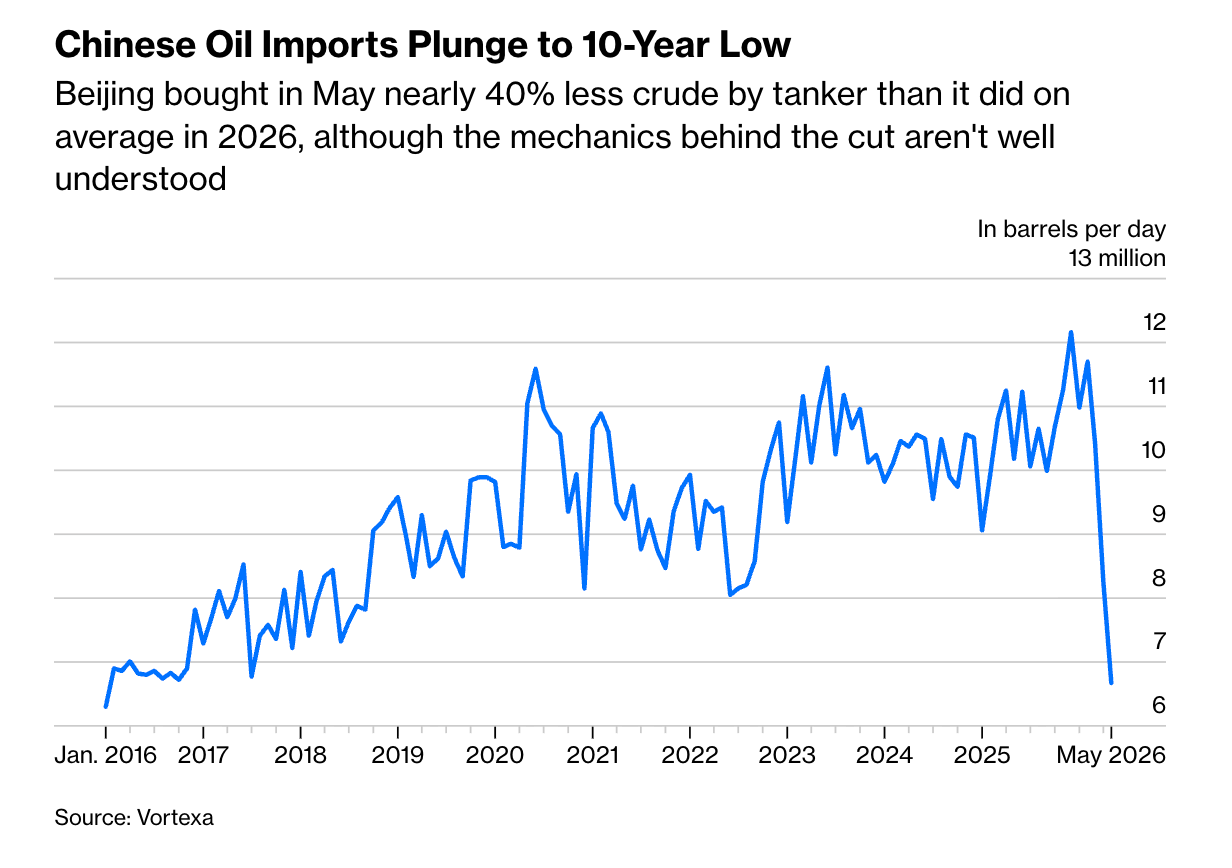

I’m pondering what we’ve learned over the past four months about China’s energy “flexibility.” Their focus on energy security has paid dividends, and I expect other Governments to follow suit (back to “resilience premium”).

Saudi Arabia is known as the “swing exporter” in the oil market because it can either pump out more or less of the black stuff in response to shocks. Historically the kingdom hasn’t had a match on the demand side. Barring a major economic crisis, consuming nations have always kept their purchases steady. Not anymore. After the Iran war, China has emerged as the world’s first oil “swing importer.”

I’m just left with a lot of questions:

Does this flexibility create a more range-bound energy market when China, which accounts for 22-23% seaborne oil trade and ~16% LNG, can step back if prices get too high and stockpile if too low in the oil case?

How much of the oil flexibility was the SPR drawdown? (Underground, which can’t be tracked and isn’t reported).

How much of China’s recent oil demand was due to stockpiling?

What does their coal fleet’s utilisation actually look like, especially given its upgraded flexibility, as there’s again no data to work with? We do know they are still building them rapidly; China Builds Most Coal-Fired Plants in Decade for Power Security.

Hope you are all having a great week!

Cheers,

Ferg

P.S. Mia is showing Hugo and me all the Montenegrin secret spots; this was an epic seafood restaurant on an old boat.

I’ve been steadily buying since publishing this piece.

With regard to the China question, I thought this take was interesting...

https://x.com/gnoble79/status/2069544739829944329

The most powerful force in the oil market is now a single country that doesn't produce a drop.

OPEC IS DEAD

And here's why you should change how you think about energy for the next decade:

China controls the oil price not by pumping it, but by REFUSING TO BUY IT.

For two years, while the West wasn't paying attention, China built a war chest of crude.

They bought cheap, sanctioned barrels at $60 while everyone else looked the other way. They stacked a reserve now estimated between 1.2 and 1.5 BILLION barrels.

Then the world got its biggest supply shock in modern history and instead of panic-buying like everyone else, China did the opposite.

They stopped importing and started eating their own stockpile.

Chinese crude imports collapsed from 11.6 million barrels a day to under 8 million - the lowest level since 2017. That single decision accounted for roughly 74% of the entire drop in global oil demand, according to JPMorgan.

Sit with that number for a second.

The world lost 14% of its crude supply. In 1973, OPEC cut off just 7% and the price exploded 134%.

This shock was twice as large.

But oil went the other way. WTI sits at $74 today.

Because the world's largest buyer simply walked out of the store and lived off its pantry.

THAT is the new OPEC.

For 50 years we obsessed over the Saudis. We watched OPEC meetings like Fed meetings, parsing every production quota. Those days are ending and the most powerful swing force in oil is no longer a cartel that controls supply.

It's one country that controls DEMAND.

And demand is the harder lever. You can cheat on a production quota but you can't force a billion-barrel buyer to show up if it doesn't want to.

Here's what this means for your money right now:

China has capped the upside. As long as they're sitting on that hoard, they sell into every rally toward $100. No spike gets to run. The right tail is gone - stop dreaming about $150 oil.

But they've also built the floor. Those reserves are draining fast.

JPMorgan expects China back as a major buyer by August to start refilling. The US has to refill its own SPR, now at its lowest since 1990. Everyone has to restock at once.

You don't get $100 oil - China sells it to you. You don't get $50 oil - China and everyone else has to come back and buy it.

You get a range. And right now we're sitting at the bottom of it.

Crude is parked on its 200-day moving average. Retail traders are positioned near record short in Brent. Sentiment is in the gutter, RSI under 30.

When the entire crowd leans the same way off the same wrong assumption, I want the other side of that trade.

If I had to bet the next $10 or $15 move in crude, I'm betting higher.

Because the most important player in the oil market already told you exactly what it's going to do.

The Saudis didn't break OPEC. China did - by building a reserve nobody could see and refusing to spend it when it mattered most.